In the current market, we have seen a shift from growth stocks to value stocks.

The central theme that is driving this rotation away from growth into value is the return of inflation.

The economic rebound from the COVID-19 pandemic, massive shortages of raw materials and continued disruptions of global supply chains, labour and logistic bottlenecks have caused a surge in inflation.

One of the companies that benefits from this rotation is The Coca-Cola Company (NYSE: KO).

I’ve written about the three key reasons to buy Coca-Cola back in March, and I think the latest earnings result validate some of those views.

Coca-Cola earnings beat analysts’ expectations as revenue jumped 16% during the first quarter of 2022 (Q1 FY2022) to US$10.5 billion. Wall Street’s analysts’ average estimate came in at US$9.83 billion.

Meanwhile, earnings per share (EPS) for the quarter increased to 64 US cents per share from 52 US cents per share a year ago, beating the average estimate of 58 US cents per share.

Looking beyond the headlines, here are three positive takeaways from Coca-Cola’s latest earnings in Q1 FY2022.

1. Strong organic sales growth

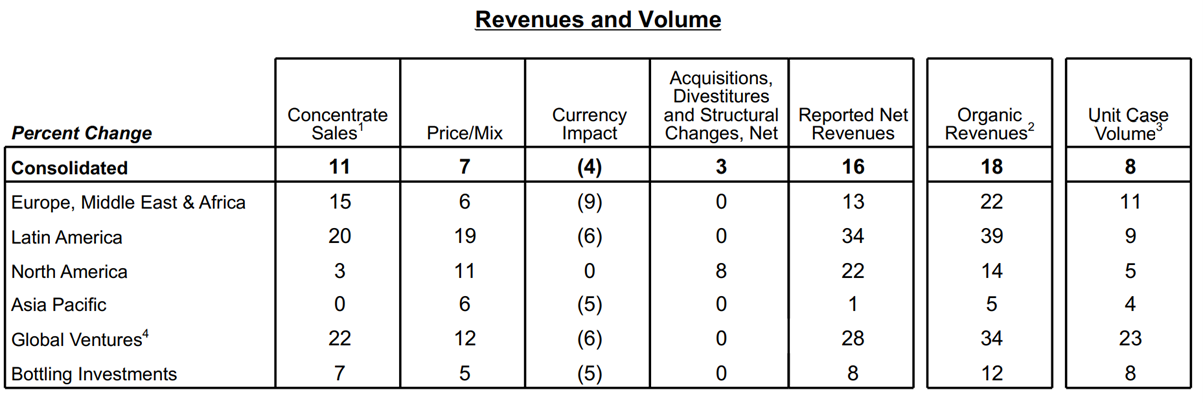

First off, I was impressed by Coca-Cola’s strong organic sales and the recovery of the company is proceeding faster than I expected (see table below).

During the quarter, Coca-Cola’s organics sales grew by 18%. In comparison, most analysts were only expecting growth in the 9% range.

The strong organic growth was led by its volume growth of 8%, with broad-based growth seen across all operating segments.

Developed markets, developing and emerging markets all recorded high-single digit growth.

Growth in developed markets was led by the US and the UK while growth in developing and emerging markets were led by Brazil and India.

