-

Trump is back and the dollar fell after reaching the peak of 110.17, which meet our expectation of our previous report mentioning the possible strength going past 110.00. The corrective action in the Dollar Index (DXY) is supported at 108.00. Hence, we maintain our target of 112.00 for the Dollar Index (DXY)

-

Bank of Japan’s decision to raise rate is likely coming to past after the index after the better than expected CPI data from the US, which may prompt the Federal reserve to cut rate and in turn, making a lucrative bet to raise rate by the BOJ

-

We maintain dollar strength in the long-term and may suffer some form of corrective action before heading to 112.00 as the potential rate raise by the BOJ may trigger another wave of unwinding of the Yen carry trade.

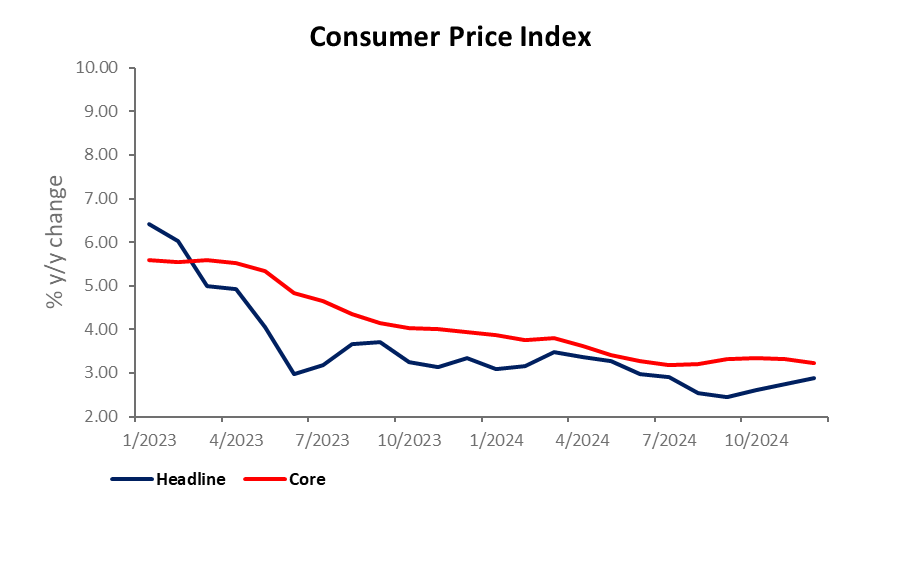

US better than expected CPI quench the fire for any doubt on the rate decision

The latest US CPI rings good news to the market after core inflation slows to 3.2% YoY. However, the headline inflation ticks up to 2.9% as food and energy prices rose, especially energy when oil soars more than US$79.00 per barrel. Regardless the head line inflation, the prospect of rate cut is surging and this will likely to be in line with President Trump desire in his first 100 days in office. With further cutting down unwanted regulation, climate changes agenda that caused prices to rise and delayed tariffs with its largest trading partner, China, the inflation pressure may eased slightly going forward. Hence, the dollar may reprice a correction but not reversal.

We still reiterate the Dollar strength in the near-term and the ability to cross past 110.00 and reach 112.00 going forward, after reaching our major target at 110.00. However, we also reiterate our view that there may be a reversal at 112.00 or at 110.11, which resembles the sell-off in early 2016 when Trump took office. However, the degree of its potential reversal is likely to be milder and may be able to stay supported above 100.00 psychological level.

Bank of Japan is confident of raising its interest rate once again

The Japanese enjoyed a raise in wage growth but 2% inflation rate has net the wage growth effect in terms of purchasing power as Tokyo’s core inflation rose 2.4%YoY. Softer export also take a toll on the export oriented economy. While BOJ’s rate hike may seems to be an unknown due to the Federal reserve’s no rate hike in January and a Trump’s presidency on trade tariffs may spurs Ueda’s consideration of a no hike in January. If that’s the scenario, the rate hike by the BOJ may be delayed till March 2025.

The near-term target of USDJPY at 157.00 has been achieved. With the uncertainty on the BOJ, we believe near-term correction is likely to be mild and will has seen slight bullish strength at 154.62 key support. Rate raise may cause the Dollar Yen pair to slide further to 150.00 or 148.00.

Uncertainty clouding the Bank of England, rate cut is out for now.

The Bank of England is battling one of the toughest time now. Sticky inflation, hindered spending by the government and the elevated US dollar rate has caused the pressure on the pound. Which we believe is one of the crucial factor which the Bank of England has turned dovish.

To add fuel to the fire, Gilt yields have surged significantly in recent months, with the 30-year yield reaching 5.3%, its highest level since 1998. The 10-year yield has also risen sharply, though at 4.7%, it remains within the range seen in the early 2000s. Factors driving this upward movement include Labour’s spending plans, persistent inflation, higher US rates, and supply pressures. While we anticipate gilt yields to decline later in the year, these contributing factors are likely to persist, delaying a reversal.

As such, we remain bearish on GBPUSD with a near-term target of 1.2000.

Fig 1- US CPI – Disinflation! Phew!

Technical outlook on Dollar index – Looking at a larger degree correction if 108.00 is broken

Source: Tradingview

The dollar index continue to see uptrend but recent momentum and price action is pointing towards a correction going forward. Stochastic Oscillator shows an overbought condition and Directional movement index is displaying weakness in the bull after both ADX and DM+ declined.

This is in-line with our previous report titled “The Red wave is backing the dollar strength, 105.00 target exceeded” where the bulls will die off at/near 110.58 or 112.00 resistance, potentially leading to a reversal. Such a reversal would resemble the post-Trump victory pattern in 2016, which saw a clear bearish shift by January 2017. We believe that 112.00 is achievable but with correction first. Then we may see a shift in trend after Feb 2024.

Please refer to the disclaimer here.