In a world of uncertainty amid rising geopolitical tension and the tightening of monetary policy, I believe Johnson & Johnson (NYSE: JNJ) is an ideal investment choice for risk-averse investors.

The drugmaker and consumer products leader is one of the leading stocks that offers stability through its diversified business model.

Following J&J’s first-quarter 2022 earnings (1Q FY2022), the company’s share price gained by 3.1% as its adjusted net profit of US$2.67 beat analysts’ average estimate of US$2.59.

However, as a long-term investor, I try to avoid being caught up with the initial reaction of the stock market and instead focus on the underlying business model.

Here are five key takeaways for investors from J&J’s latest 1Q FY2022 earnings.

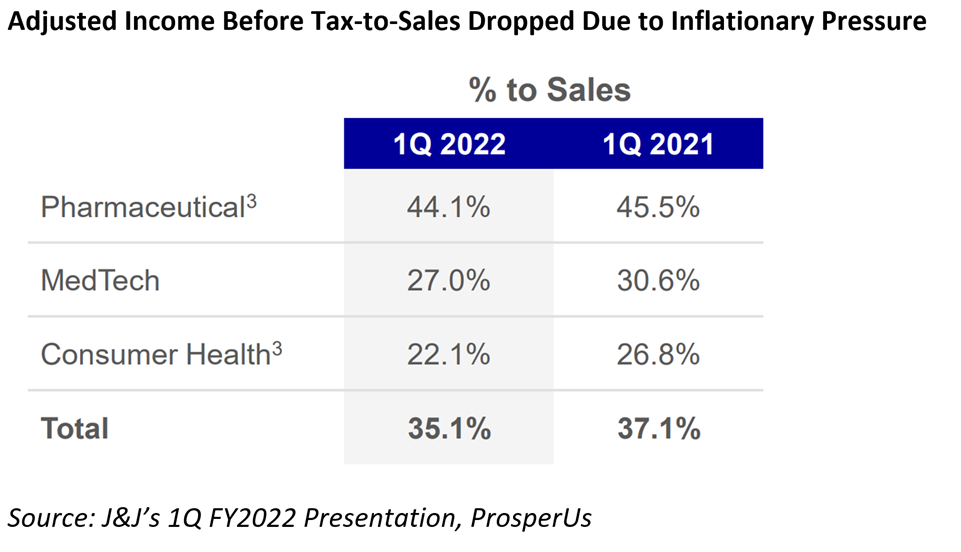

1. Inflationary pressure eats into margin

One of the most obvious impacts from the 1Q FY2022 earnings is the impact of higher inflation as well as higher input costs.

J&J’s adjusted income before tax (as a percentage of sales) dropped to 35.1% in 1Q FY2022 from 37.1% in 1Q FY2021.

Among some of the reasons for the decline in margin were changes in product mix, commodity inflation and increased brand marketing expense.

Among some of the key drivers of inflationary pressures include shortages and rising prices of commodities, increased costs for labour, energy and transportation.

These impacts are most notable in J&J’s Consumer Health business segment (see below).

