Volatility in the stock market continues, even as the US Federal Reserve (Fed) raised its benchmark interest rate by 75 basis points (bps) – its most aggressive hike since 1994.

With this rate hike, the Federal Open Market Committee (FOMC) took the level of its benchmark funds rate to a range of 1.5%-1.75%, the highest since before the COVID-19 pandemic.

Stocks were volatile after the decision, but the market actually turned positive following Fed Chairman Jerome Powell’s press conference.

Officials, however, have also cut their 2022 economic growth outlook significantly to a 1.7% gain in GDP, from 2.8% in March.

With so much uncertainty, I believe investors should buy this defensive aerospace & defense company; Northrop Grumman Corporation (NYSE: NOC).

I have written about the need to diversify into aerospace & defense companies back in February and talked about Northrop Grumman’s strength as the defense company to own for the decade.

Since then, the share price of Northrop Grumman has increased by 17.3% to its closing of US$458.45 per share. This is in stark comparison with the S&P 500 Index, which has just entered into a bear market.

Despite the outperformance against the overall market, Northrop Grumman’s share price was also affected by the overall bearish sentiment.

Slightly over a week ago, the share price of Northrop Grumman fell by 6.8%.

I believe the current pullback provides an opportunity for investors to buy Northrop Grumman to withstand the market volatility.

Here are some of the company’s updates since I last wrote about them.

1. Robust backlog orders of over 2x annual sales

Northrop Grumman’s Q1 FY2022 was a good quarter for the company with more bookings than expected.

It has a robust backlog order of US$76 billion, which is more than twice that of Northrop Grumman’s annual sales.

This provides the foundation for growth going forward.

In fact, the Department of Defense (DoD) has just awarded Northrop Grumman and Owl Cyber Defense Solutions a new contract with the Missile Defense Agency (MDA) worth a total of US$240 million.

2. Guidance for FY2022 remains despite weakness in Q1 FY2022

The earnings in Q1 FY2022 were affected by COVID-19 disruptions on productions.

Sales during the period totalled US$8.8 billion, which represents a decline of 4%.

According to the management, there were some disruptions on productions at the beginning of the year due to COVID-19 but the impact on volume has receded as the quarter progressed.

Despite the weakness in sales due to production, Northrop Grumman delivered a segment operating margin of 11.8%, in line with projections.

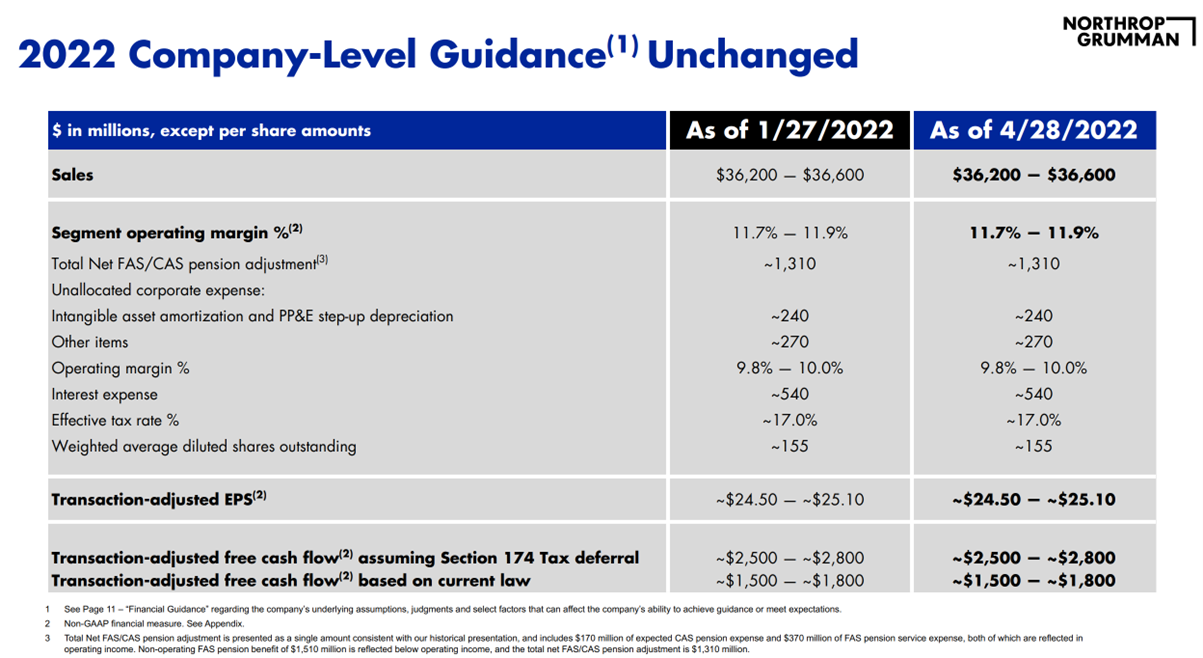

While it will be great if management could provide more clarity on the margin and revenue pressures going forward, it did maintain its guidance despite the weaker Q1 FY2022.

Sales are expected to be in the range of US$36.2 billion to US$36.6 billion for FY2022 while operating margin is expected at between 11.7% to 11.9%, resulting in a US$24.50 to US$25.10 adjusted earnings per share.

Source: Northrop Grumman’s Q1 FY2022 Results Presentation

3. Revenue growth will accelerate into FY2023

Management also expects revenue growth to accelerate from the 2H FY2022 and carry onto FY2023, from the low-single digit growth in its FY2022 guidance.

By FY2024, Northrop Grumman expects to deliver a segment operating margin rate of about 12%.

This is based on bipartisan support in the US to increase its defense budget.

Congress finalised the fiscal year 2022 defense appropriations in March and the administration has since issued the fiscal year 2023 defense budget request.

Both of these base budgets show solid 4% to 5% top line growth with additional potential in supplemental funding.

Based on initial indications from Congress, the final fiscal year 2023 appropriations could be even higher than the initial request as Congress looks to address the evolving threat landscape, but also to offset inflationary pressures.

The FY2023 budget request includes an 8% increase over FY2022, including funding ongoing programmes such as Artemis and new initiatives for Moon to Mars efforts.

4. Dividend raised by 10% to S$1.73

Northrop Grumman also declared S$1.73 quarterly dividend per share (DPS), which is a 10.2% increase from its prior quarterly dividend of S$1.57.

This puts the dividend yield at 1.5%.

Northrop Grumman benefits from increasing threat levels

As a defense company, Northrop Grumman will benefit from the increasing threat level in the world while it is shielded from inflation.

The downside risk remains that a defense company is not immune to recession fears. However, defense names usually have long-term contracts with governments, which help them lock in revenue.

Disclaimer: ProsperUs Investment Coach Billy Toh doesn’t own shares of any companies mentioned.