It’s that time of year again for Singapore REIT lovers; earnings season.

While Christmas only comes round once a year, for Singapore investors buying into S-REITs, earnings season is much more frequent – with REITs listed here normally updating unitholders four times a year.

One of the first REITs to report its earnings this season was data centre-focused Keppel DC REIT (SGX: AJBU). It released its H1 2023 (for the six months ending 30 June 2023) results on Monday.

The REIT last gave investors an update in April, when it revealed its Q1 2023 operational metrics.

So, for Singapore REIT and dividend lovers, here are three key takeaways from Keppel DC REIT’s latest H1 2023 results.

1. Dividend flat for the year

As REIT investors, we’re all focused (understandably) on the distribution per unit (DPU) that they pay out.

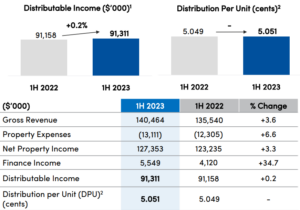

Linked to that is the actual growth of the DPU. For Keppel DC REIT, in H1 2023, it announced a DPU of 5.051 Singapore cents (see below).

That was effectively flat year-on-year from the DPU of 5.049 Singapore cents for H1 2022. Meanwhile, its Q2 2023 DPU of 2.51 Singapore cents was actually down 2.8% year-on-year.

Source: Keppel DC REIT H1 2023 earnings presentation

While it does announce quarterly DPUs, Keppel DC REIT actually only pays out the DPU to unitholders twice a year (for H1 and the full year).

Distributable income was up slightly by 0.2% year-on-year to S$91.31 million. This was mainly due to an increase in gross revenue from the acquisitions of Guangdong DC 2 and the building shell of Guangdong DC 3.

Some renewals and income escalations also contributed to stable distributable income. The higher top line growth was partially offset by lower contributions from some Singapore colocation assets, given higher costs (like electricity).

2. Gearing down to 36.3%

In this interest rate environment, many investors are watching the gearing (or leverage) ratios of REITs.

For Keppel DC REIT, its gearing ratio of 36.3% (as of 30 June 2023) was an improvement of 50 basis points (bps) from the prior quarter.

That debt headroom provides the REIT with plenty of growth opportunities should they arise.

Meanwhile, Keppel DC REIT’s average cost of debt was 3.3% in Q2 2023, up 50 bps from the prior quarter.

Its interest coverage ratio (ICR), for the trailing 12 months, remained strong at 6.0 times while it has no debt maturing this year and only around 11% of its total debt maturing in 2024 and 2025.

Source: Keppel DC REIT H1 2023 earnings presentation

3. Trading at big premium to NAV

Keppel DC REIT has always seemed to be an expensive Singapore REIT, from a valuation perspective. Indeed, the share price’s strong rally so far in 2023 has made that price-to-book (PB) ratio even higher.

As of 30 June 2023, Keppel DC REIT’s net asset value (NAV) per unit was S$1.39. Keppel DC REIT units closed at S$2.16 on the last day of June, meaning the shares’ premium to NAV was 55.4%.

Keppel DC REIT shares today are trading even higher, close to S$2.30, meaning that its PB ratio has stretched even further – to 1.64 times.

Paying up for quality

Overall, it was a solid quarter for Keppel DC REIT with no surprises on the revenue or distribution fronts.

US data centre firm Cyxtera (one of the REIT’s tenants) filed for Chapter 11 bankruptcy in early June.

However, management did say that its UK-based GV7 data centre is fully master leased to Cyxtera’s UK entity and that the tenant remains current with its rent obligations.

With Keppel DC REIT one of the few REITs in Singapore that isn’t cutting its DPU in this environment, while also providing opportunities for growth, investors appear willing to pay a premium to hold it.

Its share price has rallied nearly 27% so far this year and at its current price, Keppel DC REIT shares are giving dividend investors a 12-month forward yield of 4.4%.

Disclaimer: ProsperUs Head of Content & Investment Lead Tim Phillips doesn’t own shares of any companies mentioned.