Streaming giant Netflix Inc (NASDAQ: NFLX) has seen its share price decline by more than 60% in 2022.

This has come amid concerns over its ongoing loss of subscribers, intensifying competition in the streaming video market, and slowing growth.

While the company has benefitted from the pandemic (where millions of us stayed indoors), the reopening of the economy has put Netflix at a strategic disadvantage for eyeballs.

So there was focus on Netflix after it reported its latest earnings, following its poor first-quarter report.

Here’s a look for investors at the company’s Q2 FY2022 earnings report. Has the selloff in the shares created a buying opportunity for investors?

1. Another quarter of declining subscribers

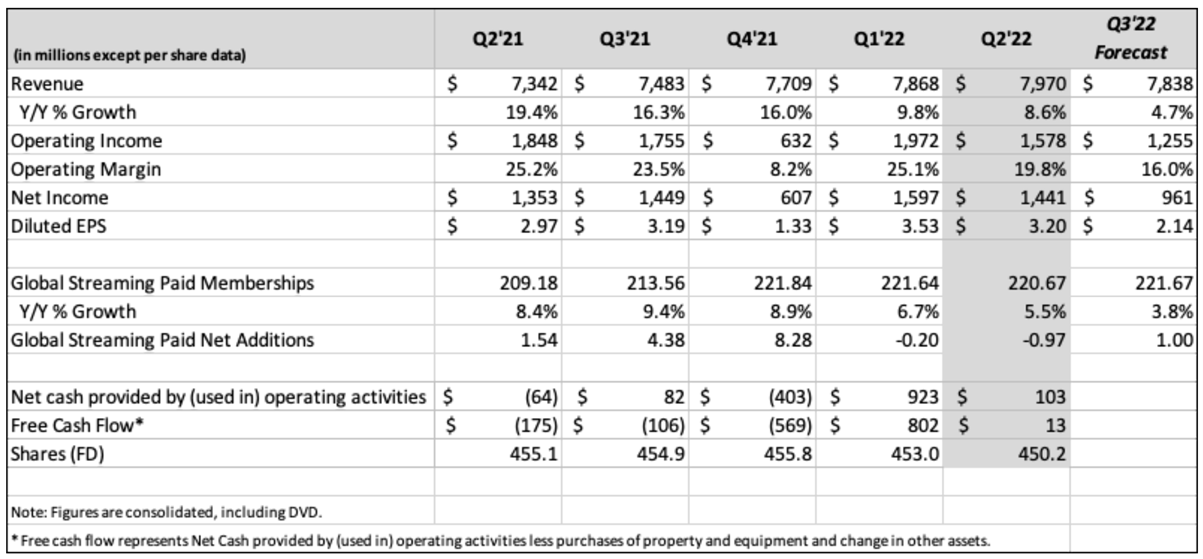

Netflix reported a second consecutive quarter of declining subscribers as the streaming giant lost 970,000 subscribers in Q2 FY2022.

This was worse than 200,000-subscriber loss in Q1 FY2022 but better than the 2 million subscribers that the management projected.

While it is difficult to point to a single factor that drove the better-than-expected number of paid subscribers, management has talked about the strong debut of season 4 of Stranger Things.

Revenue during the quarter was up 9% year-on-year to US$7.97 billion but it was another slowdown from the 9.8% growth recorded in the previous quarter.

Source: Netflix’s Letters to Shareholders for Q2 FY2022 Earnings

2. Better third quarter guidance

One of the positive takeaways from the earnings results was the better guidance offered by the management.

They expect to see an increase of 1 million paid subscribers, a reversal from the decline we saw over the last two quarters.

This will put the company’s paid subscribers back at the Q1 FY2022 level.

It could also be the silver lining that has led to a recovery in its share price recently.

Personally, I think paid subscribers in Netflix should remain relatively stable given its superior content as compared to its competitors.

