The world has been rocked by news of the failure of both Silicon Valley Bank (SVB) and Signature Bank in the US.

Following close on the heels of this was the rapid, and rather spectacular, collapse of Credit Suisse in Europe.

So, understandably, many investors in Singapore are concerned. That’s because a lot of us here have exposure to bank stocks.

The reason? The Straits Times Index (STI) itself has a 47% weighting in the three local big bank stocks.

They’ve all fallen in the past few weeks on worries of contagion. However, they’ve held up a lot better than their US and European counterparts.

So, for investors looking at bank stocks, and who want quality dividend growth, here’s why you should buy shares of the leading Singapore bank – DBS Group Holdings Ltd (SGX: D05).

Poor returns for US banks

Let’s face it. Bank returns in the US have been poor, even before the recent collapse in share prices.

If investors take a look at the S&P Banks Select Industry Index, its annualised price return over the past five years has been -0.32%.

That was data from the end of February 2023. No doubt those numbers look even worse now following the SVB and Signature Bank debacles.

Meanwhile, for DBS shares, the bank’s price return has been positive over the past five years – delivering annualised positive returns of 3.9%.

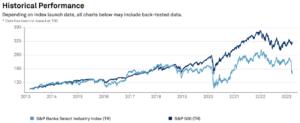

Looking at it from a total return basis is even more painful for US bank stock investors. As readers can see below, the banks sector has badly lagged the S&P 500 Index – on a total return basis – over the past decade.

Source: S&P Dow Jones Indices, as of 28 February 2023

Singapore’s bank leader

Meanwhile, DBS has a solid balance of both price appreciation and dividend growth. The key for investors is to get a positive total return from bank stocks.

That’s what DBS has given investors. Its average annualised dividend growth of 10.4% over the past decade is testament to its consistency on delivering a reliable dividend.

That compares to 8.5% annualised growth for UOB’s dividend and 7.5% for OCBC over the same period.

Additionally, a higher-than-average return on equity (ROE) versus its other Singapore-based bank peers also means DBS is more efficient at generating returns on its capital.

At its current share price, DBS shares are giving investors a 12-month forward dividend yield of around 5%.

Given its dividend growth, that’s an appealing yield in today’s environment.

What about exposure to US and European banks and non-financial corporates for DBS?

While DBS is estimated to have the highest exposure among its peers (around 3-4% of its FY2023 book value), it’s still a negligible amount and is also mostly in investment-grade debt.

Thinking long term

One of most appealing factors about Singapore’s banks – stability – has been highlighted during the recent crises in the US and Europe.

For investors who believe in Singapore’s banks as generators of superior shareholder returns, the current situation could present an ideal opportunity to add DBS shares to your portfolio.

As the leader in Singapore’s banking sector, the company has delivered both positive price returns and dividend growth over the long term.

For long-term dividend investors, that’s something worth banking on.

Disclaimer: ProsperUs Head of Content & Investment Lead Tim Phillips owns shares of DBS Group Holdings Ltd.