Get the ULTIMATE guide on how to invest successfully in Singapore REITs + our Top 5 S-REIT picks! Download now

Singapore REITs: 2 REITs to Buy in Office and Retail

September 6, 2021

As of late August, approximately 80% of Singapore’s population is now fully vaccinated, and the city is gradually reopening for business. People are going out again; shopping, dining, and working.

Up to 50% of companies’ “work from home” employees can now return to the office. People are shopping. More importantly, vaccinated Singaporeans can dine-in again.

The idea is that with one of the highest vaccination rates in the world, Singapore can pivot from a zero-COVID strategy to living with COVID as endemic.

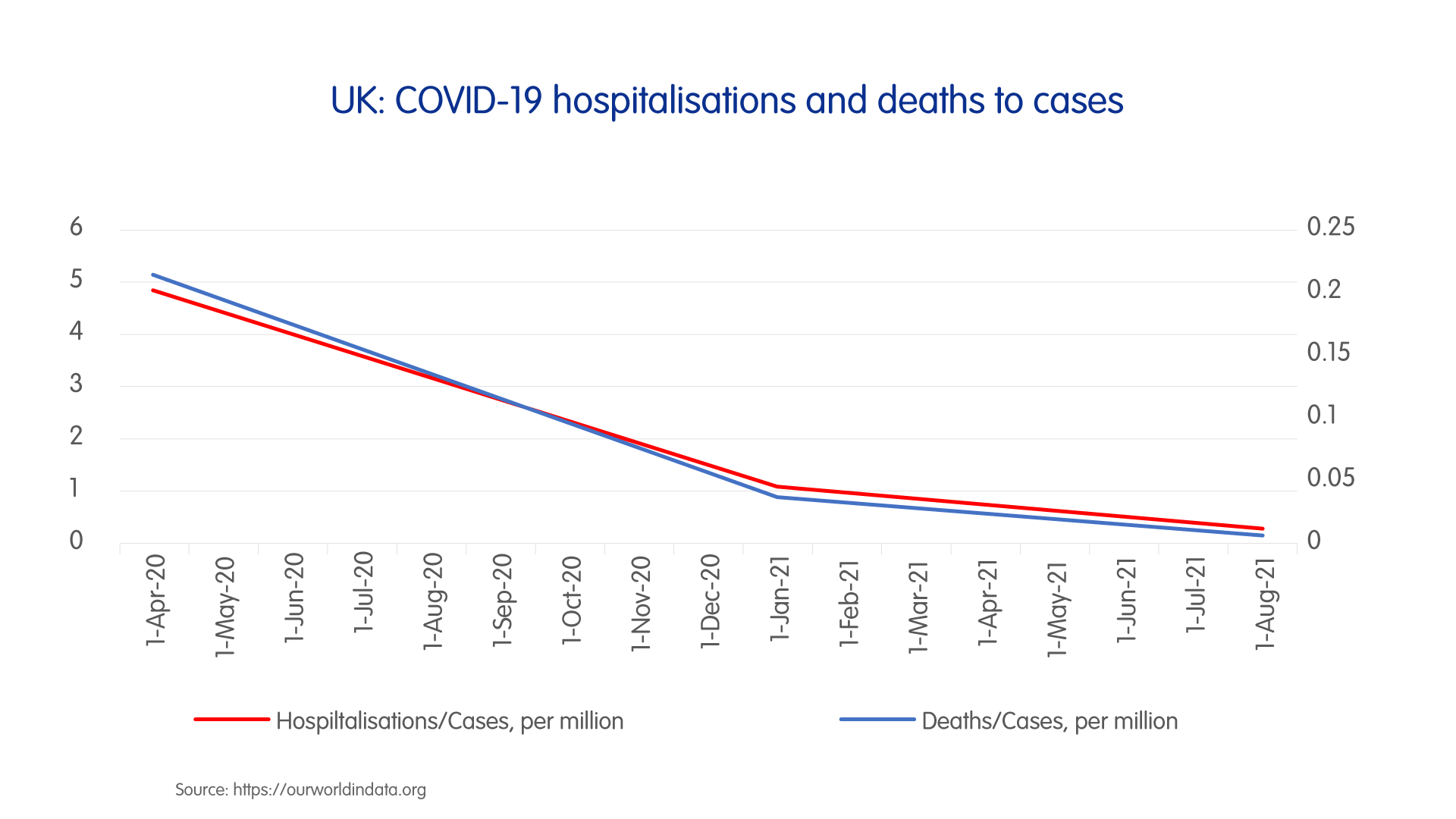

Case numbers will rise with reopening, but hospitalisations as a percentage of cases will likely decline, and deaths as a percentage of cases should also likely fall.

