It’s been an earnings deluge in recent weeks with all manner of Singapore Exchange (SGX) companies posting quarterly numbers.

Towards the end of April, one of Singapore’s mega REITs – Mapletree Pan Asia Commercial Trust (SGX: N2IU) – released its Q4 FY2023 and FY2023 results (for the three and 12 months ending 31 March 2023, respectively).

Also known as MPACT, the REIT was the result of a merger between Mapletree Commercial Trust and Mapletree North Asia Commercial Trust that was completed in June 2022.

The Singapore REIT is a constituent member of the Straits Times Index (STI) and has 18 commercial and retail properties across Singapore, Hong Kong, Mainland China, Japan, and South Korea.

So, for dividend and REIT investors in Singapore, are MPACT shares worth buying for your portfolio following their latest earnings? Let’s find out.

Quarterly DPU flat, Singapore core assets show growth

Given the comparisons to the year-ago period – pre-merger – year-on-year comparisons for revenue and net property income (NPI) aren’t really applicable given the massive jump for both given the increased asset base.

However, what investors can find useful is the distribution per unit (DPU) and here there were positive signs.

For Q4 FY2023, MPACT’s DPU was flat at 2.25 Singapore cents – if you exclude the release of retained cash in the year-ago quarter.

In terms of the full-year FY2023, MPACT had a DPU of 9.61 Singapore cents, up 6.1% year-on-year (excluding the release of retained cash).

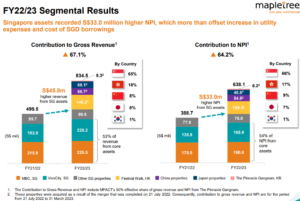

A lot of this positive business performance was driven by strength in its core Singapore assets – namely VivoCity and Mapletree Business City (MBC).

Indeed, both VivoCity and MBC contributed an extra S$33 million in NPI for MPACT in FY2023 versus their performance in the year-ago period (see below).

Source: Mapletree Pan Asia Commercial Trust Q4 FY2023 and FY2023 earnings presentation

VivoCity shines, Festival Walk stuck in the doldrums

For the full-year FY2023, VivoCity was the real growth driver for MPACT. The property’s revenue increased by 19.8% year-on-year while rental reversions came in at a positive +7.7% during FY2023.

Full-year tenant sales at VivoCity were up 30.6% year-on-year to S$1.05 billion and set a new record, exceeding pre-pandemic levels.

An asset enhancement initiative (AEI) that’s ongoing at VivoCity is set to be complete by the end of this month and will add an extra 56,000 square feet of retail space on L1.

Management expects the return on investment (ROI) of this AEI to be in excess of 20%.

This was in stark contrast to Festival Walk, the REIT’s flagship Hong Kong property, which saw negative rental reversions of -12.7% in FY2023 on the back of strict pandemic restrictions and a slow recovery even with the ongoing reopening.

There was an improvement in shopper traffic and tenant sales at Festival Walk but the overhang from the pandemic (at least in terms of rental reversions) looks likely to linger for a good part of FY2024.

Overall, MPACT’s portfolio generated positive rental reversions of just +0.7% in FY2023.

MPACT’s gearing slightly elevated

We all know how scared investors in S-REITs get when their gearing ratios exceed 40%. That’s despite the fact that the MAS-imposed cap is actually 50%.

So, for MPACT to report that its gearing ratio edged up slightly during the latest quarter – to 40.9% as of 31 March 2023 – wasn’t the best news for shareholders.

Meanwhile, the REIT’s weighed average all-in cost of debt was 2.68% as of 31 March 2023, up 28 basis points (bps) from the 2.40% from the year-ago period and up 11 bps (from 2.57%) as of 31 December 2022.

While only 11% of its debt is up for renewal in FY2024, there are concerns over MPACT’s office space in Singapore.

Management is guiding for reversions at MBC to be flattish going forward given office leasing could be challenging after recent retrenchments in the tech and financial sectors.

MPACT shares not looking that attractive

While MPACT’s share price is up nearly 5% so far in 2023, worries over its leverage are legitimate given its average term to debt maturity is 3.0 years, i.e. not that long.

Shares are trading at around book value but if I was a shareholder, I would be concerned over the timing of the recovery for Festival Walk (how long will that take?) plus the softness seen in some of the Singapore office space currently.

If there is a recession on the horizon, office space here could be further hit.

So, while MPACT shares offer investors a decent 12-month forward dividend yield of 5.5%, I feel like there could be a better entry point for this mega Singapore REIT further down the line.

Disclaimer: ProsperUs Head of Content & Investment Lead Tim Phillips doesn’t own shares of any companies mentioned.