While many in the Singapore REIT sector reported declining earnings and falling distribution per unit (DPU), CapitaLand Integrated Commercial Trust (SGX: C38U), or CICT for short, delivered strong and robust earnings during the H1 FY2023.

For dividend and S-REIT investors in Singapore, here are some key highlights from CICT’s strong earnings during the H1 FY2023.

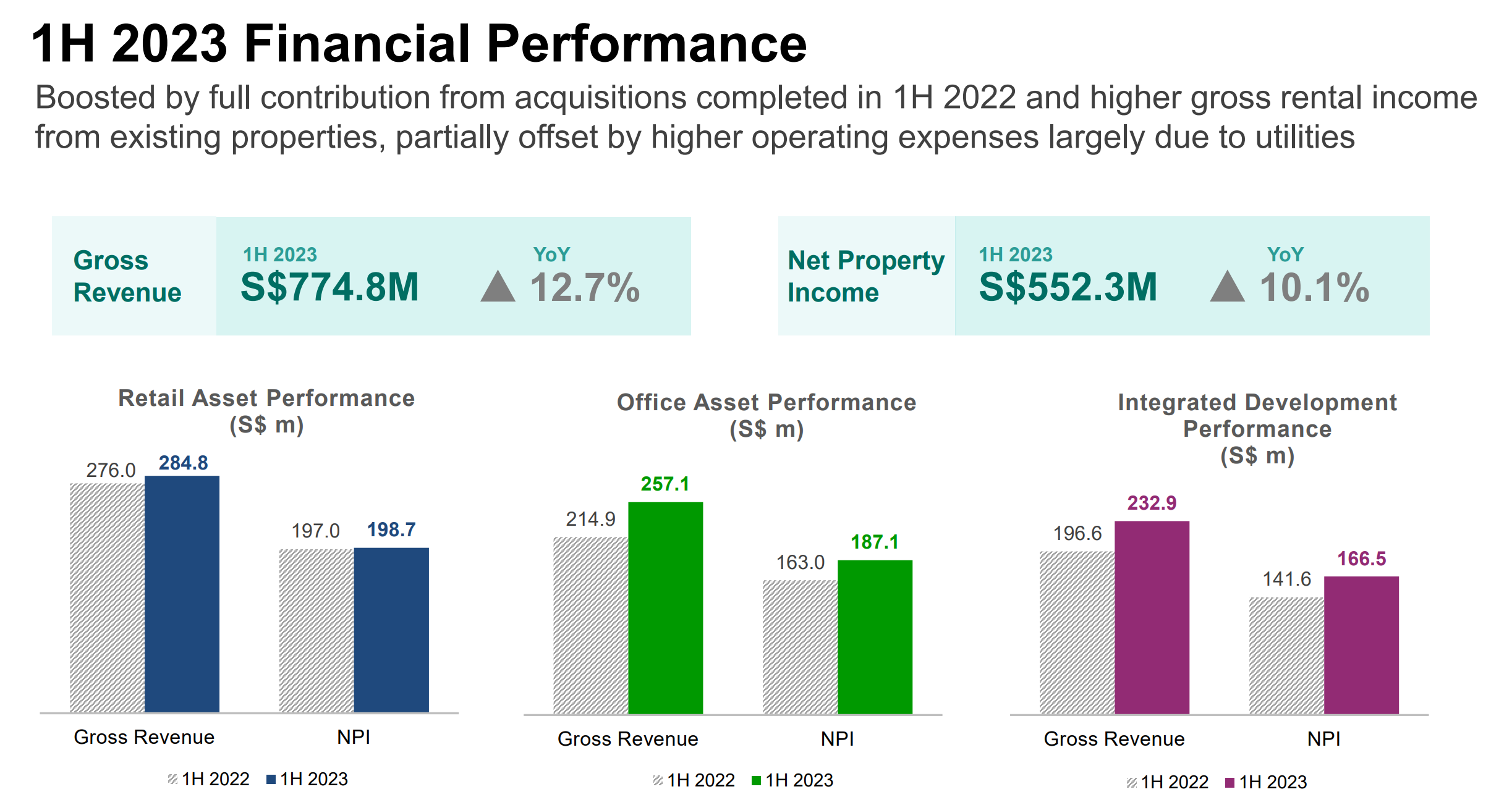

1. CICT maintains earnings growth despite rising costs

CICT recorded year-on-year (yoy) growth of 12.7% and 10.1% in H1 FY2023 revenue and net property income (NPI), amounting to S$774.8 million and S$552.3 million, respectively.

Source: CICT’s H1 FY2023 earnings

This positive trend resulted from a six-month contribution by CapitaSky (acquired in April 2022), revenues from Australian acquisitions (secured in June 2022), and asset upgrades at Raffles City Singapore.

This growth was slightly countered by increased utility costs.

