We’re approaching the tail end of the quarterly earnings season for some of Singapore’s biggest companies.

So far, it’s been a mixed bag as the global macroeconomic picture still looks uncertain.

Meanwhile, in Singapore the economy continues to do well and certain sectors – like banks – have also benefitted from higher interest rates.

Last week, one of the biggest constituent stocks of Singapore’s Straits Times Index (STI) – Singapore Telecommunications Limited (SGX: Z74) – reported its Q3 FY2023 earnings (for the three months ending 31 December 2022).

Better known as “Singtel”, the city state’s largest telco has had a tough five years or so, with its share price down around 28% over that time period.

But is Singtel now turning a corner and is it worth a second look for those of us into buying dividend stocks? Let’s have a look at how its business performed during the latest quarter.

Underlying net profit rises by nearly 20%

On the top line, Singtel saw a slight decline in its operating revenue in Q3 FY2023 as it came in at S$3.71 billion – down 5% year-on-year (although up 6% on a constant currency basis).

Meanwhile, it was (as is normally the case with the large telco) the regional associates’ profit which buoyed Singtel’s underlying net profit.

Singtel owns large stakes in key telcos in other Asian countries, including Advanced Info Service (AIS) in Thailand, Globe Telecom in the Philippines, Telkomsel in Indonesia, and Bharti Airtel in India.

It was the last one – Airtel – which really helped propel its regional associates’ profit before tax (PBT) during the period (see below) as management noted Airtel’s continued “strong growth momentum”.

Source: Singtel Q3 FY2023 business update

In fact, as readers can see, without its regional associates, Singtel’s earnings during the quarter would have been down 8% year-on-year to S$288 million.

Optus earnings drag on Singtel

In Australia, Optus (Singtel’s wholly-owned Australian subsidiary) saw its earnings before interest and taxes (EBIT) fall 37% year-on-year to S$61 million.

That was as higher staff costs, the lingering impact of a cyberattack on Optus, and a weak Australian dollar all dragged on numbers.

Meanwhile, the cyberattack on Optus in Q4 2022 – which compromised the data of 10 million customers – resulted in a net subscriber loss of 65,000 before rebounding to positive net additions in the middle of December.

Yet while there was no known financial loss suffered by customers and provisions were made that were sufficient to cover costs, the longer term reputational damage inflicted is still too early to gauge.

And that’s an important aspect to assess for shareholders given that Optus made up over 50% of Singtel’s overall revenue during the latest quarter.

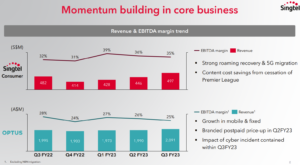

Singtel Consumer business sees strong recovery

Meanwhile, one of Singtel’s other core businesses – its own Singtel Consumer unit – saw revenue rise and EBIT come in at S$99 million, up 16% year-on-year and up 21% quarter-on-quarter.

That was led by mobile services on a strong rebound in roaming revenue (no doubt with the resumption of international travel) and higher prepaid revenue – from 5G and the return of foreign workers.

This recovery in revenue (see below) is likely to continue in the coming quarters as international travel gets back to its pre-Covid levels.

Source: Singtel Q3 FY2023 business update

How about the Singtel dividend?

Of course, for many Singapore investors, Singtel’s dividend is one big reason why they buy shares of the telco.

Yet, as we’ve seen in the past, it’s not the most sustainable dividend given its had an extremely high payout ratio in recent years.

In FY2022, Singtel paid a dividend per share (DPS) of 9.30 Singapore cents, which worked out to a dividend payout ratio of 80% of underlying net profit – on an earnings per share (EPS) basis.

In H1 FY2023, that improved slightly to 76% of underlying net profit but, for me personally, that’s still too high for comfort.

Remember that as recently as FY2019, Singtel was paying a DPS of 17.50 Singapore cents – which at that point was 101% of its underlying net profit. Not exactly sustainable.

If Singtel can get its dividend payout ratio down to a range of 50-60%, I’d be more comfortable with it as a reliable dividend payer.

Solid results but Singtel shares not compelling

It was a decent quarter for Singtel, buoyed by the impressive results coming out of its regional associates as well as a rebound in its own Consumer business.

However, with shares down around 4% so far in 2023 and only yielding 3.8% on a trailing 12-month basis, Singtel shares aren’t that compelling from either a growth or dividend income perspective.

Growth initiatives, such as its GXS Bank, don’t offer clear enough visibility on either the top or bottom line.

For income investors looking for either dividend yield or growth, there are better alternative options in both Singapore and abroad.

Disclaimer: ProsperUs Head of Content & Investment Lead Tim Phillips doesn’t own shares of any companies mentioned.