Wayfair Inc (NYSE: W), the online home-goods and furniture retailer, saw its shares soar 7.2% on positive earnings. Should investors buy into its growth?

Tim’s Take:

A 12-bagger since March this year. That’s what Wayfair shareholders would be sitting on had they picked them up the stock at around US$22 during the massive March sell-off.

Today? They’re trading at around US$275 after yesterday’s 7% pop. Granted, you’d have to be have been a brave buyer at those levels after the stock had fallen around 80% between the start of 2020 and its March low.

However, the reasoning for the extraordinary rebound is clear. Wayfair offers consumers a convenient way to buy home furniture and other home goods; by doing it online.

More so than generalists like Amazon Inc (NASDAQ: AMZN), Walmart Inc (NYSE: WMT) or Target Corporation (NYSE: TGT), specialty online retailers such as Wayfair have thrived in the Covid-19 economy.

What’s more, with young people starting to move to the suburbs, and with the housing market in the US holding up well, Wayfair is ideally-positioned to take advantage of this structural shift.

Solid results and differentiated offering

In fact, Wayfair’s latest earnings attest to the strength of its offerings. The company posted robust revenue growth of 66.5% year-on-year in the third quarter to US$3.8 billion.

Meanwhile its gross margin for the third quarter was just shy of 30%, extraordinary versus a 2019 number of 23.6%.

Wayfair also has a presence in international markets, namely in Europe. Although it only makes up about 17% of Wayfair’s overall revenue, its growing fast.

One of the big reasons for Wayfair’s success has been its diverse product offerings with five separate labels that cut across various price points.

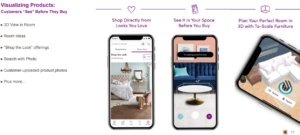

What’s more, the company has also been able to differentiate itself by addressing customer needs, such as utilising technology to help users plan and picture layouts in their home (see below).

Source: Wayfair Q3 2020 earnings presentation

For investors who are taking a long-term approach, Wayfair could prove to be an interesting stock that plays into the long-term trends of younger consumers purchasing home goods online.

With over 28.8 million active customers and an online home category that is growing at approximately 15% per year in the US, Wayfair is well-positioned to keep winning in the online home furnishings sector.

Disclaimer: ProsperUs Head of Content Tim Phillips doesn’t own shares of any companies mentioned.