- Earnings Growth Potential: MR D.I.Y. is poised to benefit from catalysts like private consumption growth and ongoing store expansions.

- Expansion Focus: The company is targeting untapped regions, particularly East Malaysia and the East Coast of Peninsular Malaysia.

- Buying Opportunity: As of Feb 19, 2025, MR D.I.Y.’s share price has dropped 25% this year, likely due to excessive market pessimism.

MR D.I.Y. Group (KLSE:5296), a home improvement retailer in Malaysia, is known for its impressive store network and affordable product range. However, with its share price dipping 25% in 2025 so far, some investors might be wondering if this is a sign of trouble or simply an opportunity for a savvy buy.

The company, which operates over 1,300 stores in Malaysia and Brunei under brands like MR.D.I.Y., MR.DOLLAR, and MR.TOY, is on a path to long-term growth, supported by multiple catalysts, including store rollouts, improved consumer sentiment, and increasing contributions from its associate, KKV.

At present, the retailer has 11 ‘buy’ calls and four ‘hold’ calls from analysts. Bee Family Ltd., with a 50.9% stake, and Employee Provident Fund (EPF), holding a 7.53% stake, are the company’s major shareholders.

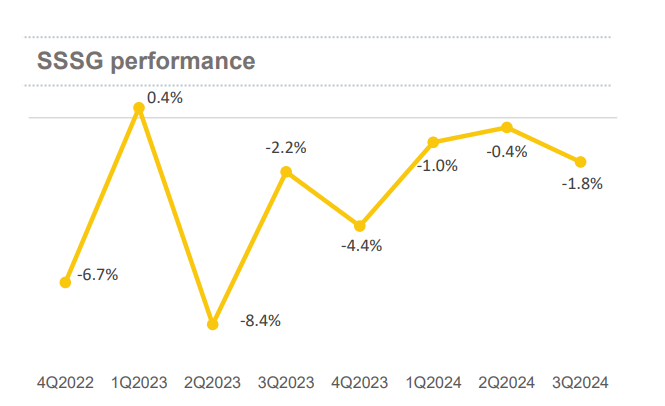

As of February 19, 2025, market concerns about its upcoming 4Q 2024 results (scheduled for release on February 27) are weighing on the stock. Investors are concerned that MR D.I.Y.’s earnings might be affected by ongoing challenges with its automated warehouse and declining same-store sales growth (SSSG).

Source: MR D.I.Y

Outlook for 2025

Looking ahead, MR D.I.Y. remains on a growth trajectory:

1. New Stores: During its 3Q 2024 results briefing, MR D.I.Y. highlighted plans for 190 new stores for 2025 (up from the usual target of 175-180), focusing on untapped regions like East Malaysia and the East Coast of Peninsular Malaysia. In addition to expanding the traditional store format, MR D.I.Y. is looking to open over 20 new KKV stores, which cater to a younger audience with trendy lifestyle products.

2. Private Consumption Growth: Our economics team forecasts 4.6% GDP growth and 5.7% private consumption growth in 2025. Positive government policies, including higher civil servant salaries, minimum wage increases, and cash handouts for lower-income households, are expected to boost demand in the consumer discretionary sector, benefiting MR D.I.Y.’s SSSG in 2025.

3. Stable Gross Profit Margins: On the operational side, MR D.I.Y. has recovered from the supply chain issues that were prevalent during the Covid-19 pandemic. We expect the company to maintain a stable gross profit margin of around 45.5%. With its growing associate KKV contributing more to MR D.I.Y.’s overall performance, margins should remain resilient.

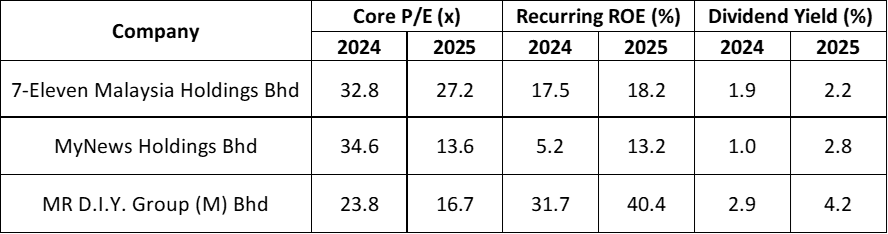

How MR D.I.Y. Measures Up to Its Peers

To better understand MR D.I.Y.’s position in the market, let’s see how it compares with other consumer stocks in Malaysia.

Source: CGSI Research

1. Growth Prospects: MR D.I.Y. boasts a high return on equity (ROE) of 31.7%, which means the company is efficient at turning its investments into profits. This makes MR D.I.Y. an attractive pick for investors seeking strong growth potential.

2. Affordable Valuation: With a price-earnings (P/E) ratio of 23.8x for 2024, MR D.I.Y. is priced more affordably than competitors like MyNews (34.6x) and 7-Eleven (32.8x). This suggests MR D.I.Y. offers good value for investors looking for growth opportunities at a reasonable price.

3. Solid Dividends: MR D.I.Y. provides a competitive dividend yield of 2.9% in 2024, with potential to increase to 4.2% in 2025. This makes the company appealing to income-focused investors.

Risks to Consider

However, it’s not all smooth sailing. There are risks investors should be mindful of:

- Slower Store Openings: If MR D.I.Y. faces challenges in its aggressive expansion plans, the company’s growth could stall.

- Margin Pressures: Any strain on operational efficiency, such as higher costs or weaker sales, could affect the company’s margins.

Conclusion

MR D.I.Y.’s share price drop of 25% in 2025 may feel like a red flag, but it could also present an opportunity for investors who believe in the company’s long-term growth story. MR D.I.Y. could be a compelling addition to a diversified portfolio, but investors should be comfortable with the potential volatility that comes with it.

Disclaimer: Hailey Chung, Manager of Content at ProsperUs, does not own shares in the company mentioned.

Reference

CGSI | Mr D.I.Y. Group | Feb 18, 2025