The big banks in Singapore have been reporting their earnings over the past week or so. Earlier this week was the turn of DBS Group Holdings Ltd (SGX: D05).

It reported before the market open on Tuesday (2 May), the first working day back after the long three-day weekend.

In short, it was a blowout quarter from Singapore’s biggest bank. So, for Singapore bank stock and dividend lovers, here’s what you need to know about DBS’s latest Q1 2023 results.

DBS net profit and ROE both hit record high

With bank earnings, it all comes down to net profit. On this front, DBS beat expectations, with its Q1 2023 net profit coming in at S$2.57 billion – up 43% year-on-year.

On a quarterly basis (from Q4 2022), its net profit was still up 10%.

Net interest income (NII), basically the interest spread between what DBS gets from loans and what they pay out on deposits, soared 69% year-on-year to S$3.38 billion. However, this figure was down 1% quarter-on-quarter from Q4 2022.

On the net interest margin (NIM) front, DBS saw a 104 basis point (bp) bump to 2.69%, and was up 8bp from the 2.61% recorded for Q4 2022.

Meanwhile, DBS’s Return on Equity (ROE) during the first quarter hit a record high of 18.6%, a phenomenal figure for a bank.

DBS fee income rises, cost-income ratio dips below 40%

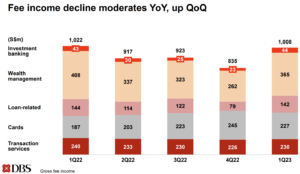

DBS had broadly seen sequential declines from Q1 2022 up to Q4 2022, in terms of its fee income. However, in its latest Q1 2023 period, this trend reversed (see below).

Source: DBS Q1 2023 earnings presentation slides

So, while only slightly down on a year-on-year basis, the S$1 billion in fee income for Q1 2023 was up strongly from Q4 2022.

Indeed, management said fee income was actually up year-on-year in February and March, with strong growth in its cards division.

A reversal of declines in its wealth division also helped power fee income in the last two months of the quarter.

Meanwhile, the bank’s cost-income ratio was 38% during Q1 2023. That was down a full five percentage points from 43% in Q4 2022 and was down from 45% in the year-ago period.

NIM likely peaked in Q1 2022; guiding for moderate loan growth

DBS CEO Piyush Gupta, in prepared remarks, did note that DBS’s NIM likely peaked out in Q1 2023.

Having said that, while he expects the NIM decline to be gradual, overall NIM for 2023 is still expected to be in the range of 2.05-2.1%.

On the ROE front, DBS is aiming for full-year 2023 ROE to be 17% with a cost-income ratio below 40%.

Loan growth guidance was revised down slightly, from mid-single-digit growth to 3-5% growth and its fee income growth is expected to be in the high-single digit range for 2023.

With new money flowing in during the March banking crisis in the US and Europe, DBS looks well positioned to benefit from a larger deposit base.

However, many investors now feel that the interest rate hiking cycle is coming to an end – which explains why DBS shares were down despite announcing record results.

Even so, the bank remains extremely well capitalised and can easily afford to pay out its quarterly dividend per share (DPS) of 42 Singapore cents.

At its current share price, DBS is offering investors a 12-month forward dividend yield of 5.2%.

Disclaimer: ProsperUs Head of Content & Investment Lead Tim Phillips owns shares of DBS Group Holdings Ltd.