Investors are in the midst of studying results from earnings season, with many of the biggest names in US markets reporting their first-quarter numbers.

That’s very much the same situation in Singapore as the “Big Three” banks of DBS Group Holdings Ltd (SGX: D05), United Overseas Bank Ltd (SGX: U11), also known as UOB, and Oversea-Chinese Banking Corporation Limited (SGX:O39), better known as OCBC, reported their first-quarter numbers last Friday.

Dividend investors were interested to hear more from these companies, whose stocks pay out a reliable passive income stream in the form of regular dividends.

With all three banks seeing their share prices up so far in 2022, it was a great time to see how their respective businesses performed in the current volatile environment.

Here’s what investors need to know about the big banks’ latest numbers and which one – out of DBS, UOB and OCBC – came out on top.

Net profit for banks fall year-on-year

Across all three banks, net profit fell 10% on a year-on-year basis as the strong start to 2021 (coming out of the worse of the pandemic) made for difficult comps in the first quarter of this year.

On the bright side, though, the upcoming US Federal Reserve (Fed) interest rate hikes will be a strong tailwind behind the sails of all three.

While expectations for rate hikes earlier this year were at four or five hikes, that has now been readjusted – in the face of higher inflation – to seven Fed rate hikes.

Naturally, this should benefit their net interest income (NII) and net interest margins (NIMs) as the spreads between deposit rates and loan rates start to widen.

DBS: Fee income up

For Singapore’s biggest bank, DBS reported net profit of S$1.8 billion for the first quarter of 2022. While this was down 10% year-on-year, it was actually up 30% quarter-on-quarter.

Fee income for DBS was down 7% year-on-year on lower wealth management fees while net interest income saw a 4% year-on-year boost.

Loans were up 8% year-on-year while they also saw a 2% improvement quarter-on-quarter. While expenses were up 4% year-on-year, DBS maintained a healthy cost-income ratio of 44%.

DBS maintained its mid-to-single digit loan growth guidance for the rest of this year, meaning it’s likely that loan growth slows in the second half of 2022.

In line with its Q4 2021 earnings, DBS announced an interim dividend per share (DPS) for the first quarter of S$0.36.

UOB: Customer loans up 9% from year-ago period

As for UOB, the bank saw net profit after tax (NPAT) of S$900 million for the quarter, down 10% year-on-year.

However, the good news came from loan growth, which was up 9% year-on-year and 3% quarter-on-quarter at US$320 billion.

Looking at the bank’s performance by segment, the Group Wholesale Banking division saw the strongest year-on-year growth in operating profit – with a 17% expansion to S$939 million.

This was partially offset by Group Retail, with operating profit of S$470 million, which was down 18% year-on-year.

UOB, which has a strong footprint in Southeast Asia, continues to have confidence in the growth trajectory of ASEAN as its loan growth projections to mid-to-high single-digit loan growth is underpinned by accelerating domestic recoveries in regional countries.

The bank’s non-performing loan (NPL) ratio is at a manageable 1.6% and UOB does also have a buffer of S$1.2 billion in management overlays that can be used to offset any future deterioration in asset quality.

OCBC: ROE up 310 basis points

Similarly, OCBC saw net profit fall 10% year-on-year to S$1.36 billion but this figure was up a whopping 39% quarter-on-quarter.

OCBC’s NPL ratio dropped to 1.4% while its operating expenses were well-managed, falling 7% quarter-on-quarter to S$1.2 billion.

One of the highlights for OCBC was its low credit costs, which came in at 6 basis points (bp), down from 32bp for the whole of 2021.

Additionally, the bank’s Return on Equity (ROE) was an annualised 10.6% in the first quarter of 2022, which was up 310bp from the prior quarter.

Picking the long-term winner

As for the strength of the earnings, all three banks had a solid first quarter in terms of the key metrics that investors should watch.

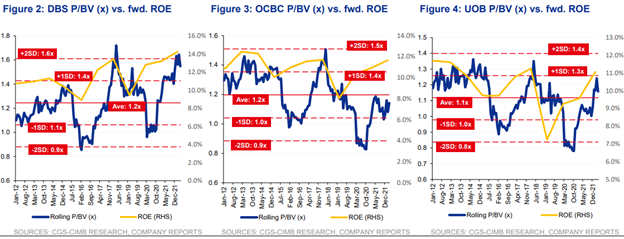

Going into the second half of the year, there are perhaps more tailwinds for OCBC and UOB, which are trading at lower price-to-book (PB) values than DBS (see below) and may see slightly stronger loan growth.

However, on the whole, investors should be thinking about which bank has the strongest franchise over a three-, five- and 10-year time horizon.

In that sense, it seems natural to think that DBS will continue to perform strongly and maintain its outperformance versus its two smaller peers.

Valuations from a PB perspective mean DBS is more expensive but the ROE improvement from DBS over the past few years has been stark.

Finally, DBS is best-positioned to benefit from higher US interest rates given its significantly larger deposit base.

In fact, DBS CEO Piyush Gupta guided that the bank expects to earn S$1.8-2.0 billion in incremental NII for every 100bp increase in the US Federal Funds Rate.

Overall, it was an earnings report card that came in line with what analysts were expecting. With robust balance sheets and the added benefit of rising interest rates, all three Singapore banks should continue to pay out reliable dividends for the foreseeable future.

Disclaimer: ProsperUs Head of Content & Investment Lead Tim Phillips owns shares of DBS Group Holdings Ltd.