At the start of this month, Federal Reserve Chairman Jay Powell decided to hike interest rates again. That’s impacting all sorts of investments, in particular REITs.

And that matters in Singapore, given how many REITs are listed on the SGX. It also happens to be a period when many REITs are reporting their latest numbers.

One that recently reported was large cap, logistics-focused REIT Frasers Logistics & Commercial Trust (SGX: BUOU). It is also a constituent member of Singapore’s Straits Times Index (STI).

Towards the end of last week, Frasers Logistics & Commercial Trust announced its latest H1 FY2023 business update (for the six months ending 31 March 2023).

How did the Europe- and Australia-focused logistics powerhouse S-REIT, also known as FLCT, perform?

Here are some of the key takeaways for REIT investors and I answer the question of whether FLCT shares are worth buying now.

DPU falls, rental reversions positive

Of course, in this environment the big question is whether REITs can keep up their distribution growth. The bottom line is that this comes down to distribution per unit (DPU) growth.

On that front, FLCT had a poor showing – its H1 FY2023 DPU declined 8.6% year-on-year to 3.52 Singapore cents.

That was mainly due to lower H1 FY2023 revenue (down 11.7% year-on-year) and net property income (NPI) – which fell 13.4% year-on-year.

These falls were mainly attributed to the divestment of its Cross Street Exchange property in Singapore on 31 March 2022 as well as currency effects from a weaker Australian Dollar, Euro, and Great British Pound.

The REIT managed to renew a total of 84,500 square metres worth of leases in Q2 FY2023, achieving average positive rental reversions of +3.6% on an incoming vs. outgoing basis and +23.2% on an average-to-average basis.

A lot of this was driven by positive uplifts in its Logistics & Industrial (L&I) properties in Australia and Germany, with the segment delivering a +3.6%/+23.7% rental uplift in lease renewals.

FLCT occupancy stable, balance sheet remains healthy

During Q2 FY2023, FLCT’s overall portfolio occupancy remained stable at 95.9% as of 31 March 2023.

Its L&I segment maintained its 100% portfolio occupancy rate while the REIT’s Commercial segment saw portfolio occupancy of 89.8%.

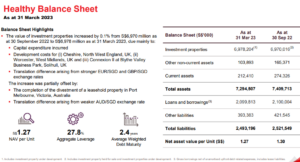

FLCT’s balance sheet remained pretty robust, with one of the lowest gearing ratios among all S-REITs – at 27.8% as of 31 March 2023 (see below).

Source: Frasers Logistics & Commercial Trust H1 FY2023 earnings presentation

The REIT continues to invest and has recently completed two developments in the UK – one in Worcester and the other in Blythe Valley Business Park – that management foresees contributing to top and bottom lines in FY2024.

However, FLCT’s net asset value (NAV) per unit of S$1.27 was down during H1 FY2023 from the S$1.30 as of 30 September 2022.

Low borrowing costs but uncertainty on the horizon

While FLCT has an extraordinarily low gearing ratio and a relatively solid pipeline of developments, it does also have around 50% of its debt coming due in FY2024 and FY2025.

So, while it has a low borrowing cost currently (of 1.8%) this could rise substantially when loans mature and get repriced from October 2023 onwards.

That’s particularly true if interest rates globally stay higher for longer than we currently anticipate. With over 50% of FLCT’s portfolio exposed to Australia, rates and the currency there also have an outsized impact on the REIT.

Unfortunately for unitholders, recently the Australian Dollar has been weak against the Singapore Dollar – impacting distributable income and DPU.

So – while FLCT shares currently yield 5.3% on a 12-month forward basis – with economic uncertainty on the horizon and higher interest rates set to stay, I think there are better S-REIT opportunities out there.

Disclaimer: ProsperUs Head of Content & Investment Lead Tim Phillips doesn’t own shares of any companies mentioned.