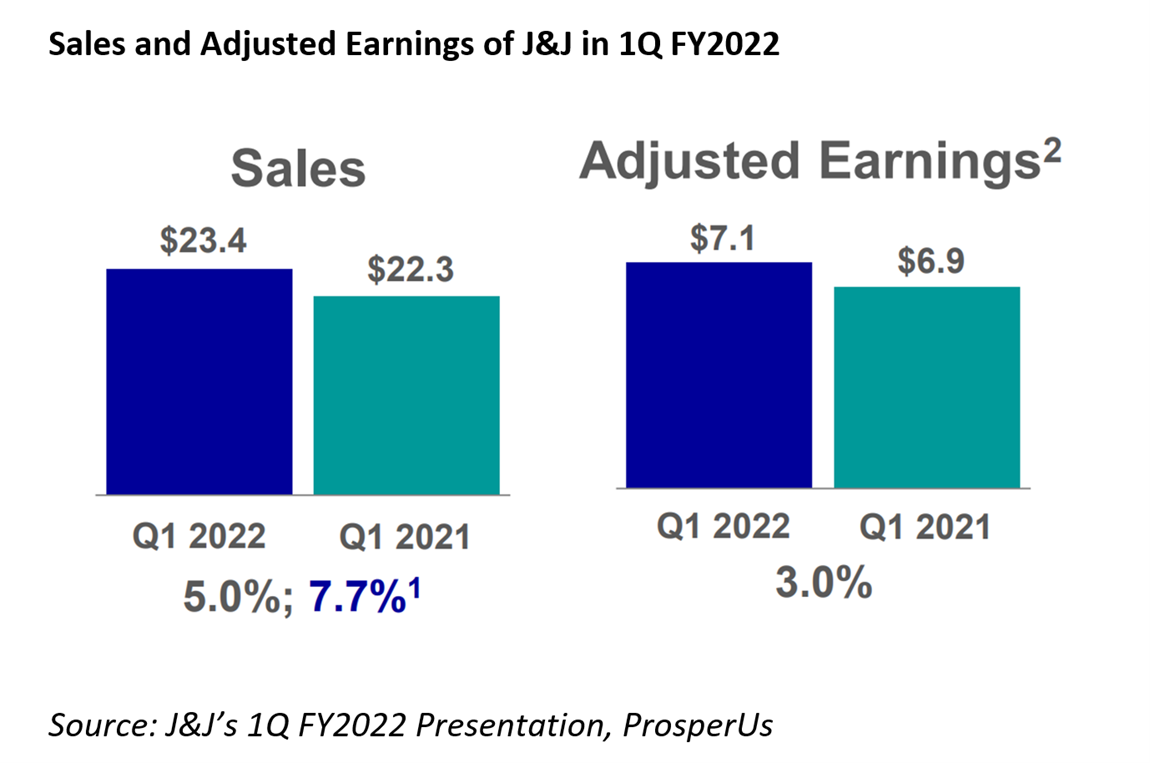

2. Resilient growth across all segments

While inflationary pressure will hurt earnings in the near term, I’m encouraged by the resilient growth of J&J.

Sales increased by 5.0% to US$23.4 billion in the 1Q FY2022 from US$22.3 billion in 1Q FY2021.

In line with higher sales, J&J’s adjusted earnings was up by 3.0% to US$7.1 billion as compared to US$6.9 billion during the same period last year.

