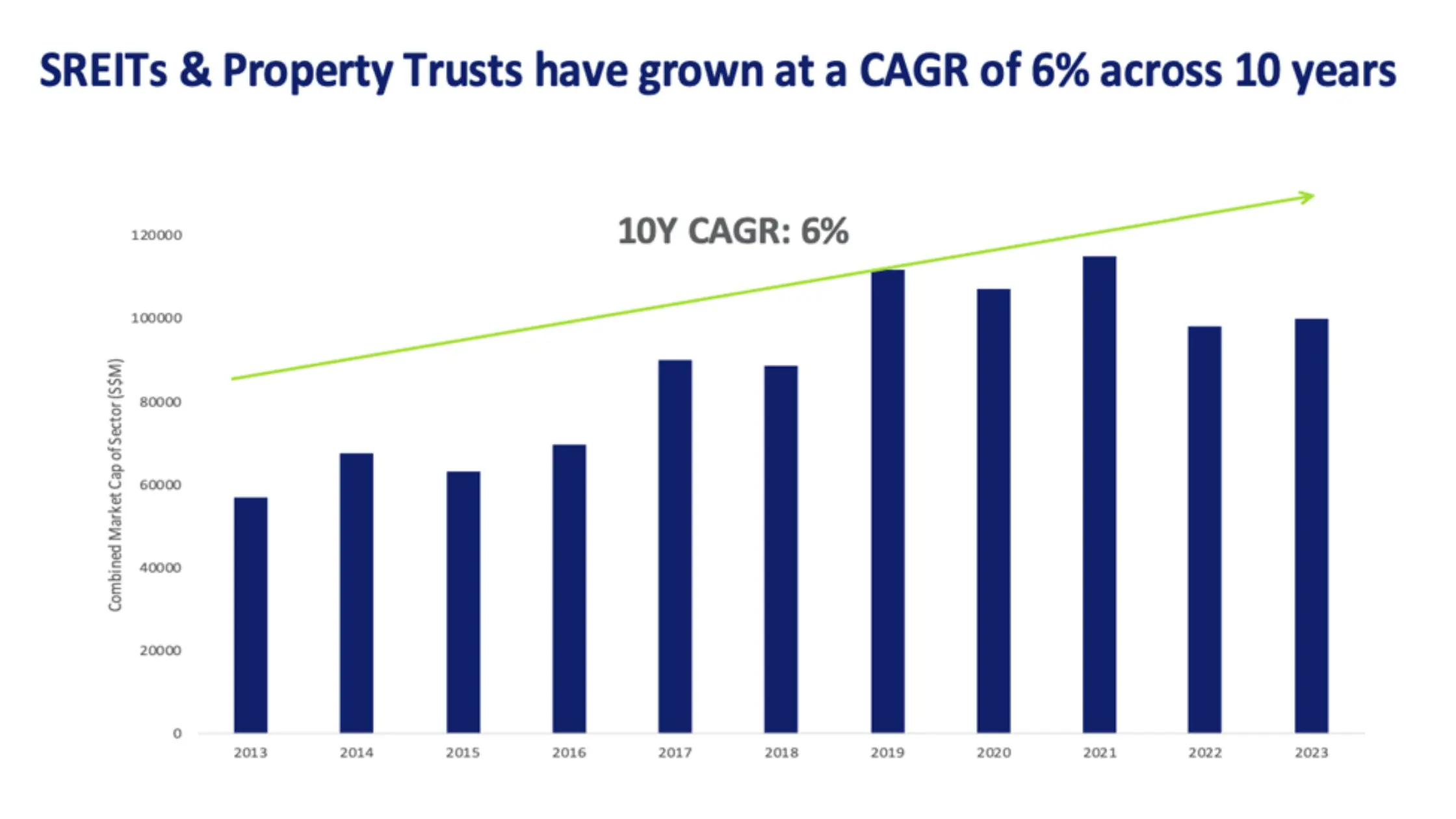

As we look towards 2024, the question on many investors’ minds is whether Singapore REITs (S-REITs) can weather the storm of less aggressive Federal Reserve rate cuts. Over the past two years, S-REITs have struggled to gain momentum amidst the rising global interest rates. This trend, influenced mainly by monetary policies aimed at curbing inflation, has led to higher borrowing costs for REITs, pressuring their operational margins and distribution yields. Higher interest rates generally result in higher capital costs for REITs, making it more expensive to finance acquisitions and developments. Despite these challenges, S-REITs have grown at a compounded annual growth rate (CAGR) of 6% over the last ten years, a reflection of its resilience.

