With chatter about social media stocks among investors tending to focus on Facebook Inc (NASDAQ: FB), Instagram and Bytedance-owned Tik-Tok, you’d think there weren’t many other options to invest in.

That would be a mistake to assume. That’s because there are a whole host of other social media platforms, which are carving out specific niches that differentiate themselves from the giants.

Two such companies are Twitter Inc (NYSE: TWTR) and Snap Inc (NYSE: SNAP), both which own compelling and engaging platforms in Twitter and Snapchat, respectively.

Both Twitter and Snap stock have been volatile in recent weeks as earnings releases saw some selling pressure. The sell-off was particularly painful for Snap, which saw its shares crash 25% on the back of several factors.

But are both these businesses still solid social media investments for the long term? And more importantly, which is the better buy for investors now; Twitter or Snap?

Revenue growth

For growth stocks that rely on investors putting money behind their future cash flows, these two rising social media companies and their revenue growth rates is something that we need to watch.

In this regard, we’ll have to look at the compound annual growth rate of revenue over the past four years since Snap was only listed in early 2017.

In Q3 2017, Twitter posted revenue of US$590 million. By the latest third quarter in 2021, that figure had grown to US$1.28 billion, giving Twitter a four-year revenue CAGR of 21.4%.

So, how about Snap? The Gen Z-friendly platform saw revenue of US$208 million in the third quarter of 2017. In its most recent third quarter of 2021, Snap posted revenue of US$1.07 billion.

Winner: Snap

ARPU growth

When we look at social media firms, one of the biggest metrics is how well the company is able to monetise its users.

To measure this, we need to look at the average revenue per user (ARPU), which is basically total revenue divided by daily active users (DAUs).

Crucially, are these companies growing overall ARPU at a reasonable clip over time? That means there’s a pattern of consistent execution on the monetisation front.

For Twitter, since it only started breaking out its monetisable DAU (mDAU) as of 2019, in the third quarter of that year it saw an ARPU of US$5.68.

By the third quarter of this year, it posted an ARPU of US$6.08, meaning it had a two-year CAGR in ARPU of 3.5%.

Meanwhile, Snap saw ARPU of US$2.12 during the third quarter of 2019. By the third quarter of this year, that figure hit US$3.49, giving the firm a two-year ARPU CAGR of 28.3%.

Winner: Snap

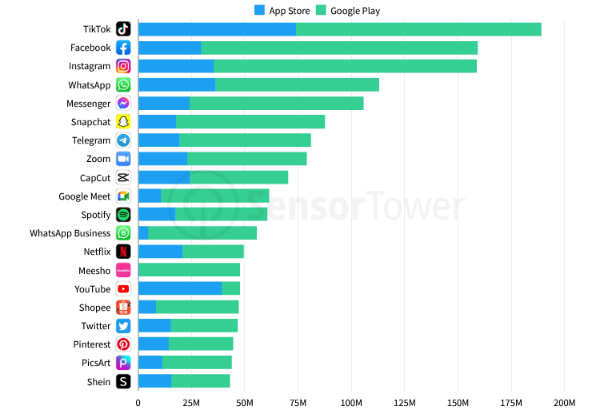

App downloads

One of the more under-the-radar ways to get info is to dig into data points that not everyone is thinking about.

This is sometimes referred to as “scuttlebutt” after the term Phil Fisher used in his book Common Stocks and Uncommon Profits.

By looking at unorthodox sources of information, you can glean interesting insights into companies. One such source for social media companies is to look at app downloads in the latest quarter.

While not all of them will be converted to DAUs that engage with the platform regularly, it’s a good indication of how popular a platform is or how it’s trending.

As readers can see below, Snap had over 80 million app downloads globally in the three months ending 30 September 2021. That compares to Twitter’s sub-50 million number.

Source: Sensor Tower Q3 2021 Data Digest

Converting these app downloads into users that contribute to the top and bottom lines will be key but on this front, Snap already has an advantage by being able to tap a larger base.

Winner: Snap

Executing better

While Twitter has started to better monetise its platform in recent years, it’s still some way behind Snap and its popularity in terms of an overall platform.

For example, in the third quarter Snap had an average of 306 million DAUs whereas Twitter only had 211 million mDAUs.

For long-term investors, it seems that Snap’s focus and execution of its strategy has been more successful than Twitter.

And while its shares recently took a hit, the company is still one of the brightest up-and-coming social media stocks to own over the next five to 10 years.

Disclaimer: ProsperUs Head of Content & Investment Lead Tim Phillips doesn’t own shares of any companies mentioned.