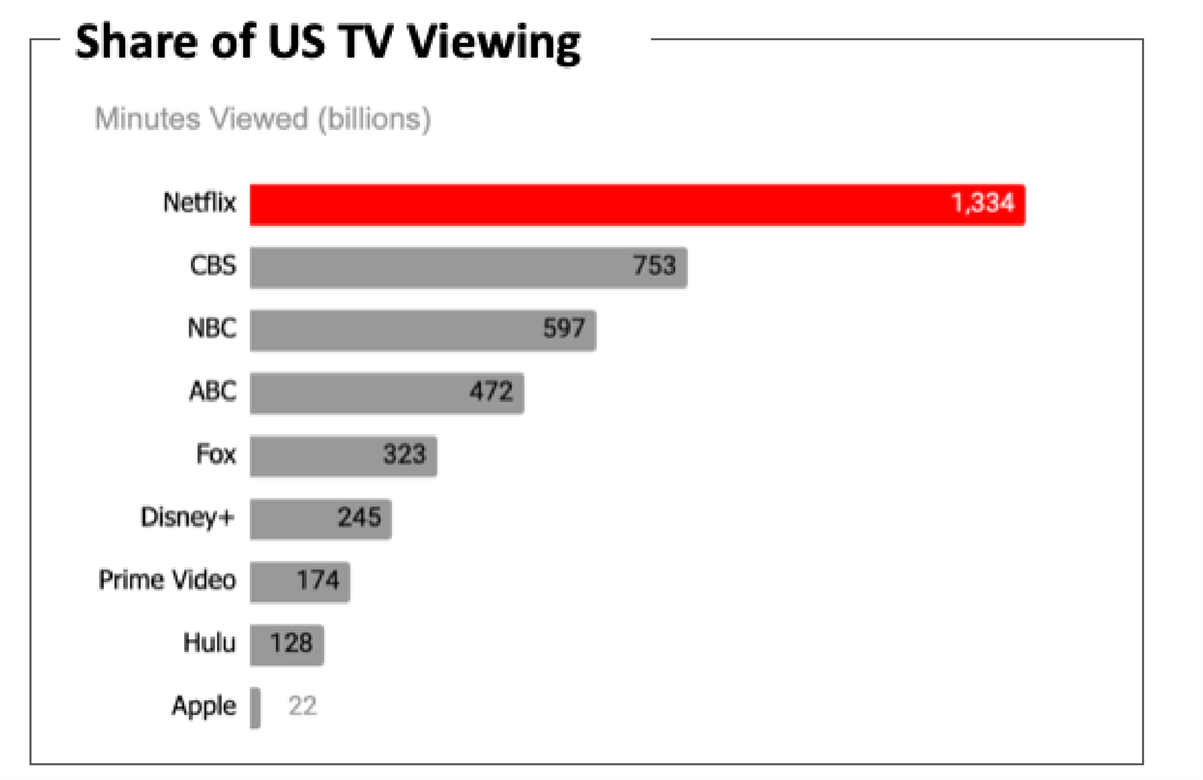

To put it into perspective, Netflix drew more TV viewing time than any other service during the 2021-22 TV season in the US.

Source: Nielsen, Netflix’s Letter to Shareholders for Q2 FY2022 Earnings

Source: Nielsen, Netflix’s Letter to Shareholders for Q2 FY2022 Earnings

Looking at the chart above, the minutes viewed on Netflix is at 1,334 billion minutes, almost matching the combined total of the two most watched broadcast networks in the US.

This is despite the US being one of the most competitive markets in the world.

When we compare it with Netflix’s closest competition, Disney+, it is obvious that Netflix has a far better reach and engagement in the streaming space with more than five times the viewing minutes.

3. Netflix looks to maintain positive, sustainable free cash flow

I think Netflix has finally reached a level that allows the streaming giant to generate free cash flow while investing in good quality content.

As a content company, I believe Netflix has done an outstanding job of investing in original, exciting content.

Below are some of the top original shows that have been produced by Netflix.

Source: ProsperUs, Netflix

In Q2 FY2022, net cash generated by operating activities was US$103 million as compared to -US$64 million in Q2 FY2021.

Free cash flow generated in the quarter totalled US$13 million as compared to -US$175 million in Q2 FY2021.

During the earnings call, Chief Financial Officer of Netflix, Spencer Adam Neumann, said:

“But as you say, we’re guiding to $1 billion, plus or minus a few hundred million of positive free cash flow in ‘22. We think that will continue to grow substantially next year.

It’s a combination of what we said before. We’re through that kind of cash-intensive transition of our business. We’re also operating about kind of roughly similar levels of cash content spend next year as this year.

In fact, as we said, we pulled forward a little bit of cash spend into ’21, ’22. So those things are kind of working in our favor as we continue to scale the business.”

4. Ad Partnership with Microsoft

Netflix will also introduce a new, lower-priced ad-supported tier to complement its existing plans, which will remain ad-free.

The company has recently announced Microsoft Corporation (NASDAQ: MSFT) as its technology and sales partner, and the lower priced advertising-supported offering is targeted to launch in early 2023.

It is probably still too early to gauge the impact of this new initiative but with a strong dominance in viewership, the advertisement business could be a game changer for the streaming giant.

5. Paid sharing to better monetise viewing

Another initiative that Netflix is looking to better monetise is paid sharing.

This will help the company to monetise more than 100 million households that are currently using Netflix but not paying for it.

While Netflix is still in its early stage of monetising this significant number of households, the company will start testing it out in Latin America and could go live in some areas as soon as 2023.

To put into context, Netflix will roll out two models. The first model will require users to pay a little bit more to add a member of the household and share with those additional members.

The second model will be to pay a little bit more to add an additional home for account sharing purposes.

Netflix’s fundamentals improved despite slowing growth

Personally, I like how the Q2 FY2022 earnings report for Netflix turned out. However, it is worth taking note of the company’s huge debt level.

As at the end of Q2 FY2022, gross debt stood at US$14.3 billion. With cash of US$5.8 billion, this means that Netflix has a net debt of US$8.5 billion – or 1.3 times its earnings before interest tax, depreciation and amortisation (EBITDA).

The global headwinds also remain with inflationary pressures and fear of a recession in the US.

Netflix will also need to prove that it can execute its new initiatives and return to a growth trajectory in the near term.

The downside risks remain but given the sharp decline in its share price, I think Netflix at a forward price-to-earnings ratio of 21.5 times currently, is very attractive.

That’s cheap when you compare it to when its five-year average of 83.8 times.

Disclaimer: ProsperUs Investment Coach Billy Toh doesn’t own shares of any companies mentioned.