Source: SGX

Going forward, I believe there is a potential pathway for recovery for S-REITs in 2024, even if the interest rate cuts by the US Federal Reserve are not as aggressive as previously hoped. This resilience and recovery is underpinned by several factors:

Strong balance sheet to withstand the current interest rate level

Most of the S-REITs’ balance sheets reflect robust health, underscored by judicious leverage and a strategic approach to capital management. Based on the latest quarterly filing as of the end of February 2024, the average gearing ratio among S-REITs stood at a comfortable 38%, reflecting a healthy buffer below the regulatory ceiling of 50%. This prudent financial positioning affords them ample room to manoeuvre for future growth opportunities and debt servicing capabilities.

Selected sectors within S-REITs will benefit from structural growth

The sectoral dynamics will also play a role. Industrial and logistics REITs have enjoyed robust demand, buoyed by the e-commerce surge, while data centres have capitalised on digital transformation trends. Hospitality REITs, too, are recovering with the rebound in tourism.

Improve efficiency to mitigate higher borrowing costs

Operational efficiencies and cost management have been key for S-REITs in maintaining their margins. Strategic use of technology and a focus on tenant retention have helped mitigate the impact of higher borrowing costs.

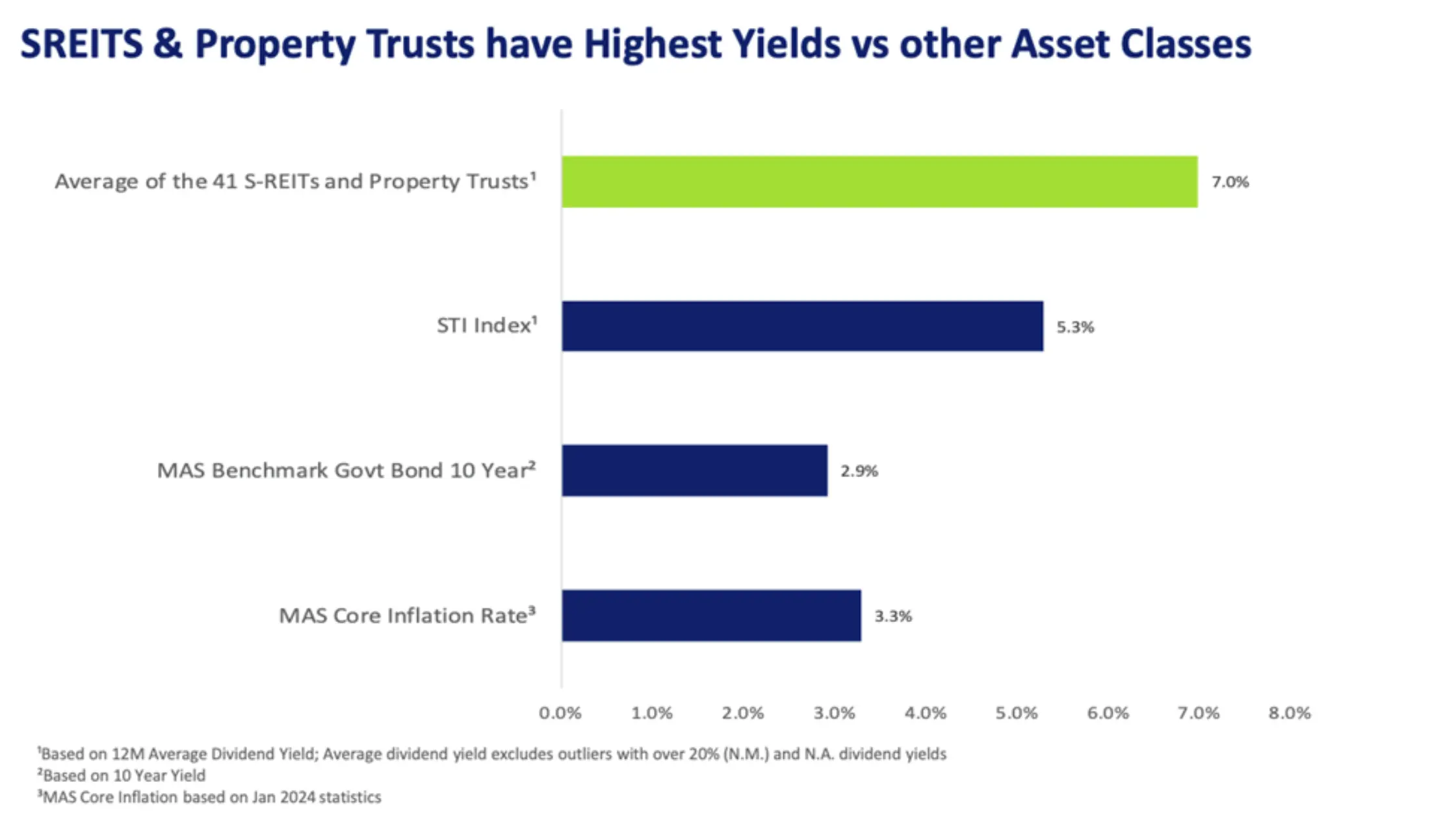

Attractive yield despite rising interest rate

Source: SGX

S-REITs have solidified their reputation as a high-yield asset class. Recent data from February 2024 highlights that S-REITs boast an average dividend yield of 7.0%, surpassing the 5.3% yield from the Straits Times Index (STI) and outperforming the yields of long-term government bonds and the core inflation rate, which stand at 2.9% and 3.3% respectively. This differential underscores S-REITs’ appeal to investors seeking robust income-generating investments.

S-REITs continue to expand with targeted acquisitions and developments