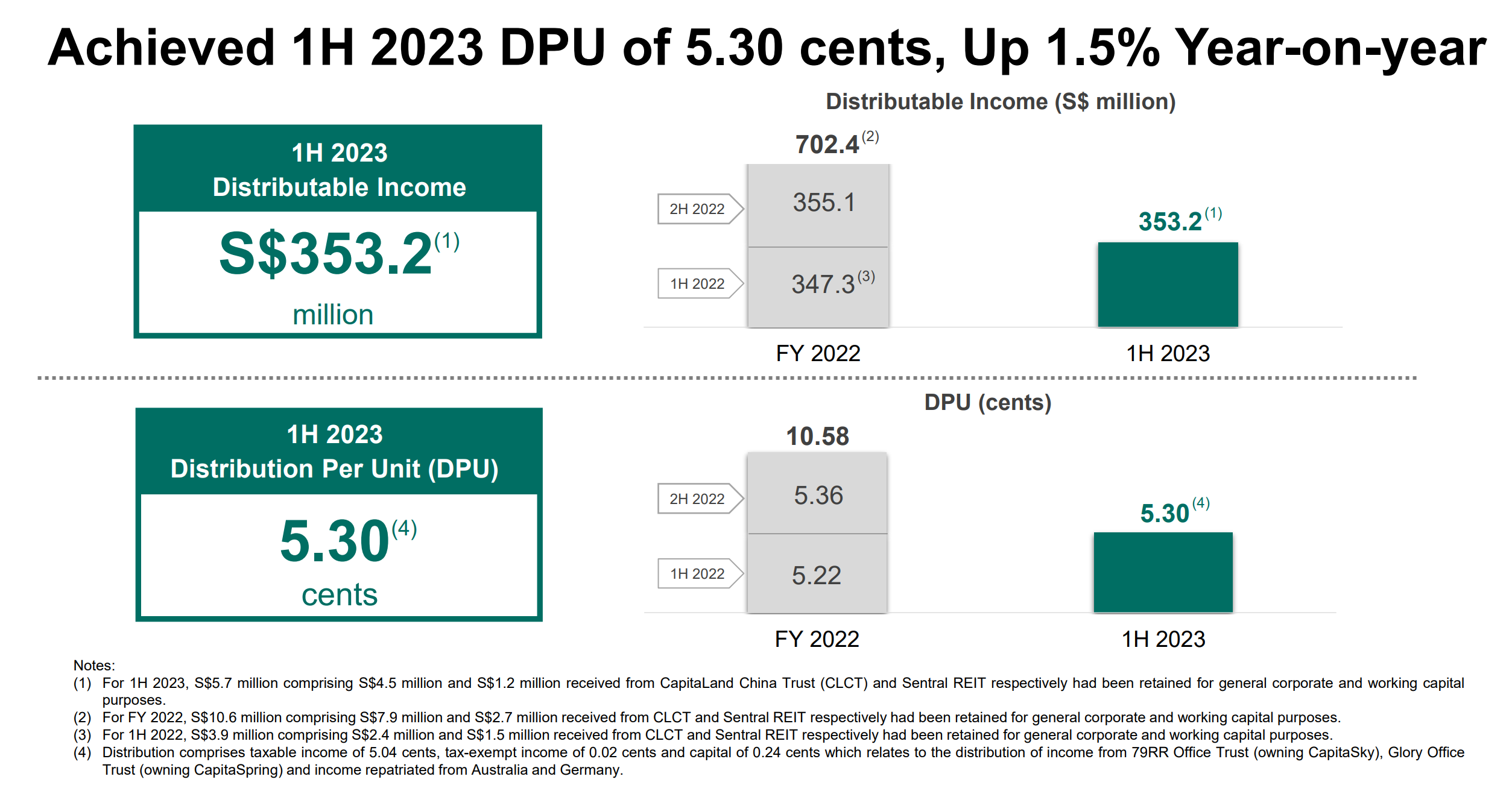

2. Modest growth in DPU

The 1H23 DPU saw a modest increase of 1.5% yoy, reaching 5.3 Singapore cents, despite rising interest expense.

Source: CICT’s H1 FY2023 earnings

The average cost of debt rose to 3.2% as of 30 June 2023, compared to 2.4% a year ago.

This was in line with the rising interest rate environment.

Management has guided that it could rise to around 3.5% in FY2024.

3. Strong retail sector performance

The H1 FY2023 period saw CICT’s retail division display positive rental reversion of 6.9%.

The REIT’s downtown malls stood out with an impressive 7% growth.

Retail tenant sales and shopper count increased by 6% and 17.5% yoy, respectively.

Downtown malls profited from increased tourist numbers and the return of the office-going population.

With a positive outlook for the retail sector, CICT foresees a rise in retail rents and occupancy rates in the latter half of 2023.

The enhancement works at CQ @ Clarke Quay are on track for a late-H2 FY2023 completion.

4. Moderation in growth for office spaces in the near-term

During H1 FY2023, commitments to office spaces witnessed a 0.6% rise, reaching 9.4%.

This was primarily boosted by greater demand for newly-fitted suites at 66 Goulburn in Australia.

There was a notable positive rental reversion in office space by 9.6%, with 304.2k sq ft renewed in the second quarter.

However, the management predicts a moderation in office rental growth in the second half due to potential supply and reduced demand.

A significant development is the expiration of Commerzbank’s lease at the Gallileo skyscraper in January 2024, followed by a significant 18-month enhancement plan.

The building will be without income during this period.

However, its impact is subdued since it contributed less than 2% of CICT’s total revenue in FY2022.

