Among some of the companies that were affected by the ongoing Russia-Ukraine war is Taiwan Semiconductor Manufacturing Company Ltd (NYSE: TSM) (TPE: 2330), also known as TSMC.

This is as Taiwan is a geopolitical hotspot given its historically tense relations with China and its vulnerability has been under more scrutiny ever since Russia’s invasion of its smaller neighbour, Ukraine.

Some political experts believe that Russia’s military operation could embolden China to consider invading Taiwan in the future and the rhetoric has only gotten louder.

TSMC’s share price has been affected since the invasion and has posted a decline of 14.3% to US$106.72 per share during that time.

Aside from that, Russia and Ukraine are major exporters of palladium and neon – both of which are used to make semiconductors.

While chipmakers have downplayed the potential impact on the semiconductor supply chain so far, a worsening Russia-Ukraine war will hit the global supply chains that are already constrained due to the pandemic.

Despite these uncertainties, I think TSMC’s current share price weakness represents a great opportunity for long-term investors to own the world’s largest semiconductor foundry.

Here are five reasons why I think investors should consider adding TSMC into their portfolio.

1) TSMC is the world’s largest semiconductor foundry

As the world accelerates into the digital world in the post-COVID era and amid the rollout of 5G networks globally, I expect to see a surge in demand for the electric & electronics (E&E) space.

The rise of the Internet of Things (IoT), automation of manufacturing processes, electric vehicles (EVs), migration to cloud data, the Metaverse and a shift towards the digital world will take place at a much faster pace in the future.

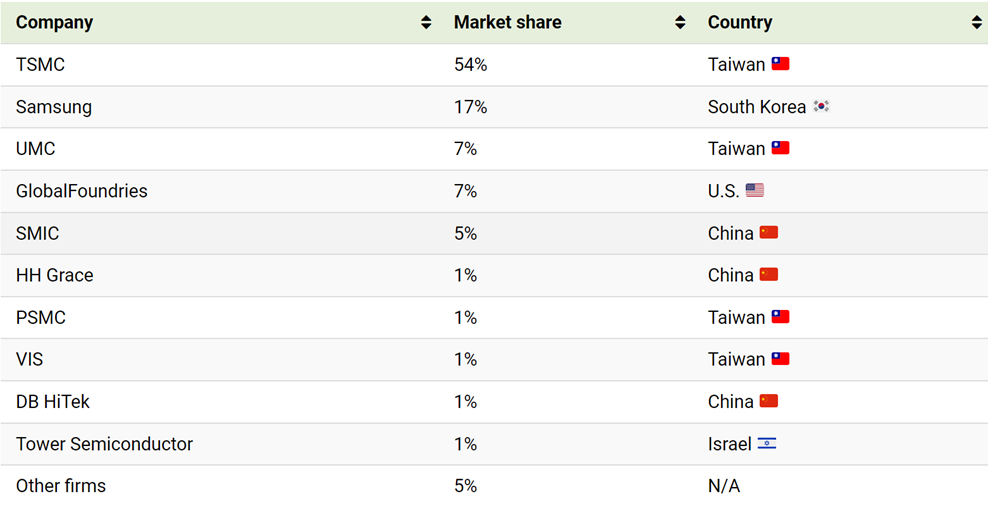

TSMC, which is the world’s largest semiconductor foundry, will benefit from the surge in demand. It has more than a 54% market share in the global fabrication (or production) of semiconductor chips.

Source: Visual Capitalist, ProsperUs

Source: Visual Capitalist, ProsperUs

Its large size gives TSMC an advantage and the company’s customers include Apple Inc. (NASDAQ: AAPL), Advanced Micro Devices Inc (NASDAQ: AMD), Qualcomm Incorporated (NASDAQ: QCOM), and NVIDIA Corporation (NASDAQ: NVDA).

2) Strong competitive advantage with the smallest chips

TSMC leads the way in the fab industry as the company produces the smallest chips. In the semiconductor industry, the smaller and more powerful chips are technologically better.

The company currently leads with its new 5nm nodes chips, which are being supplied to Apple for its M1, M1 Pro and M1 Max chips.

TSMC is also expected to start its mass production for its 3nm process by 2023. The future Apple Silicon Macs have been reported to use 3nm chips with up to 40 cores.

To put this into context, Intel Corporation (NASDAQ: INTC) saw a delay in its 7nm chip production due to production issues and had to turn to TSMC to help with production, which is expected by 2023.

Meanwhile, Samsung Electronics Co Ltd (KRX: 005930) (LSE: BC94) also saw that its 3nm process was not up to scratch for Qualcomm, and it too would have to contract TSMC for its future 3nm nodes, according to reports.

TSMC’s competitive strength is evident as other big fab players, such as Intel and Samsung, have had to turn to it for advanced chips production, such as the 3nm nodes.

3) Benefit from ongoing chip shortages

The ongoing chip shortages seen in 2021 are expected to continue this year and could even extend into 2023 for some products.

With the ongoing chip shortages, this gives TSMC a strong negotiating position.

Price increases are expected to materialise in a tight market and TSMC has also been forecasting margin expansion this year.

4) Strong financial track record

Aside from that, TSMC also has a strong financial track record.

The group’s revenue has a compounded annual growth rate (CAGR) of 14.0% for the past 10 years and has seen a sharp increase of 18.5% over the last one year.

Its five-year average net profit margin stood at a comfortable level of 35.5%. This is good as it indicates that TSMC has the capacity to pass on cost increases to its clients – especially in an inflationary environment.

TSMC also has a strong balance sheet with a cash balance of US$43 billion while debt remains manageable at around US$27 billion.

5) Strong growth guidance

TSMC’s outlook for the first quarter of its financial year 2022 (1Q FY2022) is very encouraging as management provided guidance of sequential growth of 10% in revenue while gross margin and operating margin expansion are expected at around 150 basis points, respectively.

The combination of higher revenue and better margins point to strong earnings growth in the coming quarter.

It is even more impressive considering that the quarter included the Chinese New Year holidays, which is usually a slower quarter.

With demand for E&E expected to remain strong going forward, the growth potential for TSMC remains strong.

Buy the dominant leader

I think investors should take advantage of the current price weakness to gradually build a position in TSMC shares, given the company is the dominant player in the fabrication industry.

Considering the rising importance of semiconductors and chips, I think long-term investors will benefit from its advantage in terms of size, leadership, technology and financial strength.

However, investors should also consider the downside risks. These include geopolitical risks, especially involving China, as well as the intense competition in the space with Intel’s reinvention under new CEO and its IDM 2.0 Strategy.

Disclaimer: ProsperUs Investment Coach Billy Toh doesn’t own shares of any companies mentioned.