When you think of insurance, you generally think of it as a boring, mature industry waiting to get disrupted.

Yet in Asia, the growth runway for insurance, especially life and health, is still huge. That’s because the lack of social security safety nets in the region mean many people buy insurance privately.

One big winner from that trend is AIA Group Ltd (SEHK: 1299), a Hong Kong-listed insurance giant that has a presence in 18 Asia-Pacific markets.

The company recently released its full-year 2020 earnings and although its value of new business (VONB) was down 33% year-on-year to US$2.76 billion, it still posted an operating profit of US$5.94 billion – which was up 5% year-on-year.

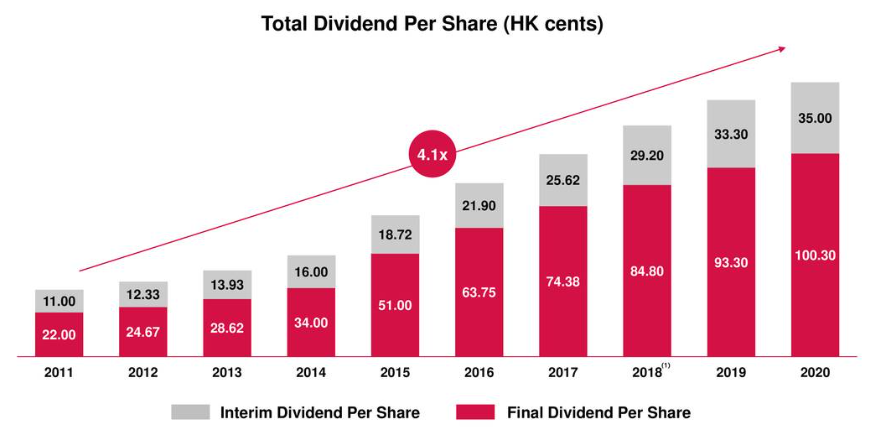

In a year when shutdowns were common across Asia, AIA’s business did suffer. Remarkably, though, the company still managed to raise its full-year dividend per share by 7.5% to 100.30 HK cents.

Track record to match

AIA has managed to keep growing its business by expanding further into China, region by region. This trend is likely to play out over the next decade as China’s insurance gap is still sizable.

For long-term investors, even though shares are up nearly 400% since listing a decade ago, the dividend tends to go unnoticed. That’s because its shares, which yield “only” 1.4%, mask a strong dividend grower.

If we zoom out over the longer term, the company’s dividend growth track record is enviable. Since listing in 2010, it has grown its full-year dividend over four-fold in less than a decade (see below).

What’s more, its business – which was battered last year – will be a key beneficiary of the “reopening” trend as headwinds last year turn into tailwinds in 2021.

For investors who want a combination of both structural growth and a consistently rising dividend, AIA looks likely to be continue being one of the top choices in the Asian region.

Source: AIA Group full-year 2020 earnings presentation

Disclaimer: ProsperUs Head of Content Tim Phillips owns shares of AIA Group.