As we kickstart the earnings season for Singapore REITs this week, let’s take a look at Suntec REIT (SGX: T82U). It happens to be one of the oldest REITs listed in Singapore.

Suntec REIT is currently trading at an attractive forward 12-month dividend yield of 6.8%.

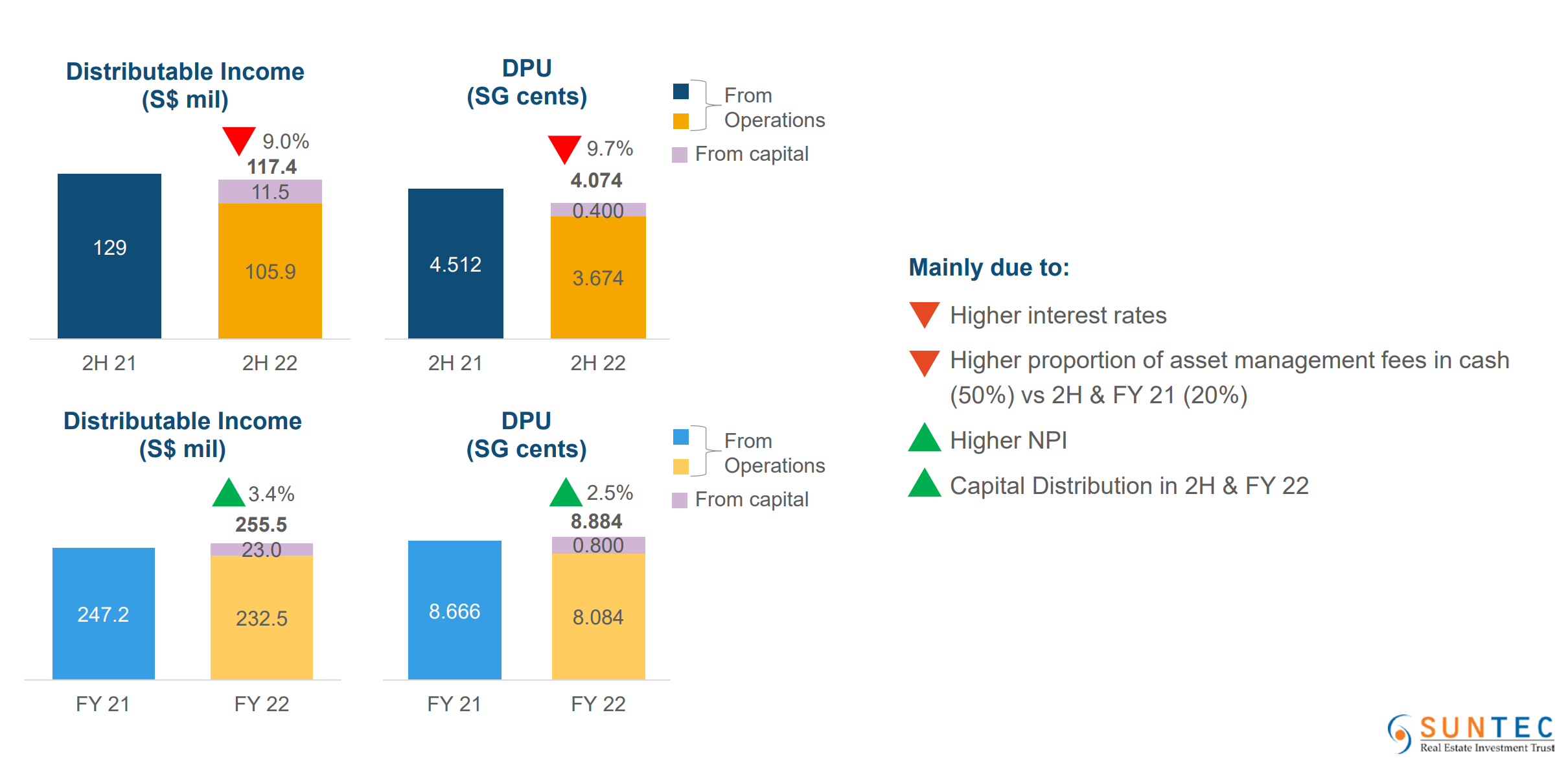

However, the latest earnings results for Suntec REIT – for H2 FY2022 – shows that distribution per unit (DPU) was down by 9.7% year-on-year (yoy) to 4.074 cents.

I believe that there are five key risks that REIT investors should be aware of when considering Suntec REIT as part of your dividend portfolio.