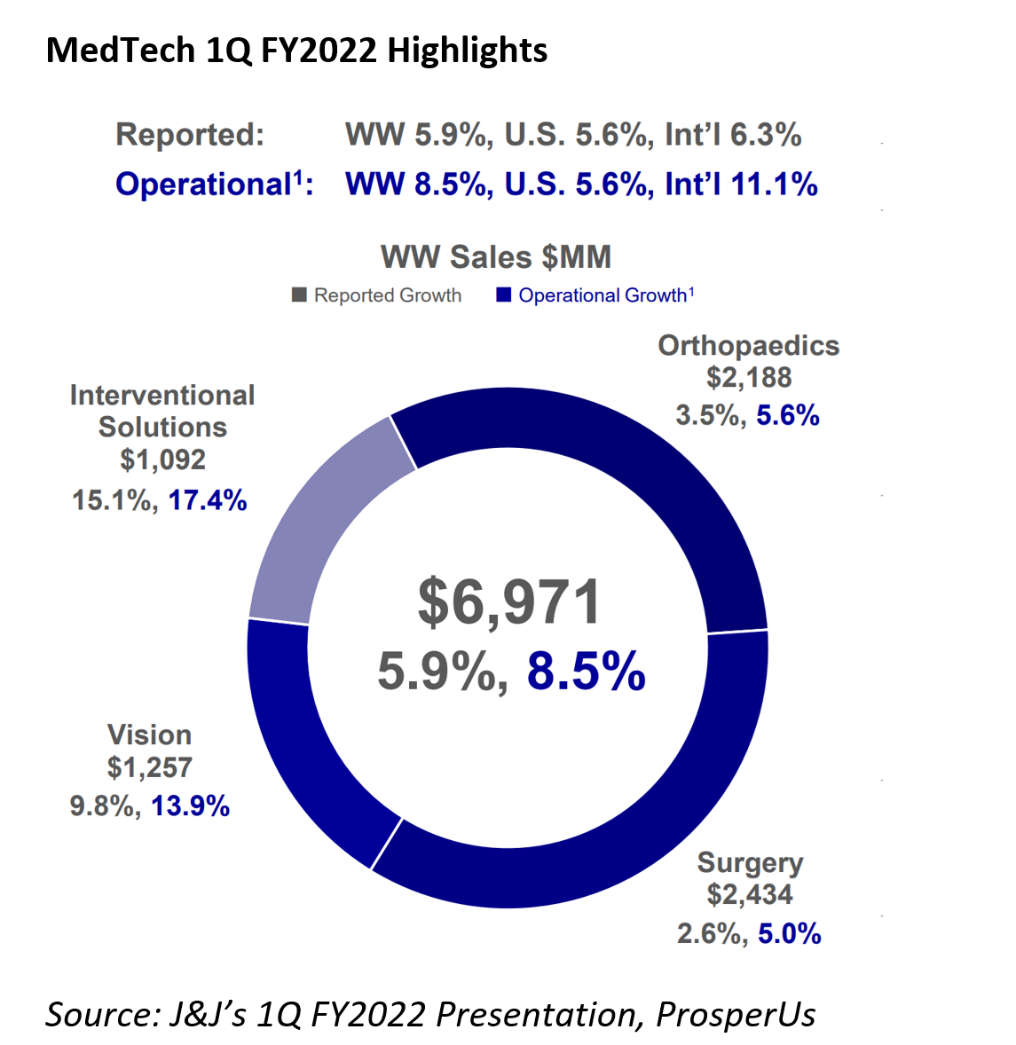

3. Strong growth in MedTech

The MedTech business segment posted 5.9% growth in the 1Q FY2022 (see below).

According to J&J, that growth was driven by a COVID-19 market recovery, market expansion and innovation undertaken by the team to enhance its global leadership.

Strong growth is seen in the hips and knees sub-segment, an indication of a rebound in procedures as economies reopen.

Growth potential ahead remains strong as MedTech will continue to build on the 20 major new product launches seen in 2021.

MedTech has announced the addition of two new innovations to its ATTUNE portfolio – the ATTUNE cementless fixed bearing knee with AFFIXIUM 3DP Technology and the ATTUNE medial stabilised knee system.

4. Above-market performance of pharma driven by volume

The pharmacy business is the largest segment for J&J. Growth continues to outperform driven by volume. This helped to offset inflationary pressure.

Pharmaceutical segment sales rose 6.3% year-on-year to $12.9 billion, reflecting 9.3% operational growth and 3% negative currency impact.

Excluding the impact of all acquisitions and divestitures, on an operational basis, worldwide sales rose 9.3%.

Among some of the key areas that have driven growth are oncology, immunology and neuroscience.

It is also worth noting that J&J has suspended its Vaccine guidance.

J&J’s single-dose COVID-19 vaccine generated sales of US$457 million in the 1Q FY2022 as compared with US$1.62 billion in the 4Q FY2021.

The impact on its earnings, however, will be minimal as J&J is selling its vaccine on a not-for-profit basis.

5. Dividend Increases

J&J also increase its dividend during the quarter to US$1.13 per share from US$1.06 per share. This will add up to annual dividend of US$4.52 per share as compared with the previous rate of US$4.24 per share.

It has a strong track record of rewarding its shareholders with dividend increases as seen by the 60 consecutive years of dividend hikes.

At its current share price level, J&J shares offer investors a dividend yield of around 2.4%.

Strong underlying growth but near-term risks unavoidable

The focus on the MedTech and Pharmaceutical businesses, with the spinoff of its Consumer Health business, will help J&J to accelerate its growth trajectory.

The separation into two companies – the new J&J with MedTech and pharmaceutical business and the new Consumer Health company, will help to streamline technology and processes.

The management has also continued to deliver resilient growth despite the challenging macro environment and generate meaningful free cash flow to allocate US$3.5 billion to research & development (R&D) investment (+8.9% versus prior year).

Despite the positive underlying growth, I believe persistent inflation and the recent resurgence of COVID-19 in China (and the lockdown imposed) will have an impact on J&J’s earnings in the near term.

Long-term investors who aim to protect themselves from the current volatile market will find safety in J&J stock.

However, short-term traders might find it harder to time the entry into J&J given the upcoming spinoff exercise and potentially weaker earnings growth in the near term.

Disclaimer: ProsperUs Investment Coach Billy Toh doesn’t own shares of any companies mentioned.