Earnings season in the US is heating up. Earlier this week, The Coca-Cola Company (NYSE: KO) reported quarterly earnings and revenue that beat analysts’ expectations.

This was fuelled by price hikes and higher demand for its drinks. Coca-Cola exceeded Wall Street’s expectations in terms of both earnings per share (EPS) and revenue.

Based on a survey of analysts by Refinitiv, the market anticipated EPS of 64 US cents and revenue of US$10.8 billion.

However, Coca-Cola reported adjusted EPS of 68 US cents and adjusted revenue of US$10.96 billion.

So, for consumer staples investors, here are five key takeaways from Coca-Cola’s positive financial performance during Q1 FY2023.

1. Sales momentum continues as global unit case volume grew 3%

Unit case volume increased 3%, driven by away-from-home channels and market investments.

Developed markets saw mid-single-digit growth, while developing and emerging markets grew in the low single digits, led by China, India, and Brazil.

Growth in developing and emerging markets, however, was affected by the suspension of business in Russia.

The unit case volume performance was driven by the following:

Source: Coca-Cola’s earnings release Q1 FY2023

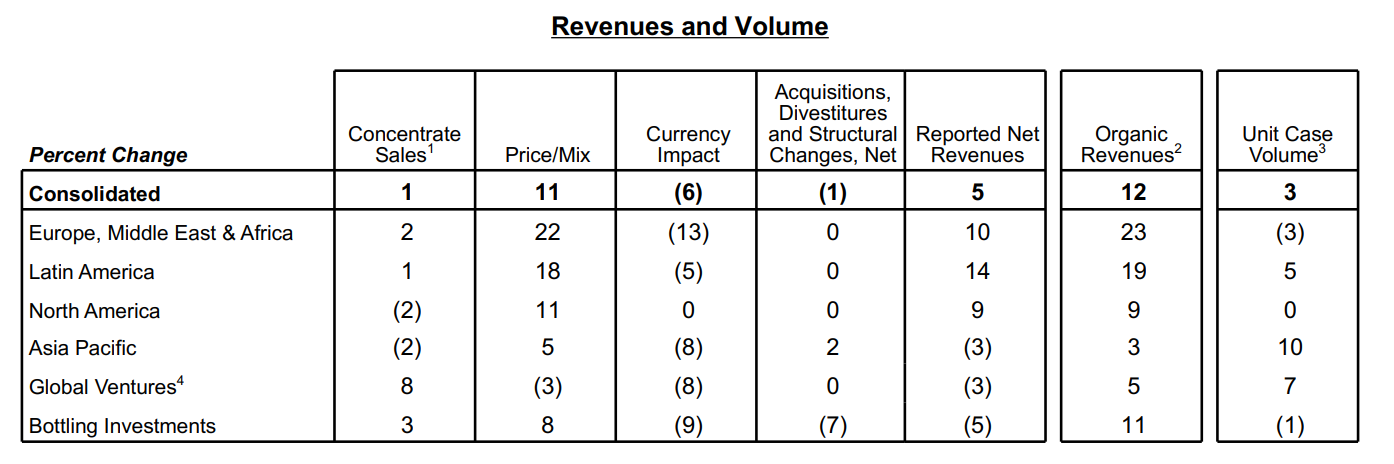

2. Net revenue grew 5% while organic revenue jumped by 12%

Source: Coca-Cola’s earnings release Q1 FY2023

Net revenues grew by 5% to US$11.0 billion, while organic revenues (non-GAAP) saw growth of 12%.

The revenue performance was driven by an 11% rise in price/mix and a 1% uptick in concentrate sales.

The discrepancy between concentrate sales and unit case volume, which trailed by two points, was mainly attributable to the scheduling of concentrate deliveries and the quarter having one fewer day.

3. Coca-Cola has strong pricing power

Coca-Cola’s average selling price (ASP) increased 11% yoy during Q1 FY2023.

The resilient demand for its sodas, despite multiple price increases undertaken to combat higher commodity and shipping costs, reflects Coca-Cola’s strong pricing power.

With little to no pushback from consumers to its price increases, Coca-Cola said in February that it would raise soda prices further this year globally but at a moderating pace even as rival PepsiCo Inc (NASDAQ: PEP) hit “pause” on price hikes.