1. Rising financing cost

One of the notable consequences of rising interest rates is the impact on Suntec REIT’s financing cost.

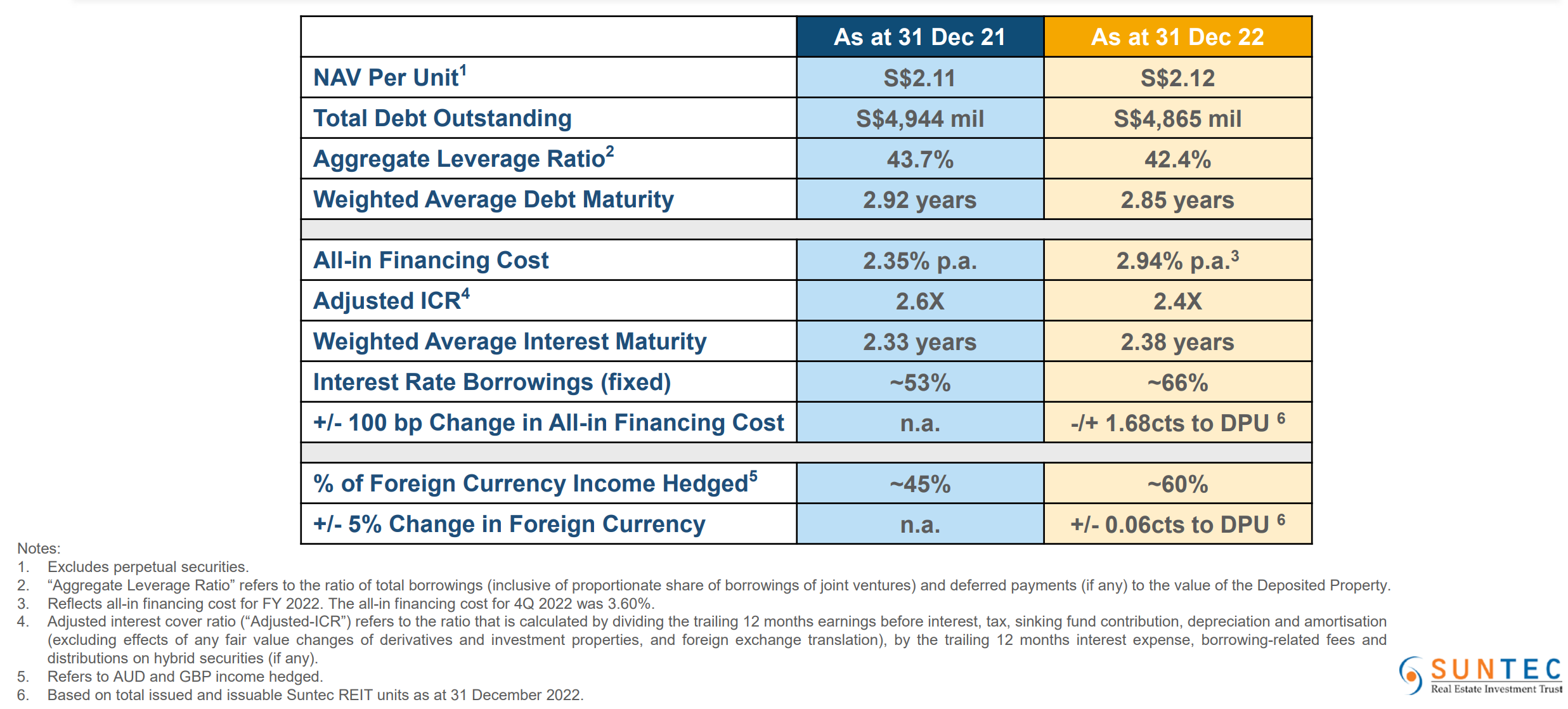

The all-in financing cost has increased to 2.94%, as at 31 December 2022, as compared to 2.35% a year ago.

In fact, the all-in financing cost for the Q4 FY2022 was as high as 3.60%.

While all REITs are likely to face a similar issue amid rising interest rates, Suntec REIT’s borrowings consist of a higher percentage of floating rate borrowings.

In fact, its fixed interest rate borrowings only stood at 53% as of 31 December 2021.

While management has increased its fixed interest rate borrowings to 66% by the end of FY2022, the impact from higher rates will be more pronounced since it has a higher proportion of floating interest rate borrowings.

