In Singapore’s REIT market, the price action lately has been ugly. That’s because the US Federal Reserve (Fed) recently announced a jumbo-sized 75-basis point (bp) interest rate hike.

The result was that many Singapore REITs saw their share prices fall by double-digit percentages in the weeks following the late September announcement by the Fed.

In a way, that wasn’t a surprise given that REITs tend to benefit from lower interest rates.

However, the furious pace of interest rate hikes – in stark contrast to slow and steady rate hikes from 2016-2018 – has caused concern for REITs.

Yet even among the downturn in REITs, there are now some compelling opportunities starting to crop up.

Within Singapore’s Straits Times Index (STI), there’s also one large constituent REIT that now sports a dividend yield of over 6%. Here’s what investors should know about this blue-chip REIT.

Global logistics properties

One of the biggest Singapore REITs that’s also a constituent of the STI is Frasers Logistics & Commercial Trust (SGX: BUOU), also known as “FLCT”.

The REIT owns around 105 properties across Australia, Singapore, Germany, the Netherlands, and the UK.

While it appears to be also a commercial REIT – given its name – it has 97 properties that are part of the Logistics & Industrial (L&I) segment.

Adding to that is the fact that the L&I segment of its portfolio continues to maintain a 100% portfolio occupancy rate.

Its latest quarterly update for its Q3 FY2022 period (for the three months ending 30 June 2022) showed a solid rental income profile.

Overall, occupancy for its portfolio actually ticked up to 96.5% at the end of Q3 FY2022, versus 96.1% at the end of H1 2022.

So, despite this FLCT’s share price is down by nearly 14% in the last month alone. So far in 2022, its shares are down by 21.6%. Why have investors sold it off?

Issues with Europe and weaker currencies

For REIT investors, outside of rising interest rates, the main issue for FLCT has been weakening currencies.

That’s particularly true of the Euro and British Pound, which have weakened considerably so far in 2022 versus the Singapore dollar (the currency which the REIT reports in).

A weaker Australian dollar hasn’t helped either given 65 of its 105 properties are located Down Under.

With an energy crisis brewing in Europe, and winter approaching, investors seem to view FLCT’s exposure to Europe as a weakness in the current market environment.

That’s understandable but FLCT also appears well-equipped to weather the storm ahead.

Positive rental reversions and low gearing

One of the big positives to come out of its latest earnings was the fact that FLCT saw solid positive rental reversions across its portfolio.

It saw solid quarter-on-quarter leasing activity while rental reversions benefitted from inflationary pressure – especially in Europe – as its renewal leases are linked to underlying CPI.

Meanwhile, in Australia, the REIT saw leases re-contracted at average positive reversions ranging from +5.5% to +9.2%.

In Europe, one L&I lease was renewed at a +17.7% uplift. That’s solid evidence that the REIT is being able to use inflation to its advantage.

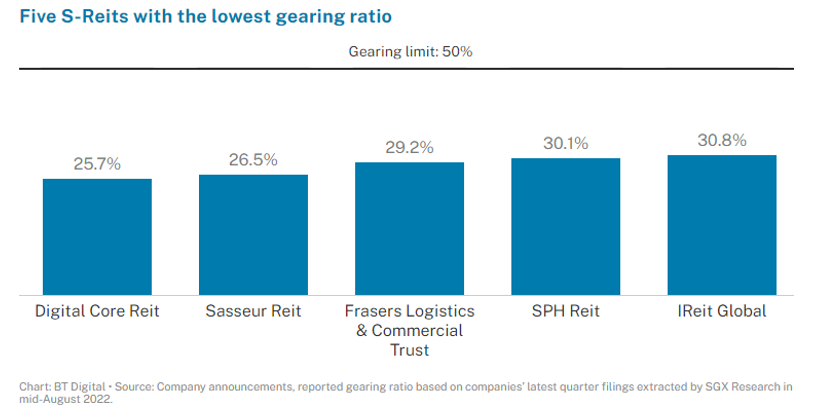

On the gearing side, the news is also bright. In fact, FLCT is one of the five Singapore REITs with the lowest gearing ratio (see below).

With just 29% gearing, the REIT has sufficient debt headroom to acquire if it spots opportunities.

Source: SGX Research

Yielding over 6% but risks remain

So, while the REIT has seen its share price take a hit this year, it’s now the only STI REIT that yields in excess of 6%.

With its latest half-year distribution per unit (DPU) of 3.85 Singapore cents, the REIT is paying a 12-month forward DPU of 7.60 Singapore cents.

That equates to a forward dividend yield of 6.3%. However, for investors, it’s important to remember that the REIT isn’t immune to rising rates in the US.

Like other REITs, its DPU will be impacted by the pace of interest rate hikes. However, it also depends how far into the rate hiking cycle investors think we are and how deep of a recession is likely in Europe.

With FLCT’s yield of 6.3% while a 10-year Singapore Government Bond yields around 3.5%, is the 2.8% yield premium worth the risk?

That depends on the type of investor you are. Yet for long-term dividend investors, the dividend yield of FLCT is starting to look mildly attractive.

Disclaimer: ProsperUs Head of Content & Investment Lead Tim Phillips doesn’t own shares of any companies mentioned.