Stock markets globally have seen some strong selling this week on fears ranging from rising interest rates to expensive valuations.

However, for long-term investors, that’s all noise. In the real world, companies are going about trying to grow their businesses as usual.

Coming out of the worst recession for the global economy since World War II, businesses worldwide are preparing themselves for an uptick in demand once the Covid-19 vaccines are widely rolled out.

There was often talk of “stay-at-home” winners during the pandemic but, on the flipside, there’s definitely going to be a brighter outlook for a number of strong businesses once economies fully reopen.

Despite that, I’m still looking for already-solid stocks (pre-pandemic) that are resuming their long-term growth trends and aren’t simply expecting a temporary bump in growth.

With that, here’s one stock that I think will benefit greatly from a wider rollout of the Covid-19 vaccine.

Put it on the Mastercard

When you travel overseas (before the Covid-19 pandemic put us all in lockdown), the likelihood is you would have been spending money on a credit card.

And it’s likely that card was issued by Mastercard Inc (NYSE: MA), one of the largest card issuers and payment processors in the world.

Mastercard, along with rival Visa Inc (NYSE: V), basically have a global duopoly in the credit card payments space.

Yet one of the big reasons why Mastercard is set to benefit is that a significant part of its revenues (and subsequently profits) comes from cross-border processing fees, i.e. people paying for stuff when they travel.

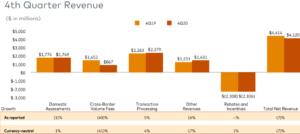

For example, in its latest fourth-quarter 2020 results, Mastercard reported a big 40% year-on-year drop in cross-border volume fees (see below).

That continued to be one of the biggest detractors from an otherwise respectable set of results.

Source: Mastercard Q4 2020 earnings presentation

That drop in cross-border volume fees drove a 15% year-on-year drop in net income to US$1.8 billion in the fourth quarter of 2020.

Waiting for borders to reopen

In fact, the closure of borders during the whole of 2020 has weighed on Mastercard, perhaps more so because it gets more of its revenue from international markets whereas rival Visa is a more US-centric company.

Around 70% of Mastercard’s gross dollar volume (GDV) in its latest quarter came from outside the US – basically capturing where its cards are used most.

Once borders start to reopen and people start spending on their cards overseas, the higher-margin cross-border business should start to outperform given the pressure the growth rates have been under for nearly a year now.

Going cashless for the long term

For investors who believe in both a cash-less society and a return to cross-border travel eventually, Mastercard stock looks set to be one of the biggest beneficiaries of those broader trends.

With shares up around 6.5% over the past month, Mastercard’s solid business looks set to improve even further once global economies reopen.

Disclaimer: ProsperUs Head of Content Tim Phillips doesn’t own shares of any companies mentioned.