Source: Suntec’s Financial Results Presentation for H2 FY2022 and FY2022

2. Higher financing cost erodes dividend

Distribution per unit (DPU) for H2 FY2022 was down by 9.7% yoy to 4.074 Singapore cents, from 4.512 Singapore cents a year ago.

The decline was mainly due to the sharp rise in financing cost amid rising rates.

Since DPU growth is an important metric for all REIT investors, this could add further pressure to Suntec REIT.

Source: Suntec’s Financial Results Presentation for 2HFY2022 and FY2022

3. Higher gearing level versus peers

Suntec REIT’s gearing ratio improved to 42.4% as of the end of last year, from 43.1% a year earlier.

However, the gearing level is still on the high side versus its peers (average gearing ratio of S-REITs stood at 37%) and has been one of the key concerns of investors when it comes to Suntec REIT.

Any significant reduction in portfolio value could affect the REIT’s gearing ratio further.

Aside from that, the limited room for borrowings also caps its potential to expand its portfolio further in the near term.

4. Office demand could slow down

Source: Suntec’s Financial Results Presentation for H2 FY2022 and FY2022

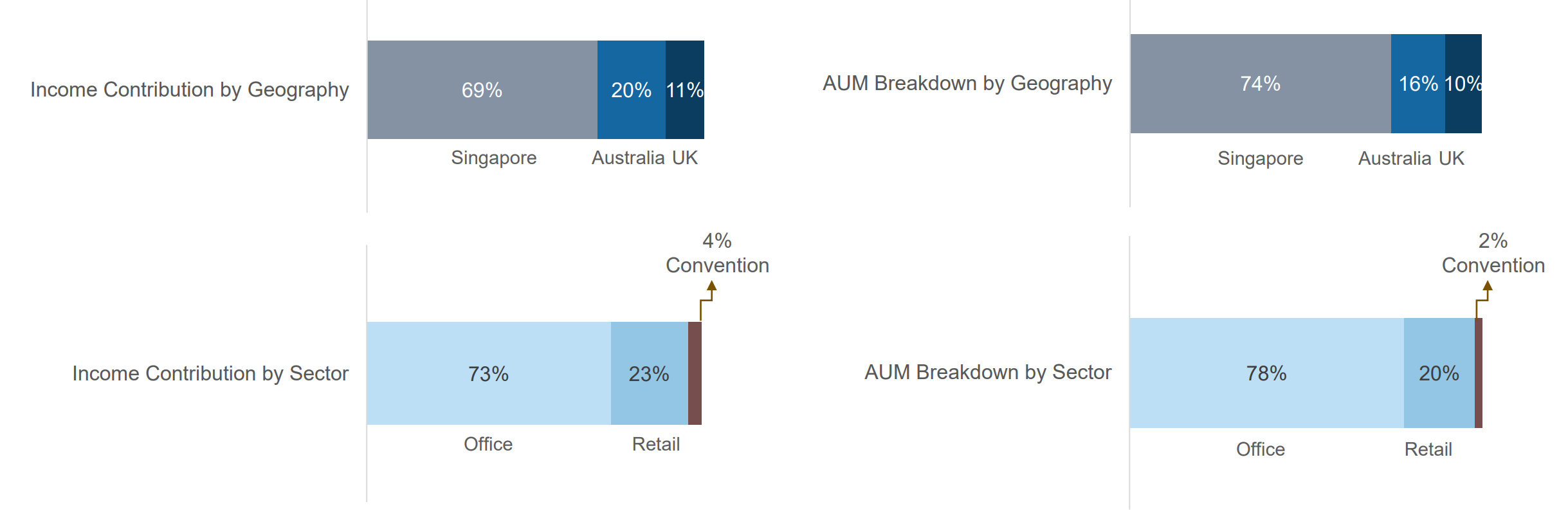

Singapore is the largest contributor of property income to Suntec REIT and it also has more than 73% of its revenue coming from the office space.

While limited supply remains the silver lining in a soft office market, the easing demand of office space in the near future will also affect Suntec REIT.