And that’s the same theory driving the strategy in other countries, such as the UK (see Figure 1 below).

But what does this mean for Singapore’s REITs?

Sideways trading but with risks

Unit prices of Singapore REITs have, on average, been ranging sideways from early July. If the strategy works, it could well mean that we are long past the lows in prices.

The Singapore S-REIT index has seen a series of higher lows from April of last year. But recently, possibly under pressure from the spread of Delta, we have also seen lower highs – with the index falling some 3% from the July high.

But seen more broadly, it has been in a trading range since early July (Figure 2 below).

Source: Refinitiv

The dangers are yet more infectious new variants or society flinching at higher absolute numbers of deaths.

The biggest risk that could push REITs prices lower is the rise of new variants – even more infectious and more resistant to existing vaccines.

Another risk is that if there is widespread infection, deaths could rise in absolute numbers – testing social acceptance and rendering percentages meaningless.

Buying opps on the horizon?

If Singapore pushes through the pain of reopening, retail and office REITs could be buying opportunities.

But if the basis of reopening is correct – that vaccines will make the virus less deadly and that societies, including Singapore, will battle through this – the two biggest losers from domestic lockdowns (retail and office REITs) could be the biggest winners.

Not coincidentally, the two most attractively valued REITs sectors are office and retail REITs. Retail REITs are now trading at an average of around 5.6% estimated FY22 yields and at net asset value (NAV).

And office REITs are at an average of around 6.0% forecast FY22 yields and approximately 0.77x their NAV.

Frasers Centrepoint Trust

Frasers Centrepoint Trust (SGX: J69U), also known as “FCT”, is a pure Singapore suburban shopping mall play.

So, if you’re looking at pure Singapore retail plays – or at least REITs with an overwhelming focus on Singapore assets – then the lowest valuation among those we cover is FCT.

With a price-to-NAV of around 1, it also has an FY22 expected yield of 5.3%.

FCT is a pure play on Singapore’s heartland malls. Hence, it is most leveraged on normalisation of life in Singapore.

Its portfolio occupancy has been strong at 96%, with Tampines 1 running at 99%.

But successful reopening will likely lift tenant sales and shopper traffic which had been affected by restrictions over recent months. It will also help with lease renewal negotiations.

CGS-CIMB Research has an “add” rating with a S$2.91 target price for FCT. As we are currently seeing a rise in COVID-19 case numbers in Singapore, there could be some retracement of recent gains in FCT’s price.

Ideally, I would be looking to buy in at the S$2.30-2.35 range.

OUE Commercial REIT

OUE Commercial REIT (SGX: TS0U) is a Singapore office play, but note that it has two hotels and a China office property.

From the office REITs we cover, the one that has a large focus on Singapore properties is OUE Commercial REIT, which is trading at only around 0.72x its NAV and at an FY22 estimated yield of 6.7%.

But do be aware that it also has a retail property in Orchard Road’s Mandarin Gallery.

And this lower valuation comes with a couple of hotels (Mandarin Orchard and Crowne Plaza Changi Airport) that are likely to be much later beneficiaries of reopening – when tourism resumes.

Also, its portfolio includes an office tower in Shanghai. Overseas-centric REITs tend to be accorded lower market valuations.

CGS-CIMB Research has a “hold” rating for OUE Commercial Trust, with a S$0.45 target price. Likewise, there could be some “give-back” of recent gains on rising daily COVID-19 cases, and I would prefer to buy in the S$0.40-0.41 region.

Back to our old way of life?

Now if you think we are never going back to the office, we’re never going shopping the way we used to, and tourists will never come back, don’t buy any of this.

But if you see a post-COVID normal eventually returning, then these two Singapore REITs might be long-term opportunities for investors.

Disclaimer: CGS-CIMB Securities Chief Investment Strategist Say Boon Lim doesn’t own shares of any companies mentioned.

Say Boon Lim is CGS-CIMB's Melbourne-based Chief Investment Strategist. Over his 40-year career, he has worked in financial media, and banking and finance. Among other things, he has served as Chief Investment Officer for DBS Bank and Chief Investment Strategist for Standard Chartered Bank.

Say Boon has two passions - markets and martial arts. He has trained in Wing Chun Kung Fu and holds black belts in Shitoryu Karate and Shukokai Karate. Oh, and he loves a beer!