Source: Coca-Cola’s Q1 FY2022 Earnings Release, ProsperUs

Source: Coca-Cola’s Q1 FY2022 Earnings Release, ProsperUs

2. Expanding margin

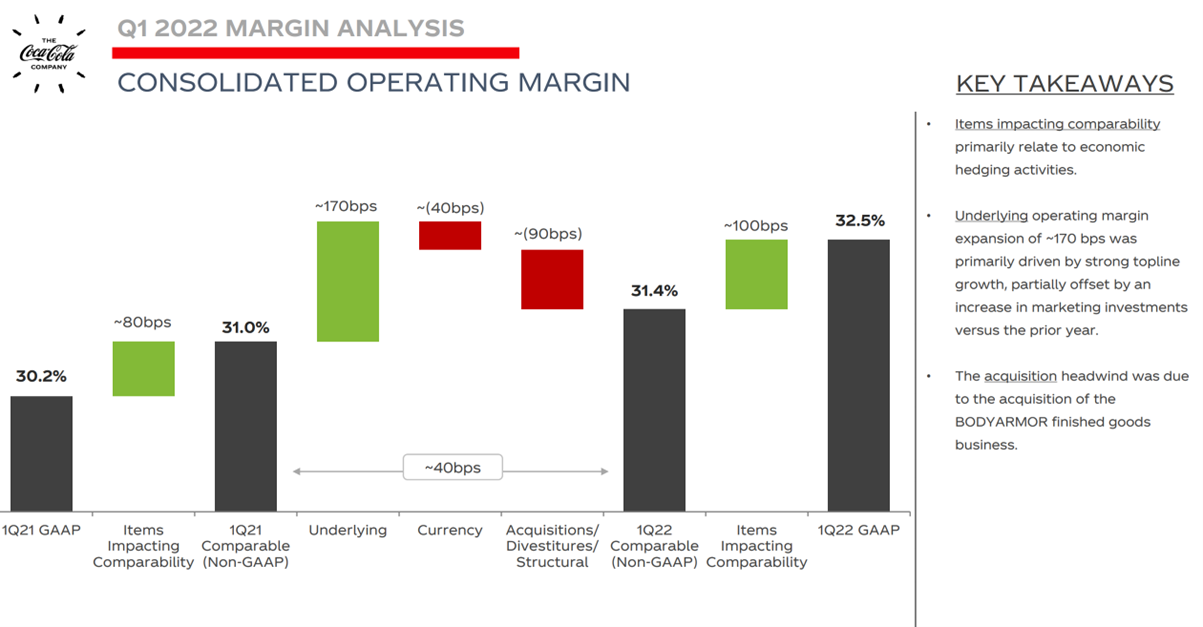

While I do not expect Coca-Cola to be immune to the rising input costs and inflationary pressures, the company’s latest earnings are testimony to the company’s pricing power.

The pricing and mix of Coca-Cola, which is the pricing across its portfolio, rose by 7% during the quarter, driven by strategic pricing, revenue growth initiatives, improvement in away-from-home channels in most markets as well as a positive segment mix.

The operating margin (GAAP), which included items impacting comparability, increased to 32.5% in the current quarter as compared to 30.2% in the prior year.

Meanwhile, comparable operating margin (non-GAAP) stood at 31.4% in Q1 FY2022 versus 31.0% in Q1 FY2021.

Source: Coca-Cola’s Q1 FY2022 Margin Analysis, ProsperUs

Source: Coca-Cola’s Q1 FY2022 Margin Analysis, ProsperUs

3. More upside with global reopening

Coca-Cola ventured into the hot beverages market for the first time when it acquired Costa Coffee in 2019.

While the timing of the acquisition was affected by the COVID-19 pandemic, the reopening of the world could see further recovery going forward.

The company created a new business segment known as “Global Ventures” to house the acquisition of Costa Coffee.

It also includes other brands such as Monster beverages, innocent juices and smoothies as well as Dogadan tea.

Almost 90% of the revenue for the business segment comes from Costa Coffee and it saw a year-on-year increase of 28% in net revenue during the quarter.

The management has highlighted that the non-retail business of Costa, the Express Machine, which is a vending digital barista machine, saw a strong quarter as transactions surged amid the reopening globally.

Coca-Cola’s CEO, James Quincey, said that the company will focus on placement of new machines across Europe, the Middle East and in China.

The impact of the lockdowns has made it harder for new placement in recent months, but the reopening of the world will help it to sustain growth.

Costa’s ready-to-drink beverages has also done very well, and growth will continue with launches in some European markets.

Strong dividend track record offers defensive positioning

Despite the strong earnings in the Q1 FY2022, Coca-Cola’s growth in the near term will remain patchy due to the ongoing geopolitical conflicts.

There is also uncertain consumer sentiment amid the increasingly inflationary environment, accelerated cost pressures and ongoing supply chain issues.

And with the evolution of the pandemic but, seen from the earnings recovery, Coca-Cola is in a better position to adapt to these market conditions.

This is in line with the guidance provided by the management, which said they expected “recovery in 2022 to be asynchronous.”

I also believe that Coca-Cola’s strong marketing brand and its pricing power will allow the company to better navigate the inflationary environment as compared to its peers.

The company’s strong dividend track record also offers a defensive proposition to investment portfolios amid the rising interest rate environment.

Disclaimer: ProsperUs Investment Coach Billy Toh doesn’t own shares of any companies mentioned.