In terms of years, 2022 is going down as one of the worst in recent memory for investors. Despite Singapore’s stock market holding up relatively well, it’s still applicable to investors here.

That’s particularly true for REIT investors, who have been hit by both rising interest rates and a slowing global economy.

So, earnings of key Singapore REITs are even more in focus than usual this earnings season as investors look for any signs of distress.

Yesterday (26 October), Mapletree Industrial Trust (SGX: ME8U) reported its results for its Q2 FY2023 period (for the three months ending 30 September 2022).

The large industrial and data centre REIT is a popular holding among local investors given its relatively solid long-term gains.

How did Mapletree Industrial Trust perform in its latest results? Here’s a quick breakdown of what REIT investors should know.

Revenue and profit up but DPU falls

Mapletree Industrial posted gross revenue of S$175.5 million and net property income of S$130.3 million in Q2 FY2023.

That was up 12.8% and 8.3%, respectively, year-on-year from the same period in 2021.

However, the key metric for dividend investors – distribution per unit (DPU) – actually fell on a year-on-year basis.

The REIT declared a DPU of 3.36 Singapore cents for its latest quarter but that was down 3.2% from the 3.47 Singapore cents DPU declared for Q2 FY2022.

Meanwhile, on a quarter-on-quarter basis, the DPU was down 3.7% from the 3.49 Singapore cents paid out for Q1 FY2023.

Borrowing costs jump, portfolio occupancy rises

Perhaps unsurprisingly, given how interest rates are rising, Mapletree Industrial’s borrowing costs surged.

In a similar vein to Mapletree Logistics Trust (SGX: M44U), following its earnings, borrowing costs for Mapletree Industrial hit S$23.8 million in Q2 FY2023 – up 36.6% from the same period last year.

Thankfully for the industrial REIT, though, its debt maturity profile is pretty well staggered. It has only 11.9% of its debt due for the rest of FY2023 while in FY2024 only 6% of debt comes due.

On the portfolio occupancy front, there was good news as its overall occupancy improved quarter-on-quarter from 95.3% to 95.6%.

This was driven mainly by Singapore, where the average occupancy rate improved to 96.8% (from 96.0% in the prior quarter) and there were positive rental reversions across its property types.

This was partially offset by its North American portfolio, which saw occupancy fall quarter-on-quarter from 94.0% to 93.1%.

How about the DPU impact from rising rates?

This is a question that is on the minds of all REIT investors. Fortunately, there can be guidance provided from management with respects to the impact of rising interest rates.

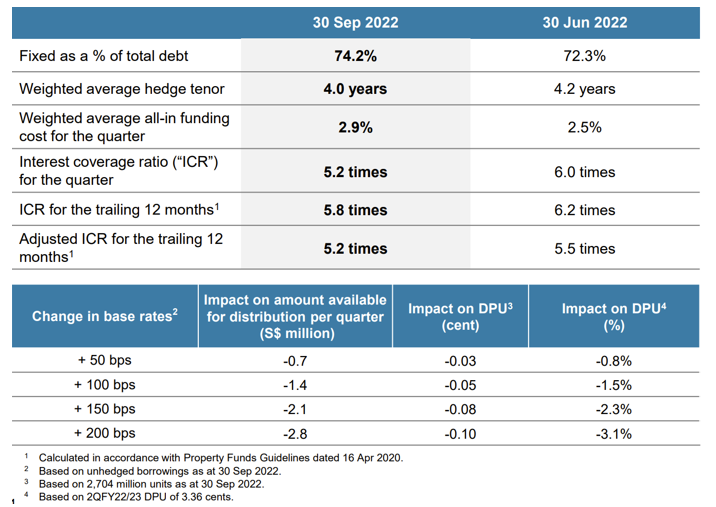

As important as this is how well protected the REIT is from floating rate debt, as in investors should want to see the majority of a REIT’s debt be fixed.

Mapletree Industrial saw its fixed debt (as a percentage of its total debt) hit 74.2% as of 30 September 2022, up from 72.3% at the end of June 2022.

That should help with visibility on the DPU impact from rising rates. Management provided a detailed breakdown on the impact of rate hikes and subsequent DPU erosion (see table below).

On the interest coverage ratio (ICR) front, Mapletree Industrial is still well protected despite a slight fall in its ICR over the past quarter.

Meanwhile, the REIT’s gearing ratio fell to 37.8% as of 30 September 2022, down from 38.4% as of the end of June 2022.

Source: Mapletree Industrial Trust Q2 FY2023 earnings presentation

New properties coming and releasing distributions

Management stated its intention to be prudent with how it manages its capital.

Mapletree Industrial managed to raise S$40.2 million from the application of its distribution reinvestment plan (DRP) for its Q1 FY2023 distribution. The DRP will again be applied for its Q2 FY2023 DPU.

The REIT’s big redevelopment at Kolam Ayer 2 is set to be operational in the first half of 2023. This was a property enhancement project that has been in the works for a few years, which will see the existing plot of land turned into new hi-tech buildings – including a build-to-suit (BTS) property.

Finally, Mapletree Industrial’s management announced its intention to progressively release up to S$6.6 million in tax-exempt income (that had been in reserve during the pandemic) to help mitigate rising operating and borrowing costs.

This amount will be released over three quarters beginning in Q3 FY2023.

Overall, it was an admirable quarter amid challenging economic conditions. Mapletree Industrial Trust currently trades for S$2.25, giving dividend investors a 12-month forward distribution yield of 6.0%.

Disclaimer: ProsperUs Head of Content & Investment Lead Tim Phillips owns shares of Mapletree Industrial Trust.

")