Ping An Insurance Group Co of China Ltd (SEHK: 2318) is a well-known Chinese financial conglomerate with interests in insurance, banking, fintech and health tech, among others.

The insurance giant is also well-positioned for long-term growth given the low life insurance penetration rate in China.

What’s more, Ping An Insurance has effectively leveraged technology and has constantly innovated to disrupt an infamously staid industry.

On the income side, it is also a stock that has consistently grown its dividends – a crucial feature for any investor interested in long-term passive income.

Besides that, though, there is a lot more to like about the company. Here, I’ll share three charts that illustrate why Ping An Insurance is such a great long-term investment.

1. Massive online opportunity set

Ping An is a financial powerhouse that is utilising technology to continue growing its business and in order to take market share.

Positioning itself as an “online-first” business has only highlighted the importance of its strategy amid Covid-19.

As you can see below, in the first half of 2020, Ping An had 214 million retail financial customers while the group’s overall number of internet users on its platforms numbers 579 million.

For long-term investors, the exciting untapped opportunity for Ping An Insurance lies in converting those 365 million users of the group’s various platforms in China who are not yet retail customers.

Source: Ping An Insurance Q3 2020 results presentation

2. Cross-sell capabilities

One of the main appeals of Ping An is that it has a huge presence in a number of financial services markets – from life and health insurance to banking and asset management.

Using technology, it can then easily cross-sell products across its various businesses. What this enables are more “sticky” customers that are locked into the Ping An ecosystem at one point or another.

Furthermore, it also provides the group with more data on what customers want or need. This allows it to better target products for consumers.

As readers can see below, the increasing cross-penetration ratio (alongside the rising number of customers with multiple contracts) shows how good of a job Ping An is doing in executing this strategy.

Source: Ping An Insurance Q3 2020 results presentation

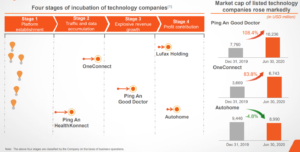

3. Range of businesses in different stages

Perhaps one of the less-appreciated aspects of Ping An Insurance is its exposure to its technology subsidiaries in various spaces.

As you can in the company’s growth chart, its businesses are in different stages of development. However, with the support of Ping An Insurance’s massive customer base, these have been able to grow rapidly.

Even better, Ping An continues to experiment with technology in its own business to make things more efficient.

OneConnect Financial Tech Co Ltd (NYSE: OCFT) listed in the US at the end of 2019 while Ping An Healthcare and Technology Co Ltd (SEHK: 1833), also known as Ping An Good Doctor, has been listed in Hong Kong since 2018.

The fact the company can realise value in its investments by listing them is good news for shareholders, who can get exposure to these fast-growing businesses via Ping An Insurance shares.

Source: Ping An Insurance 2020 Interim Results presentation

Betting on the benefits of technology

For Ping An Insurance, the technology backdrop has been a strong driver of its investment thesis. As investors can see, the company has done an admirable job of carrying out this broader strategy of tech-powered business growth.

If you believe in the long-term value of technology, like I do, then Ping An Insurance is definitely a stock to hold for the next 10-20 years.

Disclaimer: ProsperUs Head of Content Tim Phillips owns shares of Ping An Insurance Group Co of China Ltd and Ping An Healthcare and Technology Co Ltd.