Earnings season in Singapore appears to be petering out, given most of the biggest companies have reported their latest numbers.

We’ve already seen Singapore’s biggest bank report a strong set of quarterly earnings. But the other two big banks only report this week.

First up was United Overseas Bank Ltd (SGX: U11), better known as UOB, which reported its latest H2 2022 and FY2022 earnings earlier today (23 February) before the market opened.

So, what should investors know about the Southeast-Asia focused bank’s latest earnings? And did shareholders see a hike in the dividend?

Here are three big takeaways from UOB’s latest results for lovers of bank stocks.

1. UOB’s NII and NIM up strongly

Overall, it was a solid showing from UOB that saw its net profit come in roughly in line with consensus expectations.

The bank’s Q4 2022 net profit of S$1.15 billion was up 13% year-on-year but was down 18% quarter-on-quarter given one-off expenses for the integration costs for the Citigroup Inc (NYSE: C) business in Thailand and Malaysia.

However, net interest income (NII) in Q4 2022 surged by 53% year-on-year to S$2.56 billion. This figure was also up by 15% sequentially from Q3 2022.

Meanwhile net interest margin (NIM) hit 2.22%, up 27 basis points (bps) from 1.95% in Q3 2022 (see below).

Unsurprisingly, UOB has benefitted from higher interest rates from the US Federal Reserve (Fed) – like many of its banking peers in Singapore.

Source: UOB H2 2022 and FY2022 earnings presentation

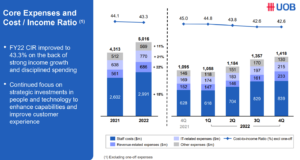

2. Cost-to-income ratio stable

One of the biggest issues for companies globally has been pulling off growing its profits while keeping its costs in control.

Thankfully for UOB shareholders, the bank has been effective at keeping its cost-to-income ratio stable during Q4 2022 – even as income rose.

For investors, the lower the number, the better. The cost-to-income ratio for UOB has been a on a downward trend since the beginning of 2021 (see below).

As a result, UOB’s cost-to-income ratio for FY2022 was down by 80 bps to 43.3%, a significant improvement from the 44.1% in FY2021.

Source: UOB’s H2 2022 and FY2022 earnings presentation

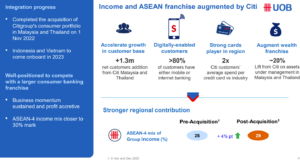

3. Citi integration on track, final dividend rises 25%

Finally, UOB’s planned acquisition of Citi’s retail businesses in Thailand, Malaysia, Vietnam, and Indonesia is going to plan.

The bank completed the acquisition of the Thai and Malay portfolios in November 2022 while the Indonesia and Vietnam ones look set to come onboard some time this year.

This should bolster UOB’s business in the ASEAN region and, post-acquisition, the bank predicts that the four countries will contribute just shy of 30% to the group’s income.

That would be up from 25% pre-acquisition while the increased customer base, as well as upsell and cross-sell opportunities in the cards and wealth divisions, should drive business momentum (see below).

Source: UOB’s H2 2022 and FY2022 earnings presentation

Elsewhere, the bank declared a final dividend per share (DPS) – for H2 2022 – of 75 Singapore cents. That’s a juicy 25% increase from the FY2021 final dividend of 60 Singapore cents.

Based on the 75 Singapore cent level, UOB’s dividend payout ratio is at a comfortable 50%.

On the fee income front, weakness in wealth and fund management saw fee income drop sequentially in Q4 2022 from the prior quarter. This was partially offset by strength in its credit card business.

UOB franchise looks as solid as ever

While UOB delivered a strong set of earnings, its share price still fell by up to 4% in response to its latest numbers.

There might have been some disappointment that NII and NIM weren’t stronger yet investors can’t complain about the attractive yield on offer for both stability and potential growth this year in the ASEAN region.

Based on UOB’s latest share price of S$29.70, dividend investors are being offered a 12-month forward dividend yield of 5.1%.

Disclaimer: ProsperUs Head of Content & Investment Lead Tim Phillips doesn’t own shares of any companies mentioned.