-

Tesla managed to deliver on earnings despite ongoing supply chain challenges, logistics bottlenecks and an inflationary environment

-

Tesla’s earnings were mainly driven by higher pricing and deliveries of EVs but reliance on regulatory credits posed downside risks

-

Tesla’s leadership in its core technology and other factors offer a lot of optimism but I think the premium is too high

Electric vehicle (EV) giant Tesla Inc (NASDAQ: TSLA) smashed Wall Street estimates for revenue and profit in another quarter despite ongoing supply chain challenges.

For the first quarter of its financial year 2022 (1Q FY2022) earnings, Tesla reported revenue of US$18.8 billion as compared to analysts’ expectations of US$17.9 billion. It was an increase of 81% from the same quarter a year ago.

Excluding special items, Tesla’s profit for the quarter stood at US$3.22 per share, easily beating the US$2.27 average of analysts’ estimates. It is even more impressive when we consider its 246% growth from a year ago.

The headline numbers are impressive, and investors are excited about the prospect of the leading EV manufacturer.

I looked at Tesla’s financial numbers to see how good the company really is and here are four key highlights to take away from Tesla’s record-beating quarterly earnings.

1. Strong double-digit growth

One of the first things that I noticed is the strong double-digit growth for Tesla.

The 1Q FY2022 reached the highest deliveries, profit and operating margin of 19% despite the chip shortages, logistics challenges and an uncertain external macro environment.

The higher pricing adopted by Tesla has helped contribute to the EV manufacturer’s improved financial performance.

With higher pricing in its backlog orders, this will help Tesla to offset some of the external headwinds.

Both Elon Musk, CEO of Tesla and Zachary Kirkhorn, CFO of Tesla, have expressed confidence that Tesla will achieve a 50% growth in vehicle production in 2022 versus 2021.

Given the strong demand and backlog of orders, the company is likely to maintain its strong double-digit growth in FY2022.

2. Strong cash position

I always love companies with a strong cash position and Tesla is one of them.

The company is currently sitting with US$18.0 billion in cash and its debt level (excluding product financing) is near to zero.

This represents an increase of about 2.0% in its cash position as compared to a year ago.

In terms of its debt for vehicle and energy product financing, it is at US$3.3 billion level, which was about 23% lower than what it was back in the 1Q FY2021.

The strong cash position gives Tesla the advantage to spend big on areas with strong growth potential in the future.

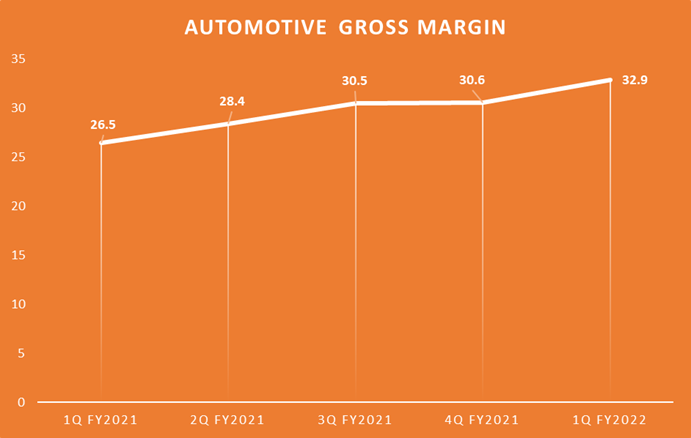

3. Gross margin boost

Automotive gross margin continues to improve in the 1Q FY2022, even in the face of rising inflation. Higher pricing has also helped Tesla’s financial performance.

It is worth nothing that cars delivered in the 1Q generally carried pricing set in the prior quarters and are at levels lower than cars being ordered today.

This will support the margin expansion, but downside risk remains as Tesla’s per unit vehicle costs have also increased.

Inflation, raw material prices, and logistics costs continued to impact Tesla’s cost structure.

Source: ProsperUs, Tesla’s 1Q FY2022 Earnings Update

Source: ProsperUs, Tesla’s 1Q FY2022 Earnings Update

4. Reliance on regulatory credits posed downside risk

Regulatory credits have been one big point that bears have trumpeted over time.

During the 1Q FY2022, Tesla reported revenue from these credits of US$679 million, more than double the US$314 million reported in the previous quarter.

Management has clarified during earnings calls that this was mainly due to a one-time benefit of US$288 million from credit revenue relating to a regulatory change in the US CAFE penalty.

For those of you who do not know what regulatory credits are, it is basically credits given to carmakers that build and sell environmentally-friendly vehicles.

In the US, there are rules that require automotive manufacturers to produce a certain number of so-called zero-emission vehicles (ZEV) based on the total number of cars sold.

These car makers are required to have a certain amount of regulatory credits each year and if they can’t meet this target, they have to buy from other companies that have excess credits.

Since Tesla only sells EVs, which are under the ZEV category, the company always has excess regulatory credits and can effectively sell them at a 100% profit.

However, since there is a shift towards EVs, even among legacy automakers, the reliance on the regulatory credits is not sustainable.

Tesla earnings impressive but it’s still expensive

If there’s one thing you can take away from Tesla’s 1Q FY2022 financial results, it is a company that has delivered on earnings and which is at the forefront of their industry.

Given its leadership in the core technology, its strong cash position, impressive margins and growth as well as the ramp-up of its Gigafactory in Berlin, there are a lot of reasons to be optimistic about the company.

Bear in mind that the strong performance was achieved despite the external challenges, such as inflationary pressure, shortages within the supply chain as well as the logistics bottlenecks.

While I think Tesla can maintain its strong earnings performance at least in the near term, its share price remains at a level that is too expensive for my liking.

With a forward price-earnings (PE) of more than 100x and a trailing PE of 200x, I think the premium is too high.

Having said this, investors who are passionate about renewable energy and EVs might find that it is worth paying the premium for a revolutionary player in the industry.

Disclaimer: ProsperUs Investment Coach Billy Toh doesn’t own shares of any companies mentioned.