One of the best-known and most popular data centre REITs, among dividend investors in Singapore, has been Keppel DC REIT (SGX: AJBU).

However, the pure-play data centre REIT has seen its share price fall by 18.8% over the past 12 months.

My colleague, Tim, has written about some of the reasons for the lack of interest in Keppel DC REIT in his article back in April after the release of its Q1 FY2022 earnings.

Today, I’ll take a look at its H1 FY2022 earnings to see if the selloff in Keppel DC REIT has created a buying opportunity for dividend investors looking for a “recession-resistant” Singapore REIT.

Let’s find out.

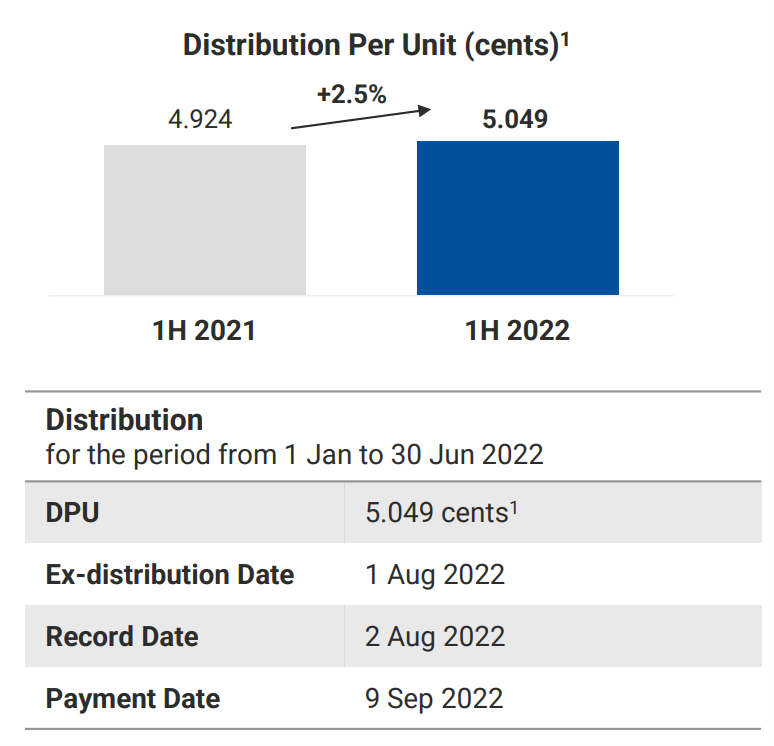

1. DPU rises 2.5%, yield at an attractive 5.1%

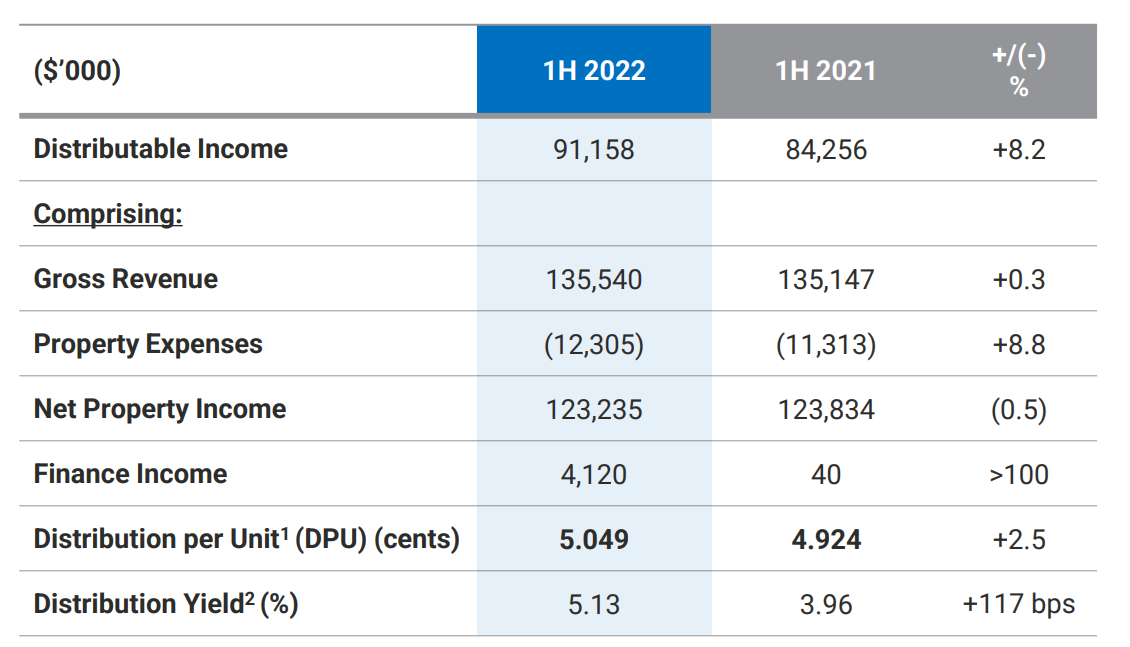

Like any dividend investor, my focus is on the distribution per unit (DPU), which was up 2.5% from a year ago. The REIT announced a DPU for its latest first half of 5.049 Singapore cents.

Source: Keppel DC REIT’s H1 FY2022 Financial Results Presentation

Source: Keppel DC REIT’s H1 FY2022 Financial Results Presentation

Keppel DC REIT has managed to grow its distributable income by 8.2% to S$91.2 million in the H1 FY2022 as compared to a year ago.

That growth is mainly due to the contributions from the accretive acquisitions of Guangdong Data Centre, London Data Centre and Eindhoven Campus, investments in the NetCo bonds, asset enhancement initiatives at DC1 and the Dublin assets, the completion of Intellicentre 3 East Data Centre in July 2021, as well as contract renewals and client expansion.

