Amid all the stock market volatility in the US, Singapore’s stock market is proving to be a relative safe haven.

That’s because there are many real estate investment trusts (REITs) listed here that pay regular dividends.

While they may experience some short-term pressure from rising interest rates, more broadly REITs can still perform well even amid an environment where debt becomes more expensive.

Some of Singapore’s biggest REITs have been reporting their latest quarterly earnings over the past month or so, giving investors an idea of what the outlook is like as the US Federal Reserve starts raising rates next month.

One of Singapore’s largest REITs – and a constituent stock of the Straits Times Index (STI) – is industrial and data centre property owner Mapletree Industrial Trust (SGX: ME8U).

It reported its third-quarter fiscal year (FY) 21/22 earnings (for the three months ending 31 December 2021) on 25 January. Here are five key takeaways that dividend investors should take note of.

1. Dividend up over 6%

Mapletree Industrial Trust announced that its distribution per unit (DPU) – in other words its dividend – for the period was 3.49 Singapore cents, up 6.4% year.on-year.

This also happened to be up marginally quarter-on-quarter, from the DPU of 3.45 Singapore cents for the second quarter of FY21/22, and came on the back of an enlarged unit base from an equity fund raising earlier in the year.

Alongside this increase in the DPU was a 10.4% year-on-year increase in distributable income during the reported period to S$89.5 million.

2. Gross revenue and NPI both up over 20%

For Q3 FY21/22, Mapletree Industrial’s gross revenue and net property income (NPI) both saw impressive growth.

Gross revenue for the period was S$162.4 million – up 31.3% year-on-year – while NPI climbed 24.1% year-on-year to S$122.7 million.

These increases were down to contributions from the sizeable acquisition of a portfolio of 29 data centres in the US and a separate data centre transaction in the US state of Virginia. Both deals closed by the end of July 2021.

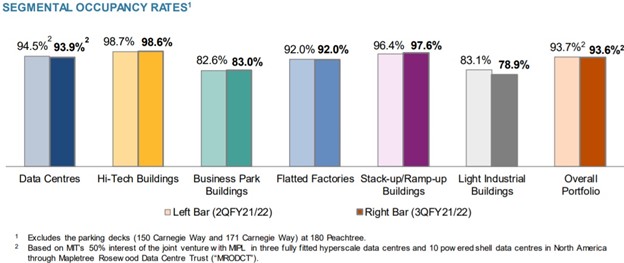

3. Portfolio occupancy down marginally

As with any REIT, portfolio occupancy is a closely-watched metric. In Mapletree Industrial’s case, the latest quarter did see portfolio occupancy drop to 93.6% sequentially from 93.7% in Q2 FY21/22.

This was mainly due to its data centres segment, which saw portfolio down 60 basis points to 93.9% in Q3 FY21/22 (see below).

Source: Mapletree Industrial Trust Q3 FY21/22 earnings presentation

Management attributed this drop to the impact of the addition of the portfolio of 29 US data centres, which had a lower average occupancy rate of 87.4%.

However, this was partially offset by better occupancy rates in its Singapore business park buildings and stack-up/ramp-up buildings.

4. Resumption of Distribution Reinvestment Plan

One other thing of note was that Mapletree Industrial Trust announced that it would be resuming its Distribution Reinvestment Plan (DRP) for the most recent quarter.

That allows investors to either take their distribution in cash or in new units. The last time the REIT offered this option was in Q4 FY18/19.

Management said the offer of new units via the DRP would allow Mapletree Industrial to strengthen its balance sheet and help finance progressive funding needs for development projects, while also allowing it to pursue growth opportunities.

The fact that it had a gearing ratio of 39.9% (as of the end of December 2021) also means the DRP could allow it to reduce its leverage ratio if it wished to.

5. Well-managed debt profile

With interest rates rising, how REITs manage their debt profile is crucial. Thankfully, for Mapletree Industrial Trust investors, it has a fairly responsible attitude towards managing its debt.

As of the end of 2021, the REIT had a weighted average all-in funding cost of 2.3% while its interest coverage ratio (ICR) was a comfortable 6.4 times.

During the quarter, the REIT also took action to ensure a higher percentage of its total debt was at fixed rates.

As a result, just shy of 80% of its debt was fixed as of 31 December 2021, versus just 57.7% as of 30 September 2021.

Another solid quarter but monitor recovery

Overall, it was another stable quarter for Mapletree Industrial Trust. Management did say that business sentiment in Singapore has improved but that lingering uncertainty remains given the Omicron Covid-19 variant.

How fast the economy can recover in the face of this is still in doubt but a lift in the moratorium for Singapore data centres could provide the REIT with opportunities in future.

Meanwhile, in the US while average asking rental rates decline in both primary and secondary markets, management said supply chain disruptions could constrain data centre development and therefore offset potentially negative impacts.

Mapletree Industrial Trust is currently trading on 12-month forward dividend yield of 5.4% given its latest unit price of S$2.55.

Disclaimer: ProsperUs Head of Content & Investment Lead Tim Phillips owns shares of Mapletree Industrial Trust.