Furthermore, S-REITs have continued to expand through targeted acquisitions and developments. These moves are not merely growth signals but also strategic efforts to strengthen portfolios and tap into markets with solid demand drivers. This proactive stance has been evident in recent activities, including the recent acquisition of German’s logistics and industrial portfolio by Frasers Logistics & Commercial Trust (SGX: BUOU).

Focus on the long-term investment potential of S-REITs

With a perspective geared towards long-term investment, the current valuation of S-REITs presents a compelling entry point for investors aiming to leverage the sector’s robustness and anticipated rebound. Highlighted below are five S-REITs that are particularly well-placed for strategic growth and potential revitalization in the year 2024.

- CapitaLand Integrated Commercial Trust (CICT): As Singapore’s largest REIT by market capitalisation, CICT has a prime portfolio of retail and office assets that are well-positioned to benefit from economic recovery.

- Mapletree Industrial Trust (MIT): With a significant presence in the data centre space and a diverse asset portfolio, MIT is poised for growth amid the digital economy’s expansion.

- Frasers Logistics & Commercial Trust (FLCT): FLCT’s recent expansion in the robust German market indicates its strategic moves to strengthen its position in logistics and industrial sectors.

- CapitaLand Ascott Trust: A leading hospitality trust, it is well-suited to capitalise on the global travel rebound and offers a diversified portfolio of serviced residences and rental housing properties.

- ParkwayLife REIT: Specializing in healthcare real estate, it is considered defensive due to the essential nature of its assets, and it’s set to continue benefitting from the sector’s long-term growth.

These REITs represent a cross-section of the S-REIT market that has demonstrated the ability to thrive in challenging conditions. With their solid fundamentals, proactive management, and strategic acquisitions, they offer investors the potential for robust returns as the sector navigates the fluctuating interest rate environment and the broader economic recovery.

Disclaimer: ProsperUs Head of Content & Investment Lead Billy Toh doesn’t own shares of the company mentioned.