Earnings season started last week and Singapore REITs (S-REITs) are among the first to report their results.

Last week, office-focused REIT, Keppel REIT (SGX: K71U) reported its earnings for H2 FY2022 (for the six months ending 31 December 2022).

Keppel REIT owns a S$9.2 billion portfolio of prime commercial assets with 78.5% exposure to the Singapore market.

Among some of the commercial properties under its umbrella are Marina Bay Financial Centre and One Raffles Quay.

So, for S-REIT investors looking to benefit from the “return-to-office” trend, here are five key takeaways from Keppel REIT’s latest results.

1. Net property income for FY2022 edged higher

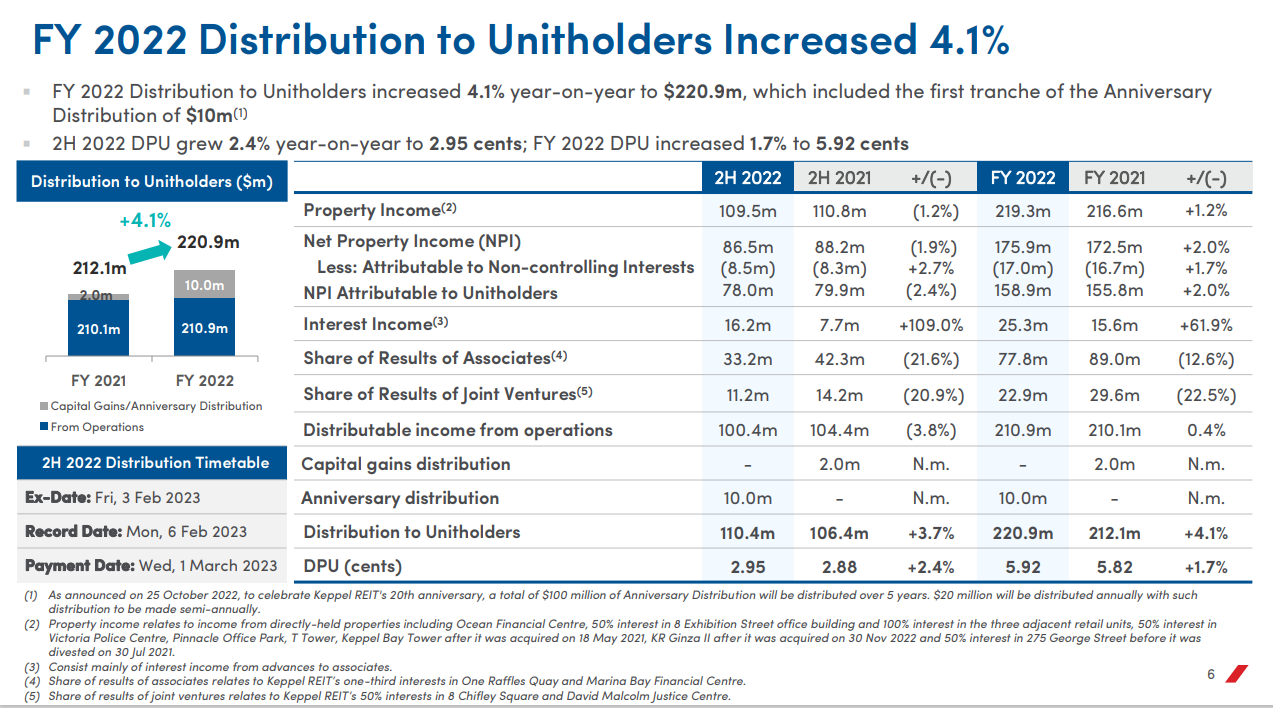

Keppel REIT reported a decline in its net property income (NPI) of 1.9% year-on-year (yoy) to S$86.5 million for H2 FY2022.

This was mainly due to the absence of contribution from 275 George Street in Australia following the divestment in July 2021.

However, the NPI for fiscal year FY2022 was up by 2.0% yoy to S$175.9 million.

The improvement was mainly due to a full-year contribution from Keppel Bay Tower, which was acquired in May 2021, as well as higher NPI from Ocean Financial Centre in Singapore and Pinnacle Office Park in Sydney.

While the Australian market dragged on its earnings recovery, Keppel REIT’s strong performance in its Singapore portfolio helped to offset this lower income, particularly Ocean Financial Centre and Keppel Bay Tower.

The strong performance of Keppel REIT is impressive given the increasing layoffs seen among tech tenants in Singapore.

