In Singapore, the local economy seems to be booming as shoppers flock back to shops and people head back to the office.

This has created dilemma for Singapore dividend investors because retail REITs are benefitting from the reopening trend yet their share prices are pressured by rising interest rates.

On the whole, though, the trend of retail and commercial REITs in Singapore seeing their property assets perform well has held up.

A perfect example of this is heartlands-focused shopping mall operator Frasers Centrepoint Trust (SGX: J69U).

The REIT has always been a popular retail play on Singapore’s consumer economy. In late October, Frasers Centrepoint Trust reported its H2 FY2022 earnings (for the six months ending 30 September 2022).

So, for investors, did the REIT’s earnings improve over the period and are its shares worth buying now?

Frasers Centrepoint Trust’s revenue and NPI up, DPU flat

For investors, Frasers Centrepoint Trust saw gross revenue of S$180.7 million in H2 FY2022, up 7.9% year-on-year.

Meanwhile, net property income (NPI) was S$128.1 million and up 6% year-on-year for the period.

While the REIT’s distribution per unit (DPU) was flat for H2 FY2022 – at 6.091 Singapore cents – for the whole of FY2022 it did manage to see its DPU rise 1.2% to 12.227 Singapore cents.

At the portfolio level, the REIT saw its committed occupancy rate at its retail malls rise to 97.5% as of 30 September 2022, from 97.1% as of 30 June 2022.

Rental reversions positive and shoppers return

Frasers Centrepoint Trust saw solid occupancy amid the return of shoppers to its malls. In fact, five out of its nine malls had an occupancy rate of above 99% as of 30 September 2022.

Rental reversions were also positive in H2 FY2022, coming in at +1.5% while tenant sales were up 11.3% year-on-year in FY2022 and averaged 10% above pre-COVID levels.

Portfolio shopper traffic at its malls was up 12.4% year-on-year during FY2022, signalling that Singapore consumers are back to shopping outside again.

The REIT’s malls are also attractive to tenants, as measured by a lower portfolio occupancy cost of 16.2% in FY2022 (“occupancy cost” is the gross rental paid by tenants as a proportion of the tenants’ sales turnover).

Attractive rates right now should provide the REIT with wiggle room and pricing power to raise rents in future.

Solid financials and debt profile

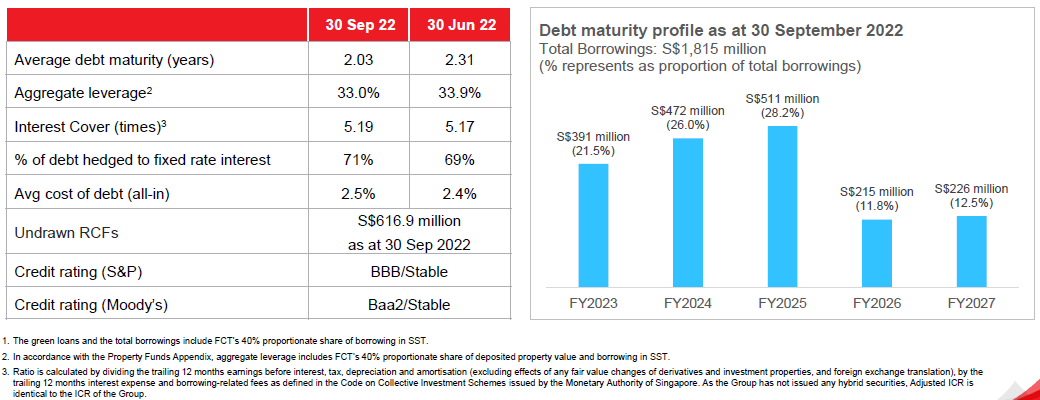

The suburban mall REIT also boasted an impressive debt and capital management profile as of the latest reporting period.

In terms of its aggregate leverage (or gearing ratio), Frasers Centrepoint Trust saw this fall to 33.0% as of 30 September 2022 from 33.9% the quarter before (see below).

Source: Frasers Centrepoint Trust H2 FY2022 earnings presentation

However, this will rise slightly and is expected to increase to around 35% post-the-acquisition of the additional 10% stake in Waterway Point in the middle of Q1 FY2023 (which was announced in September 2022).

Interest cover has also slightly improved while its average all-in cost of debt is still at a very much manageable level of 2.5%.

In terms of its lease expiries, it has 27.6% of its leases expiring in FY2023 and it has a relatively short weighted average lease expiry (WALE) of 1.87 years, by net lettable area (NLA).

A Singapore REIT focused on the local economy

Overall, the trends continue to be positive for Frasers Centrepoint Trust. The REIT saw its net asset value (NAV) per share rise slightly in FY2022, hitting S$2.33 as of 30 September 2022 – up from S$2.30 at the end of FY2021.

For Singapore investors, the REIT is a solid way of gaining exposure to the continued recovery of the Singapore consumer as the economy reopens and benefits.

Given its FY2022 full-year DPU, Frasers Centrepoint Trust shares are offering a dividend yield of 6.1% to investors.

The share price of the REIT has fallen over 13% so far in 2022 while its DPU has actually risen slightly for its FY2022.

Investors who believe that Singapore’s economy will continue to show solid growth may find Frasers Centrepoint Trust an interesting dividend investment option.

Disclaimer: ProsperUs Head of Content & Investment Lead Tim Phillips doesn’t own shares of any companies mentioned.