For investors, the latest survey of the US Purchasing Managers Index (PMI) indicates that there is no end in sight for the pandemic-led global supply chain disruption.

That’s because lead times for factories in the US continue to lengthen to a record.

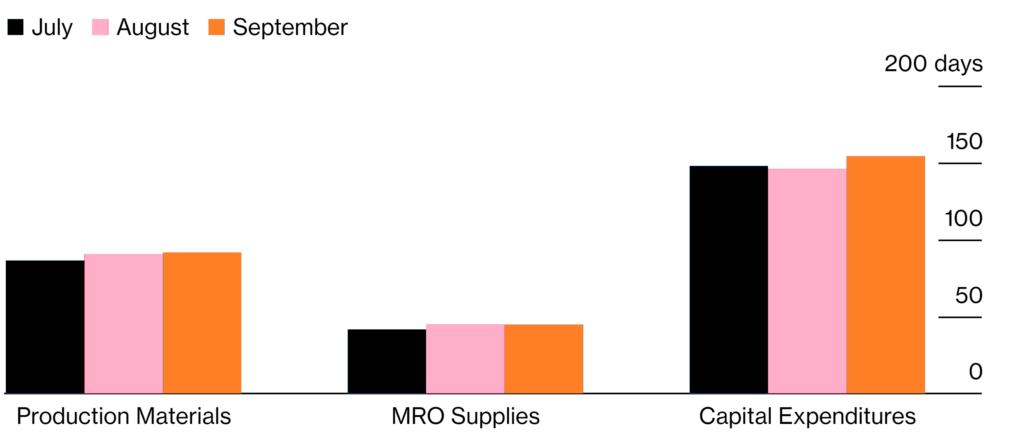

The Institute of Supply Management’s latest survey shows that the average lead time for production materials in September increased to 92 days, the highest on record since 1987.

Wait times for supplies used in maintenance, repair and operations (MRO) equalled its record of 45 days while factories are having to wait 154 days to upgrade or replace their manufacturing equipment.

Fragile supply chain comes under pressure

To put into perspective, the supply chain disruption first emerged prior to the pandemic when the US-China trade tensions first started under President Donald Trump, with the introduction of tariffs and sanctions on Chinese companies.

The shift in global trade at that time already put an initial stress on the global logistics capacity.

Then came COVID-19, which put the world under the “Great Lockdown”. Manufacturing activity came to a sudden stop, shipments were cancelled, manufacturing capacity cut and workers displaced.

But thanks to an unprecedented massive fiscal stimulus push in the US, supported by the rollout of global vaccination programme, we saw pent-up demand.

However, it turns out that restarting the manufacturing machine after a lockdown isn’t as straightforward. The interconnected global supply chain requires predictability and precision.

We all know that a chain is only as strong as its weakest link and when it comes to the state of our global chain, weakness is everywhere.

We have not even started talking about the China’s recent energy crisis, which would have a knock-on impact to supply chains, further crippling the global economic recovery.

Disruption on supply chain will push price index up further

The supply chain crunch will lead to a more heated pace of inflation, at least in the near-term. This could have a profound impact on the global economic recovery that has only started to rebound at the back of massive fiscal stimulus package and easy monetary policy.

To have an understanding on how bad the impact on prices are so far, we can take a look at the Producer Price Index (PPI) in China, which rose 9.5% from a year earlier in August.

It was the fastest pace recorded since August 2008, driven by roaring new material prices.

My view is that this will be temporary given that the disruption we witnessed today is mainly from the restarting of the manufacturing sectors.

A period of adjustment is unavoidable but the return of the services industry will also help to shift some of the spending away from spending on goods.

Long-term investors should remain focused on companies that have shown to be resilient despite the uncertainties over the last two years.

Some examples can be found at Tim’s latest “5 Top Stocks to Buy in October” here. These are some of the companies that possess solid long-term prospects.

Source: Bloomberg, Institute of Supply Management