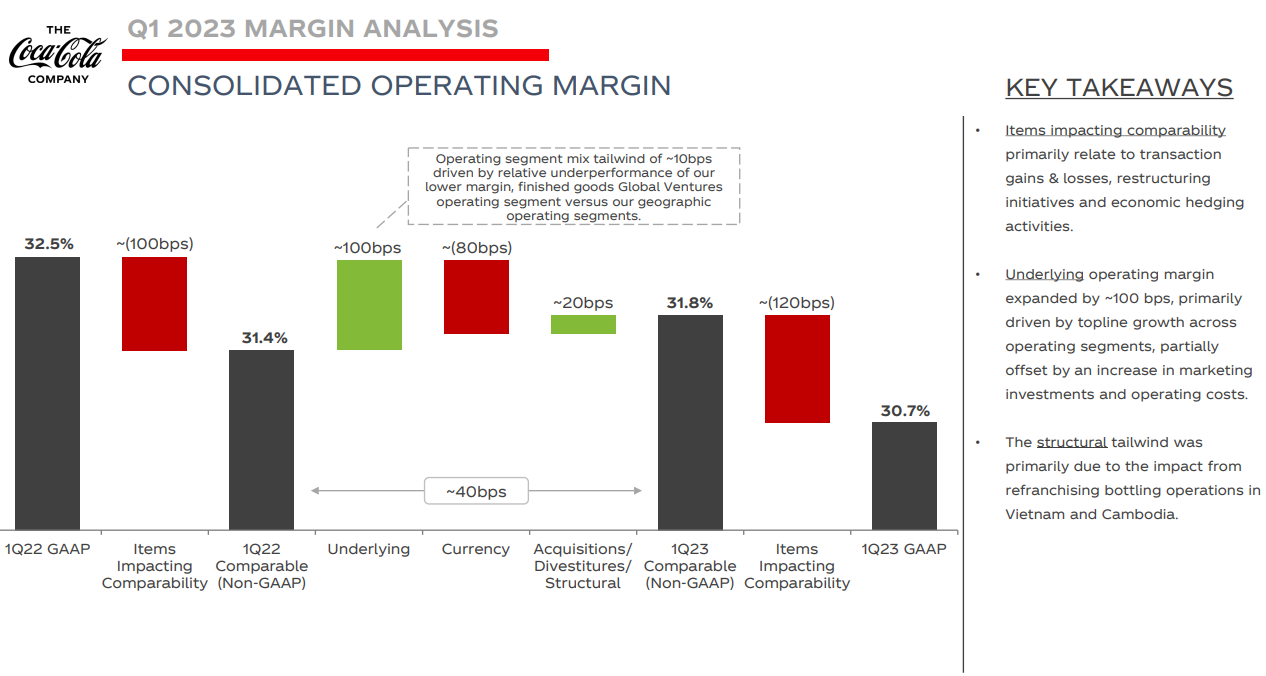

4. Higher operating costs hurt margin but remains at comfortable level

Although the average prices rose for its products, Coca-Cola’s operating margin was negatively impacted by elevated operating costs.

The operating margin for Q1 FY2023 fell to 30.7%, down from 32.5% in the previous year’s period, due to increased operating expenses, higher marketing expenditures, investments, and a robust US dollar.

During the conference call, company officials noted that freight charges and some commodity costs were stabilising but prices for sweeteners and juices were on an upward trajectory.

Source: Coca-Cola’s earnings release Q1 FY2023

5. Management maintains forecast for FY2023 despite inflationary pressures

The company reaffirmed its previous 2023 forecast, expecting organic revenue growth of 7% to 8% and a comparable EPS growth of 4% to 5% for the year.

This projection aligns with its Q1 FY2023 performance.

Furthermore, Coca-Cola anticipates that commodity inflation will impact its cost of goods sold by mid-single digits in 2023.

CFO John Murphy informed analysts during the company’s conference call that although oil spot prices and freight costs have decreased, higher prices for other commodities are persisting for a longer duration.

Invest in Coca-Cola’s brand power

Coca-Cola’s resilient earnings during Q1 FY2023, despite the increase in prices, reflects the brand power and customer loyalty.

The management team has maintained their outlook for FY2023 despite anticipating commodity inflation to continuing to put pressure on costs.

With its dominance in the soda market and the reopening in China, long-term investors should consider adding the brand power of Coca-Cola to their portfolio amid the market volatility.

Disclaimer: ProsperUs Investment Coach Billy Toh doesn’t own shares of any companies mentioned.