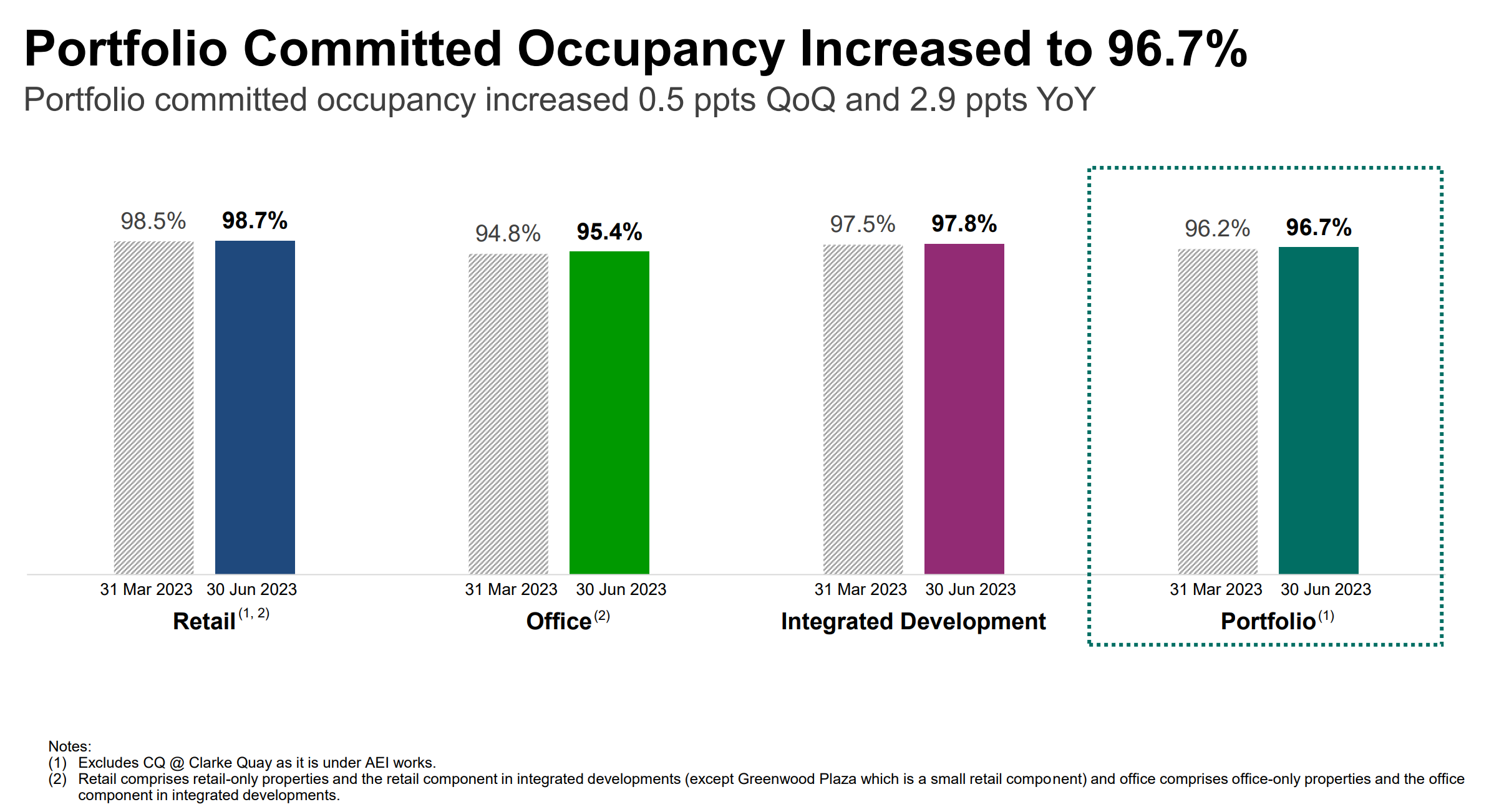

5. Strong occupancy rate and diversified tenants’ business trade mix

CICT has strong portfolio occupancy rates across both its retail and office segments.

In H1 FY2023, the REIT’s portfolio’s committed occupancy increased to 96.7%.

