-

The Dollar index corrected as expected based on our previous report and has see sustained support at 106.00 support level (see link here). The corrective action in the Dollar Index (DXY) is likely to continue in the near-term. However, we continue to maintain our target of 112.00 for the Dollar Index (DXY) over the mid to longer-term period.

-

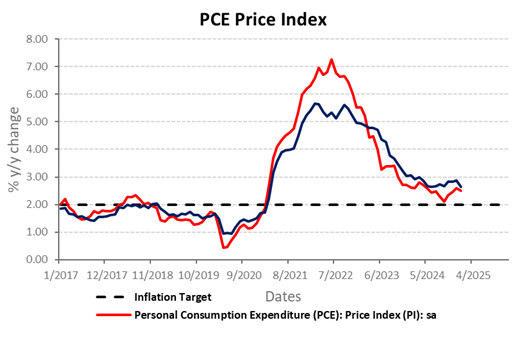

Last week’s PCE figure came bearing good news to the Feds as PCE numbers fell to 2.5% YoY in Jan 25. However, figures were attributed to dip in consumer spending from Dec 24 – Jan 25

-

We continue maintain dollar strength in the long-term but correction or rangebound scenario will continue in the near-term.

-

Aussie gain slightly after severely weakened against the Dollar last week. The gain was attributed to the better than expected data in China’s Caixin Manufacturing PMI.

-

Dollar target over the long-term will be at 112.00, with correction likely to be on the table. Key support levels to watch will be at 104.54-105.10.

-

EURUSD long-term may look at a possible parity at 1.0000 against the dollar. Reason being the weak effect of the European economy and the prospect of Germany’s government after its election last week.

-

AUDUSD likely to strengthen to 0.6300 against the dollar as China PMI has positive effect on the Aussie. Rate cute may have little effect on the Aussie yet.

-

USDJPY will see likely rebound as the next rate hike by the BOJ is likely to be far away, as far as end Q3. Hence, we remain solid on the rebound of USDJPY, targeting 154.00.

US dollar was supported by stable PCE numbers and Trump’s uncertainty on Tariffs

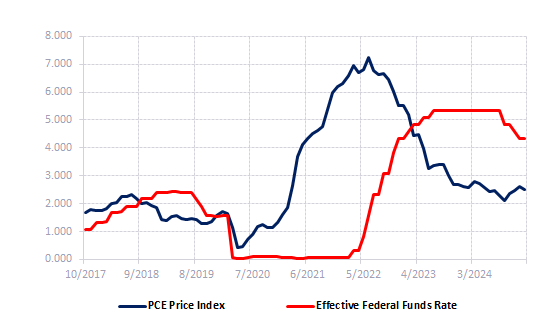

The latest US PCE number rings good news to the market after core PCE slows to 2.5% YoY, closing into the target of Fed’s 2% target. The prospect of rate cut is still on the table and we maintain that there will be 2 cuts cut this year, estimated to be in end Q3 and Q4. Despite the increased probability in rate cuts due to slower consumer spending and healthy disinflation growth, the dollar will maintain its dominance in the mid-term as the market is showing its fear of President’s unpredictable stance on Tariffs. The decrease in PCE numbers shows that the rate cut has advanced its objective and unless core PCE drops below 2.3%, the Fed may hold on to a rate cut in near-term, which strengthen the prospect of higher dollar.

The Euro against the dollar will likely weakened further in the mid to long-term as 1.) ECB rate cut is likely to go ahead and 2.) The increase tariffs on Europe will increase further risk of weakened Euro. 3.) The uncertainty after the German election will pile on the weakness of the Euro. Long-term wise, there is a possible parity for the Euro against the dollar.

We still reiterate the Dollar strength in the near-term and the ability to cross past 110.00 and reach 112.00 going forward, after reaching our major target at 110.00. However, we also reiterate our view that near-term correction is still on the table. However, strong correction if any should and will likely to be supported above the 100.00 psychological level.

Bank of Japan is confident of raising its interest rate once again

The Japanese have beat expectation and rose rate to 0.5% in Jan 25 last month and came as a surprise. However, we believe that the rate will likely to increase to 0.75% again in Q3 as inflation outlook in Japan has rose steadily.

The Rate raise has met our forecast on Dollar Yen pair and reaches our target at 150.00, based on our report dated 21 Jan 25.

Fig 1- PCE number remain stable, with disinflation intact

Fig 2- PCE VS Fed Fund rate – Objective of rate cut met

Please refer to the disclaimer here.