2. Revenue flat amid impact from Singapore’s ongoing litigation case

Revenue was relatively flat, just 0.3% higher at S$135.5 million in H1 FY2022 as compared to the S$135.1 million in the corresponding period a year ago.

This was mainly due to the 9.8% year-on-year (yoy) in its Singapore revenue, which came from the negative impact of DXC Technology Services.

DXC Technology Services is a tenant at Keppel DC Singapore 1 and Keppel DC REIT has commenced a lawsuit against the company in Singapore’s High Court, according to a March 2022 announcement.

The litigation is over DXC Technology Services’ partial default of payment in connection with the provision of colocation services.

3. Positive rental reversion but rising property expenses a concern

CEO of Keppel DC REIT, Anthea Lee, has indicated that rental reversions were positive for Singapore but no further details were provided for competitive reasons.

There were also earnings accretive acquisitions that have contributed to the increase in income.

To put into perspective, the acquisition of Eindhoven Campus was completed in September 2021 while the acquisition of Guangdong Data Centre and London Data Centre were completed in December 2021 and January 2022.

Despite this, it is worth noting the rising property expenses of 8.8% yoy for Keppel DC REIT during the H1 FY2022.

The increase was mainly due to higher expenses overall, including repairs and maintenance and other property-related costs.

As a result of the increase in property expenses, net property income (NPI) was slightly lower at S$123.2 million during the H1 FY2022.

