Singapore’s real estate investment trusts (REITs) have had a rough 2022. Rising interest rates in the US and higher inflation have dented their appeal.

Yet REITs listed on the SGX have seen a recent rebound on hopes of that the US Federal Reserve (Fed) will ease the pace of rate hikes.

This move has also coincided with some big Singapore REITs reporting their quarterly numbers.

One such popular name with Singapore investors in the data centre REIT space – Digital Core REIT (SGX: DCRU) – came out with its Q3 2022 earnings last week.

Digital Core REIT listed in Singapore last year and owns 10 data centres in North America, with 100% of its properties being freehold assets.

Here’s what investors in Singapore-listed REITs should know about Digital Core REIT’s latest earnings update for the nine months ending 30 September 2022.

Revenue beats but distributable income falls short

Digital Core REIT saw its revenue come in at US$80.7 million for the 9M 2022 period. This was 1.6% above the forecasted range – made in its prospectus in late November 2021, just before it went public.

Meanwhile, net property income (NPI) for the 9M 2022 period was US$53 million, 5.7% above its forecasted range.

However, the key metric – distributable income attributable to unitholders – was US$34.4 million, coming in 3.4% below the forecasted figure.

Its overall portfolio remained healthy, with occupancy at 100% as of 30 September 2022. The weighted average lease expiry (WALE) of its portfolio stood at 5.0 years.

Two proposed acquisitions

In late September, Digital Core REIT announced that it planned to buy two data centres – one in Frankfurt, Germany and the other in Dallas, which is in the US.

This should help reduce its customer concentration and broaden out its portfolio beyond just North America.

However, while investors should be generally supportive of this, not many REITs are carrying out acquisitions right now.

Management updated investors on in its latest earnings release that it had reached an agreement to acquire a 25% stake in the Frankfurt property (from its sponsor), with an option to acquire up to an 89.9% interest in it.

Separately, it also plans to acquire a 90% interest in a purpose-built freehold data centre in Dallas (also from its sponsor).

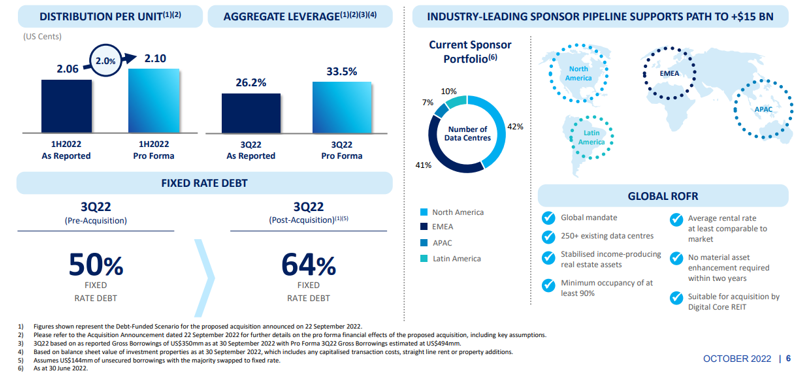

Digital Core REIT has already entered into an interest rate swap for a portion of its Euro term loan. Given it has the debt-funded scenario locked in, the 2% accretion to the REIT’s pro-forma distribution per unit (DPU) will be locked in.

Elsewhere, management did note that market vacancy across its four markets has tightened considerably given near-term supply constraints. That’s a positive sign for the data centre market.

Concerns over floating debt

Perhaps one of the biggest concerns for Digital Core REIT investors, though, has been the percentage of floating debt that the it’s exposed to.

While the latest acquisition (and subsequent debt funding) will improve the fixed rate debt portion of its debt load (see below), it will still be a relatively high 64%.

However, this is partially offset by the fact that its leverage – even post-acquisition – will be at a relatively conservative level of 33.5%.

Digital Core REIT’s massive sponsor – Digital Realty Trust Inc (NYSE: DLR) – also provides some visibility on growth for the SGX-listed REIT given its parent has a large pipeline of global data centre properties.

Source: Digital Core REIT 9M 2022 earnings update

Source: Digital Core REIT 9M 2022 earnings update

High yielding but little visibility on DPU impact

Overall, it was a solid showing from Digital Core REIT. Unfortunately for it, the REIT’s listing came just as the Fed starting raising interest rates furiously.

As a result, it’s in the same boat as many other local REITs but without the track record of years of DPU increases.

Given that uncertainty, investors seem to be avoiding its shares for now. The unit price of Digital Core REIT is down over 57% so far in 2022.

On a 12-month forward (pro-forma, post-acquisition) DPU of 4.20 Singapore cents, REIT investors are getting a whopping 8.4% dividend yield if they buy Digital Core REIT shares today.

The key question for investors is whether the REIT can maintain and, subsequently, grow its DPU from here.

Disclaimer: ProsperUs Head of Content & Investment Lead Tim Phillips doesn’t own shares of any companies mentioned.