2. DPU increased, supported by anniversary distribution

The distribution to unitholders increased 4.1% yoy to S$220.9 million, which includes the first tranche of the Anniversary Distribution of S$10 million.

Previously, Keppel REIT announced that it would distribute a total of S$100 million to celebrate its 20th anniversary in 2026.

Under the Anniversary Distribution, S$20 million will be distributed to unitholders annually over the next five years on a semi-annual basis.

This amount will come from the REIT’s accumulated gains over the next five years.

This will support the rising DPU for Keppel REIT.

Source: Keppel REIT’s H2 FY2022 and FY2022 Financial Results

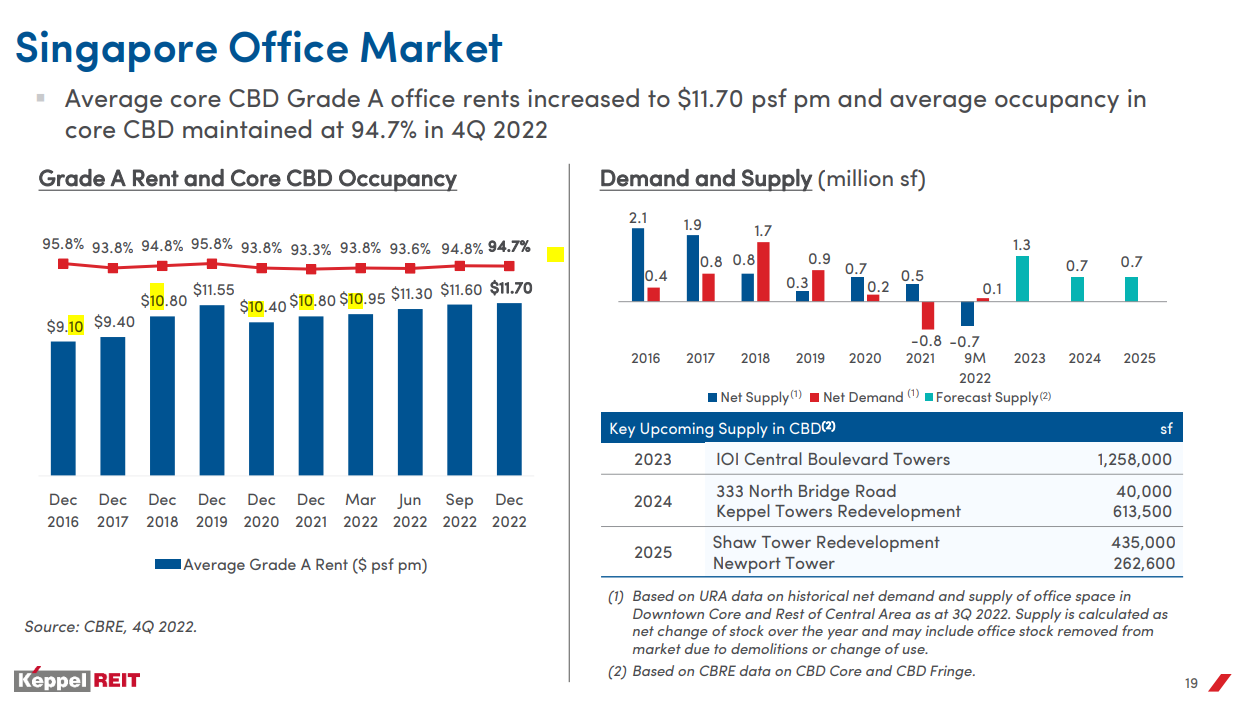

3. Positive rental reversion for Singapore portfolio

Keppel REIT’s portfolio recorded rental reversions that were up by 10% for the FY2022, supported by positive rental reversions of 23.4% for its office assets in Singapore’s central business district (CBD) in Q4 FY2022.

According to management, the REIT expects reversions to be in the “mid to higher single digits” for leases expiring in 2023.

Average core CBD Grade A office rents in Singapore increased to S$11.70 psf per month and average occupancy in core CBD properties was maintained at 94.7% in Q4 FY2022.

