If you’ve ever taken a Grab or Go-Jek then you’ll be familiar with ride-hailing. In North America, though, the ride-hailing industry is dominated by Uber Technologies Inc (NYSE: UBER) and Lyft Inc (NASDAQ: LYFT).

Lyft shares yesterday surged by 9.6% on its latest earnings after the number two ride-hailing company guided for an 11-15% jump in fourth quarter revenue (compared to its latest third quarter).

Never mind the fact that Lyft also projected an adjusted EBITDA loss of between US$190-200 million. I’ve previously written about Uber and unappealing unit economics of the ride-hailing industry (where increasing scale does not lead to higher profits).

In Lyft’s case, it’s probably even worse. That’s because Lyft focuses solely on ride-hailing and is the number two player in the market.

That’s in contrast to Uber, which is number one and at least has a fast-growing and somewhat profitable food delivery business.

Taking a Lyft during Covid-19

Both Lyft and Uber shares popped on the supposedly “positive” outlook from the former.

The key question investors should be asking themselves before even looking at Lyft is; would I get into a ride-hailing car while Covid-19 rages on in North America?

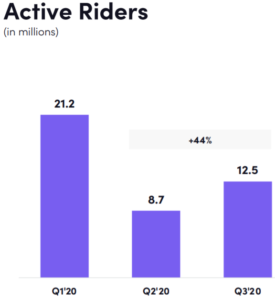

It’s somewhat scant consolation that active rider numbers for Lyft appear to have bottomed in the second quarter (see below).

However, I wouldn’t be surprised to see perhaps another drop in the first quarter of 2021 as the worst of the winter weather takes hold in North America and people stay indoors and continue to work remotely (taking less Lyft rides in the process).

Source: Lyft Q3 2020 earnings supplement

Third-quarter revenue for Lyft plunged by 48% year-on-year to US$499.7 million. Its adjusted net loss for the third quarter also ballooned to US$280.4 million from the US$121.6 million in the third quarter of 2019.

Cost cutting? Show me the profits

The fact of the matter is that Lyft, like Uber, has an extremely unclear path to profitability. The fact that a projected adjusted EBITDA loss in the range of US$190-200 million is considered “positive” says it all about the growth story of this stock.

According to Evercore ISI analyst Benjamin Black, the revised Lyft outlook suggests that “cost cutting initiatives are paying real dividends” and that the latest update has “only strengthened the thesis around Lyft’s improving cost structure”.

That made me laugh. When has cost-cutting your way to growth ever worked out as an ideal long-term and sustainable business strategy?

Lyft shares, even after yesterday’s pop, are down around 35% since its IPO in early 2019. If investors want to create long-term wealth in their portfolio then passing on this shared ride would be a good idea.

Disclaimer: ProsperUs Head of Content doesn’t own shares of any companies mentioned.