When long-term investors look at their total returns, it’s important to remember that avoiding losing stocks is as crucial as being invested in the winning stocks.

More often than not, these losing stocks tend to destroy your wealth over multiple years. One defining feature of them is that they operate in industries where they’re either being disrupted or revenue growth just simply doesn’t exist.

In some cases it can be both. Unfortunately in Singapore, like everywhere else, these types of stocks are plentiful – that’s particularly true of the Straits Times Index.

It’s imperative that investors avoid them so that their wealth has a fighting chance.

Otherwise, it kind of defeats the purpose of investing, right? You should just keep your hard-earned money in cash if what you put into the market is constantly declining, year after year.

With that in mind, here are two Straits Times Index constituent stocks that have destroyed value for shareholders and I think should be avoided at all costs.

1. Singtel

The largest local telecommunications firm Singapore Telecommunications Limited (SGX: Z74), better known as Singtel, is one of the best-known Singaporean companies.

A lot of us deal with the company regularly as mobile plan subscribers or perhaps pay-TV subscribers. However, just because it’s a big, and visible, company doesn’t make it a great investment.

The numbers speak for themselves. When purchasing property the saying “Location. Location. Location” rings true. When investing in stocks, though, my mantra is “Cash flow. Cash flow. Cash flow”.

That’s because, as long-term investors, we should be buying into the future cash flows of great companies.

And one of the best metrics is free cash flow. On that metric, Singtel has been poor. Back in the first half of fiscal year 2018, the company’s free cash flow stood at just over S$2 billion.

Weakening fundamentals

For the first six months of fiscal year 2021? That free cash flow number for Singtel had dropped to S$1.7 billion. That also happened to be sequential drop from the first-half fiscal year 2020 when it was S$1.99 billion.

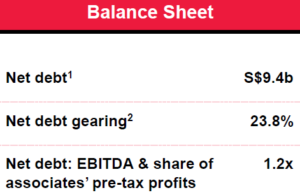

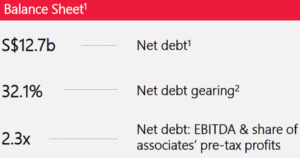

Add to that a deterioration in Singtel’s balance sheet over the period (see tables below). Net debt, gearing and net debt-to-EBITDA are all significantly higher today than they were three years ago.

Figure 1: Singtel balance sheet H1 FY2018

Figure 2: Singtel balance sheet H1 FY2021

Sources: Singtel H1 FY2018 and H1 FY2021 presentation slides

In January 2011, Singtel shares traded at around $3.10 apiece. Right now they sit at S$2.47 so on a price return basis, they’re down by nearly 20% over a decade.

The Singtel dividend might be the saving grace for some investors – it yields over 4% – but with a balance sheet that weak, I wouldn’t have any confidence that the company wouldn’t cut it further (it was cut twice in the past 12 months).

Furthermore, “5G” has been a buzzword for a lot of telcos but right now it’s still unclear how they’ll exactly monetise this mega trend so that it starts showing up materially on the top and bottom lines.

2. Dairy Farm

Second on the list to avoid is retail specialist Dairy Farm International Holdings Ltd (SGX: D01). The company operates a host of grocery stores, convenience stores and health and beauty outlets in Hong Kong, China and Southeast Asia.

Investors could be forgiven for thinking Dairy Farm is a regional retailing powerhouse. It used to be. Now, however, its star is waning and poor results bear this out.

In Hong Kong, it’s widely-known that Dairy Farm’s Wellcome supermarket operates in a duopoly with ParknShop.

In Singapore, its offerings have tended to underwhelm, with its Cold Storage and Giant brands either too pricey or not ubiquitous enough throughout the city state.

Competition in Singapore’s retail sector is also red-hot with the likes of RedMart, Amazon Fresh, NTUC FairPrice, and Sheng Siong Group Ltd (SGX: OV8) all possessing compelling offerings.

Zero digital innovation

That’s also highlighted another issue; Dairy Farm’s digital strategy has been severely lacking. The “comfort” and “safety” of the Hong Kong businesses, which have reliably thrown off profits, has been bad news for shareholders.

This has resulted in underinvestment across the group in terms of upping its appeal and offerings to consumers. In fact, Dairy Farm CEO Ian McLeod admitted as much in the company’s 2018 annual report when he stated that:

“We have historically been slow in responding to changing consumer dynamics and underinvesting in business infrastructure; something we are urgently addressing”.

Although Dairy Farm is currently undergoing a multi-year “transformation” plan, it’s unclear whether it will be successful. Given the competitive landscape the group operates in, and how far it has fallen behind in the region, the odds (at least to me) do not look good.

Take a look at long-term business performance to see what I mean. Back in the first six months of 2010, the company notched up underlying profit attributable to shareholders of US$182 million.

In the first six months of 2020, the company’s underlying profit attributable to shareholders was down at US$105 million.

Trading at over US$9 a share in January 2011, Dairy Farm shares now go for around US$4.50 – basically its share price has been cut in half over the past 10 years.

Although Dairy Farm does have a 20% stake in China’s Yonghui Superstores, shareholders shouldn’t rely on this alone to generate a return to profitable growth.

Avoiding laggards for long-term gains

For long-term investors, avoiding the laggards in any given sector is important to ensuring you don’t lose money.

Given the poor track records of both Singtel and Dairy Farm, and the dim outlooks for both, I would steer clear of these two Straits Times Index stocks.

Disclaimer: ProsperUs Head of Content Tim Phillips doesn’t own shares in any companies mentioned.