Source: Keppel REIT’s H2 FY2022 and FY2022 Financial Results

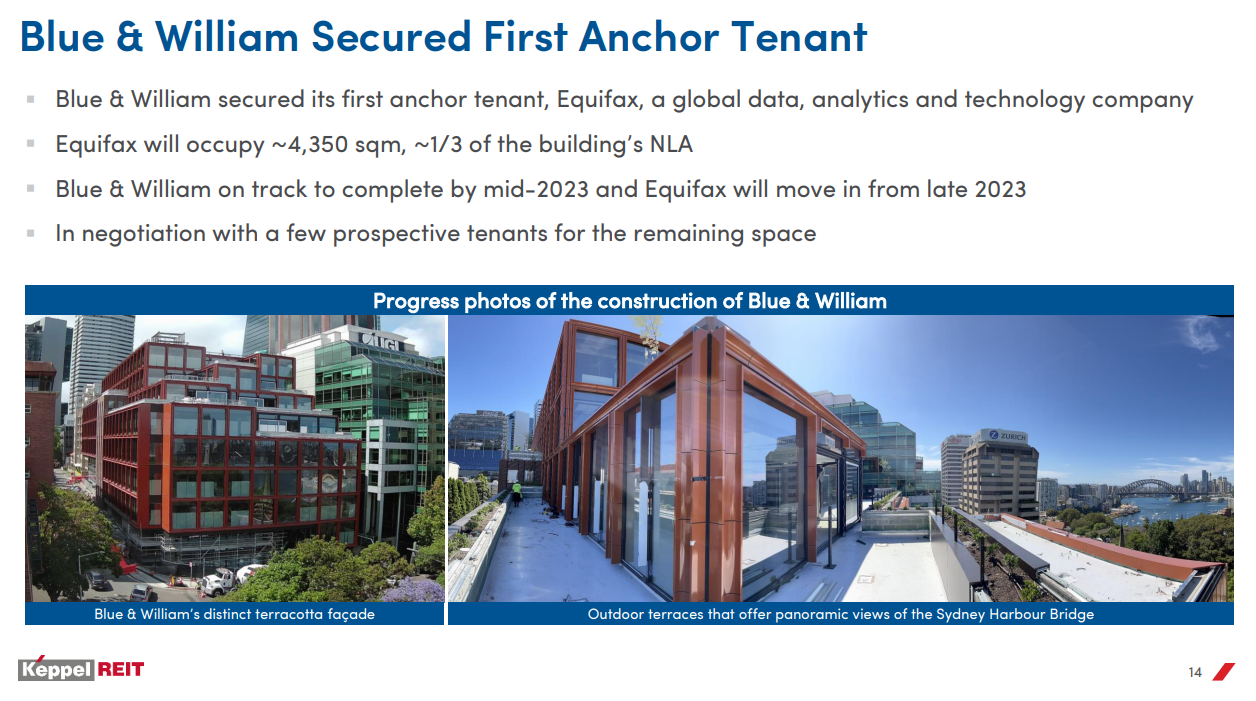

4. Expansion plans remain on track

The development project, Blue & William, has secured its first anchor tenant, which will be occupying one-third of the property.

The building is slated for completion by mid-2023, which will boost longer-term earnings for Keppel REIT.

Source: Keppel REIT’s H2 FY2022 and FY2022 Financial Results

Aside from that, Keppel REIT also expanded its footprint into Japan with the acquisition of a 98.47% interest in a freehold boutique office building in Tokyo’s Ginza district.

In my previous article in December, I was confident that the entry into the Japan market would be a positive boost to investors in the long term.

5. Balance sheet remains strong despite rising interest rates

Just like most REITs, Keppel REIT will see higher funding costs amid the rising interest rate environment.

However, with an aggregate leverage of 38.4% as at end-FY2022, its all-in interest cost averaged 2.29% with funding cost in Q4 FY2022 reaching slightly above 2.5%.

Management has also taken proactive measure to increase its fixed rate borrowing to 76% of its total debt while 76% of its debt that was expiring in FY2023 has been extended to FY2028.

As a result, its all-in funding cost will trend towards 3.0% given the rising interest rate but that remains manageable.

Strong portfolio and expansion to support DPU

Despite the challenging outlook for REITs, Keppel REIT is likely to maintain its strong distribution yield of around 6.0%.

This is supported by its expansion in Japan and development in Sydney, which is expected to boost income towards the end of FY2023.

The strong portfolio in Singapore, as evident by the increase in the valuation of its Singapore portfolio, will also support growth.

As of 31 December 2022, the Singapore portfolio’s valuation was up by 2.3% to S$7.2 billion, compared to S$7.0 billion as of 30 June 2022.

This is also reflected by the Singapore market’s occupancy rate of 94.7% in Grade A office properties in the CBD area.

Disclaimer: ProsperUs Investment Coach Billy Toh doesn’t own shares of any companies mentioned.