Singapore’s real estate investment trusts (REITs) have been known for “splashing the cash” on overseas acquisitions.

Last year, foreign deals by REITs in the Lion City hit a record high of S$12.3 billion in value. From data centres to office blocks and logistics properties, Singapore REITs were clearly hungry for assets.

One of the main reasons for this is that Singapore is a small market. Thus, in order to grow their portfolios and distribution per unit (DPU), Singapore REITs don’t have much of a choice but to venture overseas.

Indeed, that point was driven home by the recent acquisition of a logistics development in the UK by locally-listed Frasers Logistics & Commercial Trust (SGX: BUOU), also known as “FLCT” for short.

Here’s what Singapore REIT lovers and dividend investors need to know about the latest acquisition by one of the country’s largest industrial and logistics property owners.

Sizeable logistics acquisition with anchor tenant

On Saturday (25 June), FLCT announced that it had agreed to purchase a prime freehold logistics development in the North West of England for £101 million (S$171.7 million).

This would be FLCT’s fourth logistics and industrial (L&I) development in the UK (and sixth property in the UK overall). The newest L&I property will have a total lettable area of 667,185 square feet.

Yet investors should be aware that the development is only expected to be completed in the second half of 2023, with the property being built to high specifications and sustainability standards – including being certified as net zero carbon in operation for base build works.

After completion, FLCT has already secured automobile manufacturer Peugeot Motor Company Plc as an anchor tenant with a lease term of 15 years.

From there, Peugeot will operate its national distribution centre for the UK. FLCT will also benefit from five-yearly, upward-only rent reviews.

Increasing exposure to logistics and industrial

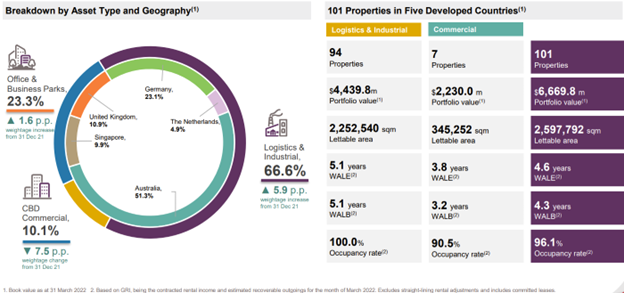

From a portfolio perspective the deal will see FLCT raise its exposure to the UK to 13.0% (of total portfolio value) from 10.7% prior to the purchase.

With regards to its weighting towards L&I, this will also increase from the current 66.3% to 67.1% post-acquisition.

In terms of weighted average lease expiry (WALE), as of 31 March 2022, the acquisition will also see its portfolio’s WALE lengthen out from 4.6 years to 4.8 years post-acquisition while its portfolio’s occupancy rate will improve marginally to 96.2% (see below).

Source: Frasers Logistics & Commercial Trust H1 FY2022 investor presentation

Exciting growth market in the UK

For investors, it’s clear that the latest purchase from FLCT is galvanising its commitment to L&I space in Europe and it’s easy to see why.

According to CBRE, supply of warehouse space in the North West at the end of Q1 2022 fell by 11.0% quarter-on-quarter to 1.8 million square feet – resulting in a vacancy rate of just 1.3%.

Furthermore, the demand for space is there as the UK government’s initiatives to drive investment to areas outside London continues.

Based on JLL research, overall L&I rental growth in the UK will increase by around 5% annually from 2022-2026.

Solid acquisition for FLCT

Overall, it looks to be an astute purchase for FLCT as it continues to grow its footprint in Europe.

The funding for the deal will come from existing debt facilities and proceeds from its disposal of Singapore property Cross Street Exchange.

Besides that, FLCT had a comfortable gearing ratio of 33.1% as of the end of March 2022 (prior to its announcement of the Cross Street disposal).

While there are some concerns over the state of the economy in Europe and a potential recession, the anchor tenant and five-yearly reviews of rent increases does provide unitholders with some visibility on income streams.

At its current price of S$1.36, FLCT shares are offering investors a 12-month forward dividend yield of 5.7%.

Disclaimer: ProsperUs Head of Content & Investment Lead Tim Phillips doesn’t own shares of any companies mentioned.