Genting Singapore Ltd (SGX: G13), a prominent player in the hospitality and casino industry, presents an interesting opportunity for retail investors considering its current business trajectory and future prospects.

Here is why placing your chips on Genting Singapore could be the right move for you now.

1. Robust Financial Resilience

Despite some challenges, the overall business momentum of Genting Singapore remains robust.

- EBITDA Margins: There was a notable dip in EBITDA margin to 35.2% in the last quarter of FY23 from 50.1% in the previous quarter. This reduction was largely due to S$92 million in bad debt losses recognized recently. However, if we exclude these losses, the margins would have been much healthier, between 44-46%.

- Bad Debt Impact: The rise in bad debt is mainly due to credits extended to VIP gamblers, a common practice in the industry. It is important to note that the company often successfully recovers a part of these debts later on.

- Cost Management: Costs related to staff and utilities are well-controlled, contributing to a stable operational foundation.

2. Rapid Tourism Recovery

Source: Singapore Tourism Analytics Network

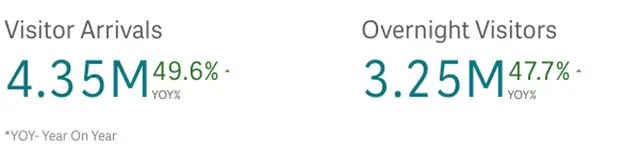

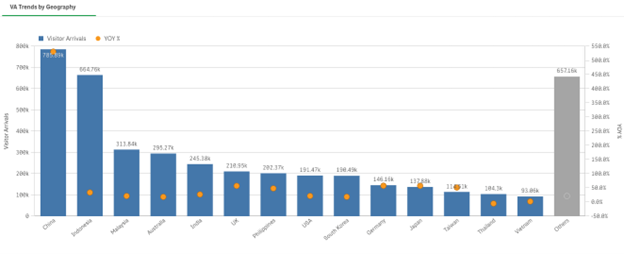

Tourism is a vital component of Genting Singapore’s business and the sector’s recovery continues to gain momentum.

During the Q1 2024, international arrivals increased by 49.6% year-on-year (yoy) to 4.35 million visitors. With increasing tourist arrivals, especially following extensions of visa-free travel for key demographics like Chinese tourists and a packed calendar of events in Singapore, Genting Singapore is well-positioned to benefit it.

Chinese tourists arrivals to Singapore during the Q1 2024 increased by 530.9% yoy.

Source: Singapore Tourism Analytics Network

3. Dividend Jackpot

The final dividend recently was 2.0 cents per share, which was lower than expected. However, future dividends are expected to increase as earnings grow. The forecast for FY24 is a dividend per share of 4.0 cents, matching the pre-pandemic levels of FY19, with an anticipated increase to 5.0 cents by FY25. This would translate into an attractive yield of around 4 to 5% based on its current share price.

4. Development and Expansion Plans

Genting Singapore is actively enhancing its facilities, which should drive growth in the long-term.

- Ongoing Upgrades: The company is renovating hotels, food and beverage outlets, attractions, and the casino. Key projects like the revamped Forum area, Minion Land at Universal Studios, and the Singapore Oceanarium are expected to complete by 2025.

- New Developments: Plans for a new waterfront development with 700 hotel rooms are underway, with construction contracts likely to be awarded soon.

5. Attractive valuation

The recovery of the tourism industry and return of Chinese tourists could keep revenue growth robust. Our analysts have a “Buy” call for Genting Singapore with a target price of S$1.15, representing an upside of 23.7%. With a decent yield of 4% and a potential improvement in its earnings, this could represent a favourable entry point for investors looking to capitalise on the company’s future growth and profitability. While Genting Singapore faces competition from Marina Bay Sands, which has seen significant growth, Genting’s strategic renovations and expansions are set to enhance its competitive edge in the long-term.

Conclusion

Investing in Genting Singapore is like playing a strong hand in a high-stakes game. The company’s robust financial performance, strategic expansion, attractive dividend payouts, tourism sector recovery, and compelling valuation equip it to provide significant returns. However, potential investors should be aware of the inherent risks associated with the volatility of the tourism industry and potential challenges in debt collection from VIP gamblers. As always, while the upside potential is appealing, it is crucial to consider these risks alongside the company’s strengths. Betting on Genting Singapore may offer high rewards, but like any investment, it comes with its share of risks.

Disclaimer: ProsperUs Head of Content & Investment Lead Billy Toh doesn’t own shares of any companies mentioned.