All investors have probably seen the memes doing the rounds this week: Credit Suisse, Debit Suisse. That’s because Credit Suisse was part of a US$3.2 billion takeover by Swiss rival UBS Group.

Announced over the past weekend, following signs of trouble at Credit Suisse, a takeover deal was welcome.

However, what came with it was less welcome. That’s because Credit Suisse’s Additional Tier-1 (AT1) bondholders got the short end of the stick.

In the process of the takeover, they were wiped out while equity shareholders were spared. That sparked a level of panic in Asian markets on Monday (20 March) when they opened.

So, here’s why the Credit Suisse takeover matters for Singapore bank investors and what they should know.

Debt trumps equity, no?

Typically in a company’s structure of ownership, debt holders have first dibs on any recovery of assets – at the expense of equity holders (also known as shareholders).

However, in the case of Credit Suisse, that norm was turned on its head as AT1 bondholders – ahead of equity holders in the capital structure – were left with nothing.

Meanwhile, shareholders are receiving US$3.2 billion in the agreed deal that was brokered by the Swiss National Bank.

In Asia, this news spooked shareholders of AT1 bonds in regional banks. For example, HSBC Holdings plc (SEHK: 5) saw its US$2 billion AT1 bond fall more than five cents to below 90 cents on the dollar on Monday.

Singapore strong

How about Singapore banks? They appear to be less affected by the scare surrounding AT1 bonds given their return on equity (ROE) profiles are extremely robust.

Indeed, all three Singapore banks – DBS Group Holdings Ltd (SGX: D05), United Overseas Bank Ltd (SGX: U11), and Oversea-Chinese Banking Corporation Limited (SGX: O39) – all have ROEs of around 12.5%.

That’s in stark contrast to Credit Suisse’s ROE of negative 16%, given the Swiss bank’s concentrated reliance on commissions and fee income.

Banks here are also well-capitalised and possess healthy capital buffers. They’re also vastly profitable, as investors have borne witness to in 2022 with increasing net interest income (NII).

Fees vs. contagion

That doesn’t address the concerns around contagion, though.

As many commentators have pointed out, rumours in the banking sector can spread like wildfire and ultimately prove destructive – even to well-capitalised and robust banks.

In Singapore, though, the Monetary Authority of Singapore (MAS) came out on Monday to reassure investors that:

“Sinapore’s financial system remains stable and financial markets continue to function in an orderly manner”.

The MAS also pointed out that Credit Suisse operations in the city state would continue without any interruptions.

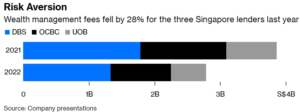

As far as Singapore banks’ own profit outlooks go, the flight from Credit Suisse could see capital end up in local bank’s wealth management arms.

But, as an opinion piece in Bloomberg this week pointed out, that might not help the Singapore banks much. That’s because fee income has dropped as investors are sitting in cash (see below).

Source: Bloomberg

With funding costs continuing to rise, the upshot is that this could crimp profitability.

Bright spot in China

Overall, while Singapore banks are highly-integrated into the global financial system, they also have exposure to China – where the reopening story continues to play out.

That could help soften the blow from what looks increasingly like an inevitable global recession.

In the meantime, Singapore investors should closely monitor the evolving banks situation to see whether this contagion spreads beyond the US and Europe.

Disclaimer: ProsperUs Head of Content & Investment Lead Tim Phillips owns shares of DBS Group Holdings Ltd.