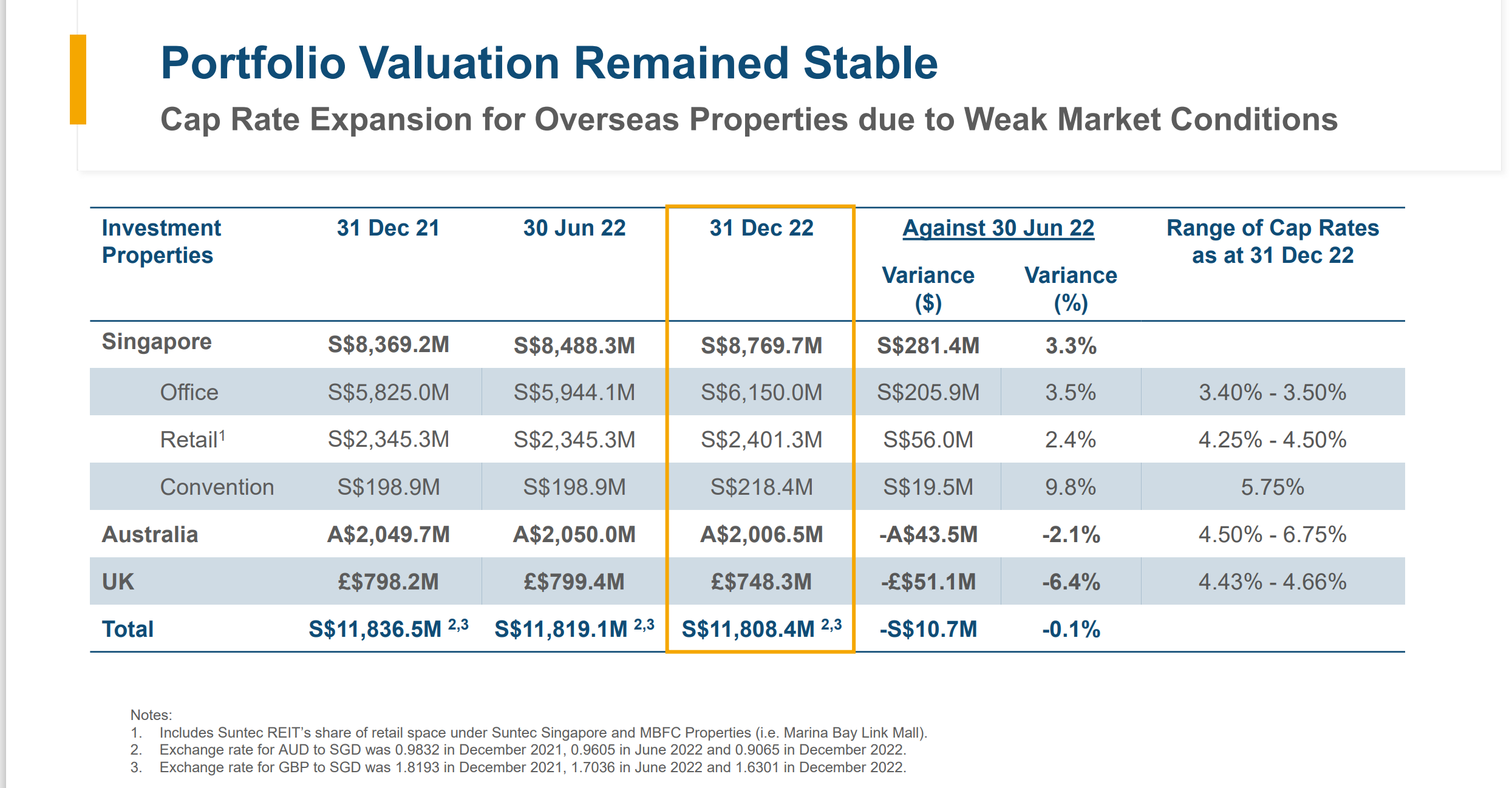

5. Falls in its Australia and UK portfolio values

Source: Suntec’s Financial Results Presentation for H2 FY2022 and FY2022

Looking at the chart above, you can see that the portfolio valuation in both Australia and the UK deteriorated in H2 FY2022.

Aside from that, the weaker Australian dollar and leasing downtime also led to a decline in contributions from the Australia portfolio.

Meanwhile, the REIT’s UK portfolio remained resilient but the weaker British pound affected earnings.

The positive takeaway is that its Singapore portfolio, which is the largest contributor to Suntec REIT, has continued to strengthen.

Challenging near-term outlook for Suntec REIT

While Suntec REIT has managed to increase its DPU by 2.5% yoy to 8.884 cents for the full year FY2022, the near-term outlook will be challenging for the REIT.

Given that fixed interest rate borrowing remains low at 66%, a further rise in interest rates will hurt margins further.

Aside from that, the near-term outlook for the office and retail space will remain challenging, especially if the world falls into a global recession this year.

Disclaimer: ProsperUs Investment Coach Billy Toh doesn’t own shares of any companies mentioned.