Source: Keppel DC REIT’s H1 FY2022 Financial Results Presentation

Source: Keppel DC REIT’s H1 FY2022 Financial Results Presentation

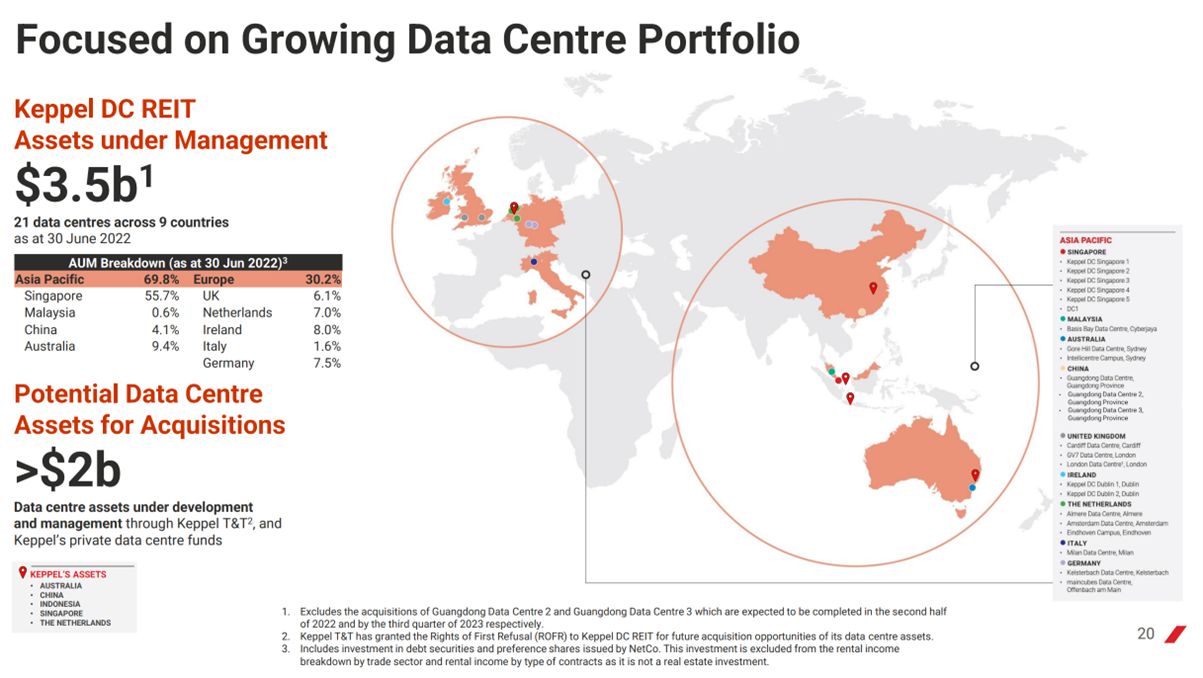

4. Expanding into China

It is also interesting to see how the expansion into China will pan out for Keppel DC REIT.

On 20 June 2022, Keppel DC REIT announced the acquisition of Guangdong Data Centre 2 (Guangdong DC2) and Guangdong Data Centre 3 (Guangdong DC3) in Jiangmen, Guangdong Province in China, for about S$142.2 million each.

Guangdong DC2 and Guangdong DC3 are expected to be completed in H2 FY2022 and Q3 FY2023, respectively.

Source: Keppel DC REIT’s H1 FY2022 Financial Results Presentation

Source: Keppel DC REIT’s H1 FY2022 Financial Results Presentation

Currently, Keppel DC REIT’s balance sheet remains supportive for acquisitions as management continues to evaluate potential new deals in Asia Pacific and Europe.

The REIT’s gearing level came in at 35.3% in H1 FY2022 and its average cost of debt remains low at 1.9%.

The impact of rising interest rates on Keppel DC REIT will also not be significant as about 76% of its borrowings have been hedged into fixed debt with a weighted average hedge tenure of around 3.6 years.

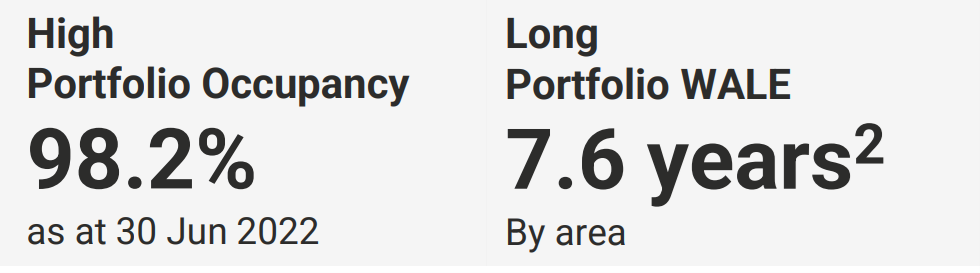

5. Portfolio occupancy and WALE remain stable

Source: Keppel DC REIT’s H1 FY2022 Financial Results Presentation

Source: Keppel DC REIT’s H1 FY2022 Financial Results Presentation

Keppel DC REIT’s portfolio occupancy rate remains healthy at 98.2% although it was lower than the 98.7% seen in the previous quarter.

This was mainly due to the non-renewal at Keppel DC Singapore 1, lowering occupancy from 93.1% to 92.6%, and downsizing on renewal at Basis Bay, lowering occupancy from 61.3% to 40.2%.

The data centre REIT’s management continues to see demand in Singapore despite the slight blip during the quarter.

Meanwhile, the portfolio’s weighted average lease expiry (WALE) is 7.6 years but is expected to increase to 8.0 years post-acquisition of Guangdong DC2 and Guangdong DC3.

Attractive dividend yield and growth opportunities

The downside risks with Keppel DC REIT remain, especially given some of the drag factors in Singapore.

However, it has a diversified data centre portfolio across nine countries and, with the strong demand for data centres globally amid a structural shift towards cloud services, this will benefit Keppel DC REIT.

Its healthy balance sheet position and earnings-accretive acquisitions could also boost its DPU going forward.

Keppel DC REIT currently has an attractive distribution yield of around 5.1%,especially for a pure-play data centre REIT that is less affected by recession risks in the near term.

Disclaimer: ProsperUs Investment Coach Billy Toh doesn’t own shares of any companies mentioned.