Last week’s news of a restructuring of Singapore Press Holdings Limited (SGX: T39), also known as SPH, was the big headline making the rounds in the local stock market.

Trading at close to S$4 five years ago, SPH shares are now 60% lower at around S$1.56. For SPH shareholders, it’s clear that the restructuring will not be beneficial to them given the media assets of the group are being given away for free.

Beyond those doubts, SPH CEO Ng Yat Chung also started trending after he – in his own words – “took umbrage” with an inconspicuous question from a journalist.

As we approach the one-year anniversary of SPH’s removal from the Straits Times Index, I thought it would be appropriate to scout Singapore’s stock market for some companies that are being disrupted.

That way, we could see which stocks long-term investors should take umbrage with and, therefore, avoid at all costs.

1. Singtel

The flagship telecommunications provider here, Singapore Telecommunications Limited (SGX: Z74) – also known as Singtel – has been one of the worst large Straits Times Index stocks over the past five years or so.

Singtel has seen its business disrupted by increased competition in the mobile space as the pricing power of data providers plunged with new entrants into the market.

What’s more, its Pay-TV business had its lunch eaten by the likes of streaming services such as Netflix Inc (NASDAQ: NLFX).

As a result, its share price has been nearly cut in half since 2015. Then there’s its dividend, which in 2020 was down by 30% from its level in 2017. All this is evidence of the struggle that this once-reliable blue chip company is now facing.

2. Hongkong Land

For any long-time investor, Hongkong Land Holdings Limited (SGX: H78) seems like a reliable property company.

However, its fortunes have suffered in recent years. Although the property group owns a suite of grade-A commercial properties in Hong Kong’s Central district, demand for these offices have been falling.

Hongkong Land’s office portfolio in Hong Kong had a vacancy rate of 6.3% at the end of 2020 but was already climbing before the pandemic hit (it was up to 2.9% in 2019 from the 1.4% in 2018).

That’s because corporations realise they don’t need to pay top dollar in Central for office space, given the amount of available office space in other parts of Hong Kong, such as Kowloon East and Quarry Bay.

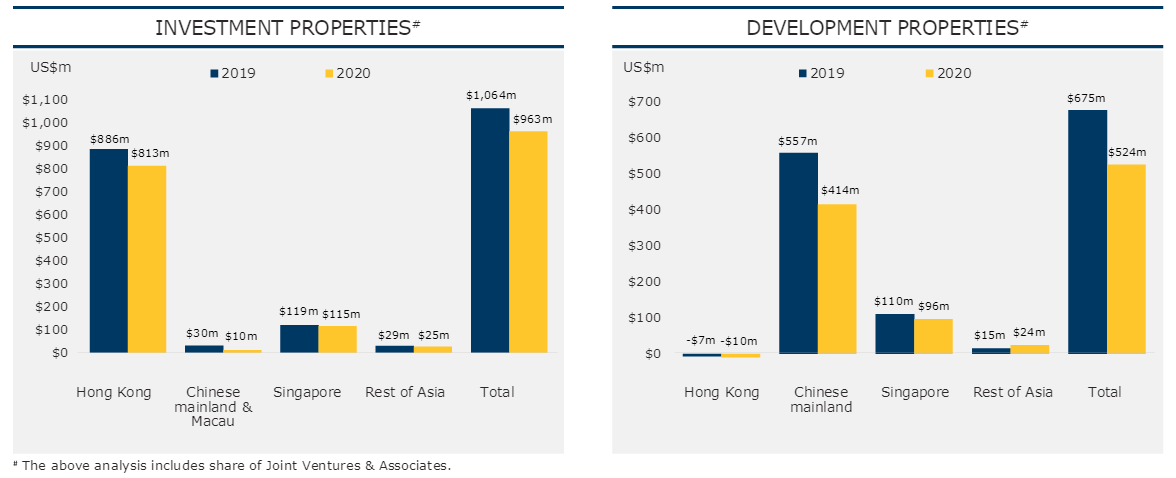

Evidently, that’s a problem for Hongkong Land given the amount of money its investment properties portfolio generates from Hong Kong (see below).

Source: Hongkong Land full-year 2020 investor presentation

Although the company has residential development projects in the pipeline in China, Hong Kong still remains the key profit generator.

3. CapitaLand Integrated Commercial Trust

Formerly known as “CapitaLand Mall Trust”, or CMT, CapitaLand Integrated Commercial Trust (SGX: C38U) is the creation of the Singapore mall operator combined with CapitaLand Commercial Trust.

Now owning both retail and commercial properties, it is the largest listed REIT in Singapore. However, that doesn’t mean it’s well-positioned to deliver superior returns to shareholders.

A case in point has been its sluggish distribution per unit (DPU) growth. In 2009, CMT paid out a DPU of 8.85 Singapore cents.

A decade later, in 2019 (before the pandemic hit), CMT paid out a DPU of 11.97 Singapore cents – meaning the dividend grew at a compound annual growth rate (CAGR) of a meagre 3.1%.

Although it’s a popular name, with many recognisable malls, question marks remain over whether the addition of a few Singapore office properties (along with one in Germany) will really improve its distribution growth for investors.

4. CDL

Property developer City Developments Limited (SGX: C09) is a great example of what can go wrong for listed real estate stocks in Asia.

Relying on developing properties to generate significant profits, any hit to sentiment in the property market means that these stocks are hammered. CDL is no exception.

Similar to some of the worst Hang Seng Index stocks, CDL shares trade at a discount to their net asset value (NAV).

A while ago many analysts would claim this was a reason to buy their shares. Now, however, as this discount has become a permanent fixture, those calls aren’t so frequent.

Over the past 10 years, CDL’s share price is down 30%. In 2020, the company was hit hard as it recorded an EBITDA of negative S$1.4 billion for the year, down from an EBITDA of positive S$1.1 billion in 2019.

Meanwhile, its dividend per share (DPS) in 2020 was slashed by 40% year-on-year to 12 Singapore cents.

5. Singapore Airlines

Singapore Airlines Ltd (SGX: C6L) has probably come to embody the havoc wreaked by Covid-19 more than any other company.

Yet even before the pandemic hit the airline industry, Singapore Airlines was suffering. At the end of 2019, shares were languishing at around S$3.40 – down by 35% over the previous decade.

In its latest quarter, cargo revenue made up about 70% of overall revenue, up from the 12% cargo generated in the previous year.

Beyond all the issues with passenger numbers and when global travel will become “normal” again, investors also have to ask whether business travel will resume.

This is the key question because business class seats make up the bulk of revenue for airlines. With the onset of Zoom video and the “work from anywhere” economy, perhaps business travel will never return to its previous heights.

Avoiding risky companies

Many of us may think that the above are “safe” companies yet they’re anything but. In danger of being disrupted, or operating in sectors that are unfavourable, means that shareholder returns can suffer going forward.

Instead, it’s important that long-term investors look for companies that are the disruptors or who can defend their competitive advantage while also innovating. I don’t think anyone could take umbrage with that.

Disclaimer: ProsperUs Head of Content Tim Phillips doesn’t own shares of any companies mentioned.