Source: CICT’s H1 FY2023 earnings

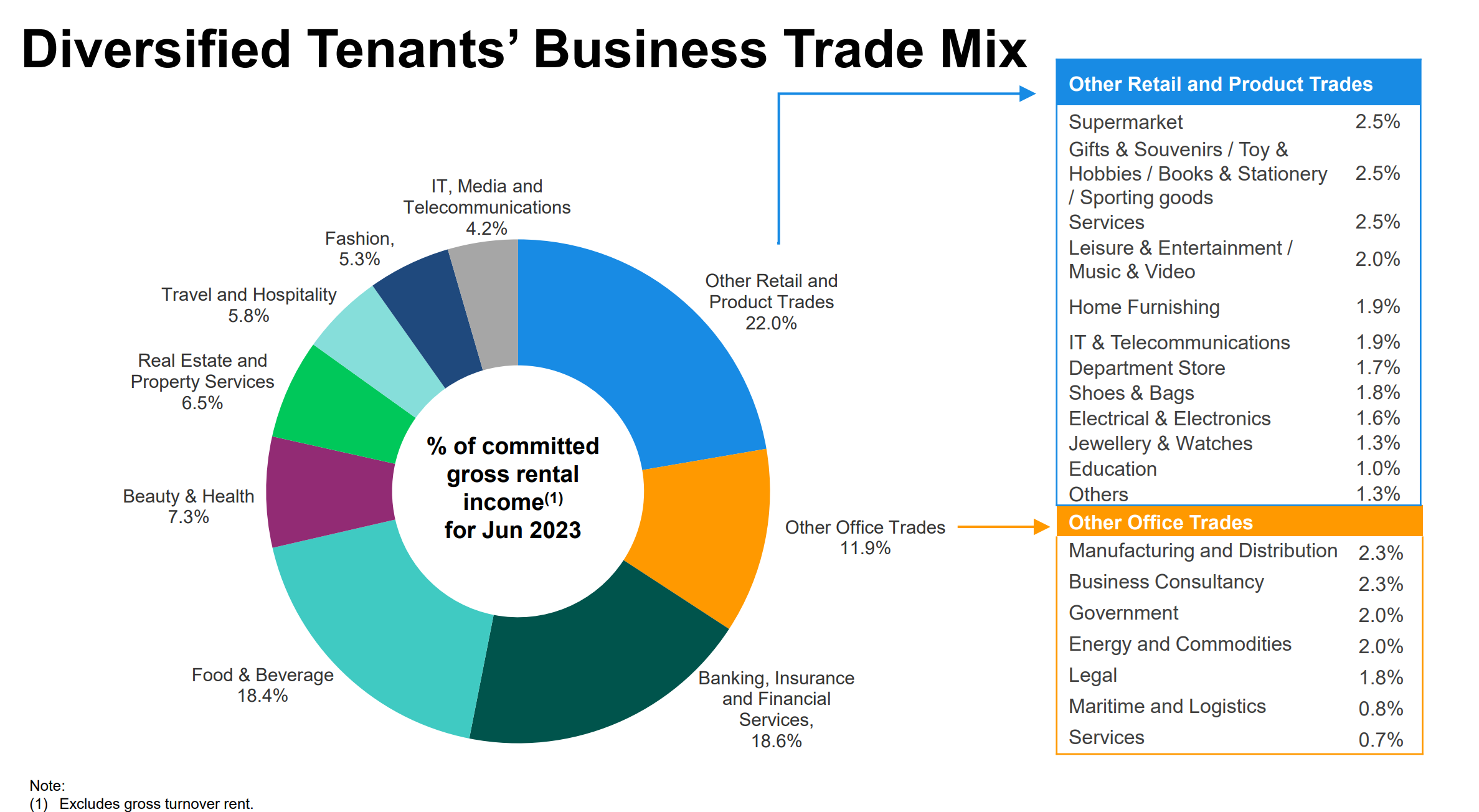

One of the key strengths of CICT’s portfolio is its diversified tenants’ business trade mix.

This helps to avoid concentration risks for the integrated REIT player.

Source: CICT’s H1 FY2023 earnings

Invest in CICT for its attractive yield and strong track record

CICT is the first and largest REIT listed on the Singapore Exchange.

The strong track record that CICT has over the years puts it top of investors’ lists for those looking for long-term investments.

Aside from that, with a forward dividend yield of 5.3%, CICT will fit into dividend investors’ portfolios.

As we reach the end of the interest rate hike cycle, I believe the worst is over for Singapore REITs and investors looking for long-term investment opportunities will find CICT to be an interesting option.

The downside risk, however, remains as a sluggish rental recovery pace and potential operational costs surge amid rising interest rates and persistent inflation which could impact anticipated returns.

Disclaimer: ProsperUs Investment Coach Billy Toh doesn’t own shares of any companies mentioned.