In the Singapore REIT space, earnings have been coming thick and fast for dividend investors.

They’ve been keen to see how REITs have been doing in this higher interest rate environment.

Last Friday (27 January), after the market closed, healthcare-focused Parkway Life REIT (SGX: C2PU) released its latest H2 FY2022 results.

Traditionally, the REIT has been seen as defensive given the nature of its properties and the visibility of revenues it generates.

It’s also a firm favourite among Singapore REIT investors given its track record of stellar total returns over the long term.

So, here are three big numbers that Singapore dividend investors should know about from Parkway Life REIT’s latest earnings.

1. DPU increases 2.7%

As with all REITS, investors are generally focused on the distribution per unit (DPU) that the REIT can pay out.

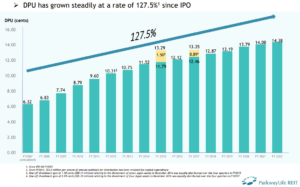

Thankfully, in Parkway Life REIT’s case, it’s latest H2 FY2022 (for the six months ending 31 December 2022), saw it announce a DPU of 7.32 Singapore cents.

This was up by 2.7% year-on-year versus the same period in 2021 and its full-year 2022 DPU of 14.38 Singapore cents was up 2.1% year-on-year versus FY2021.

That has allowed the REIT to maintain its impressive streak of consistent growth of its regular DPU since listing in 2007 (see below).

Source: Parkway Life REIT’s H2 FY2022 earnings presentation

Mainly attributable to higher rents from the Japan properties it acquired in 2021 and 2022, as well as higher rent from its Singapore hospitals, Parkway Life REIT managed to see revenue growth of 7.7% for FY2022 to S$130 million.

2. All-in debt cost of just 1.04%

What makes Parkway Life REIT stand out from the rest of the S-REIT universe is its unvelievably low cost of funding.

As of 31 December 2022, the REIT’s all-in debt cost was just 1.04%, perhaps reflecting how low interest rates have gone in Japan – a place where it takes out a of its loans.

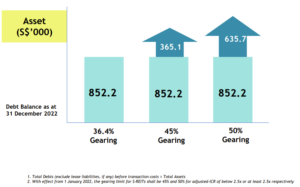

Meanwhile, the low cost of debt is also indicative of the broader strength of Parkway Life REIT’s balance sheet, which remains robust.

Its gearing ratio is at a very reasonable 36.4% while its interest coverage ratio (ICR) of 18.3 times is a multiple bigger than most of its S-REIT peers.

A gearing ratio in this range gives Parkway Life REIT significant debt headroom to acquire if it wants to (see below).

Source: Parkway Life REIT’s H2 FY2022 earnings presentation

3. Around 80% of interest rate exposure hedged

As for its debt profile, Parkway Life REIT announced that it has about 80% of its interest rate exposure hedged.

Its distributable income to unitholders has also been protected with FX hedges in place until Q1 2027, giving investors comfortable visibility over its Singapore dollar DPU.

The REIT also said that it attained attractive pricing of 0.85% and 0.97% on a 6-year JPY 5.0 billion and 7-year JPY 6.04 billion, respectively, on senior unsecured Fixed Rate Notes (FRN) issuance.

Having said that, there is no long-term debt refinancing needs for the REIT until February 2024.

Giving what REIT investors expect

It wasn’t an eventful H2 FY2022 for Parkway Life REIT. In fact, in many ways, it was what investors expected.

In this environment, that’s a positive. The REIT remains very disciplined and management says it will look to a multi-pronged growth platform for its next phase of growth.

This will focus on strengthening its presence in existing markets, building a third key market for mid- to long-term growth, and finally fostering multiple strategic partnerships that can help it grow and expand.

Disclaimer: ProsperUs Head of Content & Investment Lead Tim Phillips owns shares of Parkway Life REIT.