Global Markets Week Ahead: US Corporate Earnings and Key Data Take Center Stage

November 25, 2024

- US corporate earnings and inflation data will drive global sentiment, influencing Southeast Asia’s key economies.

- China’s industrial profits and PMI readings will be pivotal for regional markets reliant on trade with China.

- Southeast Asia’s economies – Malaysia, Indonesia, Singapore, and Thailand – face mixed prospects amid inflation, production, and trade shifts.

As the final stretch of 2024 approaches, this week will spotlight the interplay of US corporate earnings and pivotal economic data, offering critical insights for investors navigating uncertain markets. With Thanksgiving reducing trading days in the US, the focus will be on how these developments shape market sentiment. Meanwhile, China’s recovery trajectory and European economic conditions will also hold global investors’ attention, adding a regional dimension to market dynamics.

United States: Corporate Earnings and Data Take the Spotlight

This week, US corporate earnings are set to dominate headlines, with high-profile tech and consumer names leading the charge. Companies like Zoom Video Communications, Inc. (NASDAQ: ZM), Dell Technologies Inc. (NYSE: DELL), Analog Devices, Inc. (NASDAQ: ADI) and CrowdStrike Holdings, Inc. (NASDAQ: CRWD) will provide key updates on their performance and outlooks.

Tech and semiconductor firms remain in focus, with investors seeking clarity on enterprise spending trends, the impact of inventory adjustments, and demand for AI-related technologies. For instance, Analog Devices is expected to offer insights into global chip demand, particularly in the auto and industrial sectors, while CrowdStrike could influence cybersecurity sentiment with updates on customer adoption and its roadmap after recent technical issues.

Consumer-facing companies like Bath & Body Works, Inc. (NYSE: BBWI) and Patterson Companies, Inc. (NASDAQ: PDCO) will shed light on discretionary spending trends and healthcare dynamics as the holiday shopping season gets underway. These earnings reports could set the tone for broader sectors, influencing market sentiment beyond the immediate results.

On the economic front, a slew of significant data releases will complement corporate earnings, painting a broader picture of the US economy. Consumer Confidence will offer a snapshot of household sentiment as consumers prepare for the holiday season, while New Home Sales and the S&P Case-Shiller Home Price Index will shed light on the housing market’s health amid rising interest rates. Durable Goods Orders and the Core PCE Price Index, the Federal Reserve’s preferred inflation measure, will provide critical insights into economic resilience and inflationary pressures. Additionally, Initial Jobless Claims will be closely watched for indications of labor market stability, which remains a key driver of consumer spending. Speaking of spending, data on Personal Income and Spending will reveal how households are managing rising costs and whether consumption is holding steady as a growth pillar. Adding to the intrigue, the FOMC minutes from the November meeting will offer a deeper understanding of the Federal Reserve’s policy stance, particularly as markets remain divided on the likelihood of further rate hikes. Together, these releases will provide a comprehensive view of the economic landscape as investors navigate a critical juncture.

China and Hong Kong: Recovery in Focus

China’s economic recovery remains a central theme, with key data releases, including industrial profits and PMI readings, on the docket. Investors will closely watch whether Beijing’s stimulus efforts are translating into tangible growth in manufacturing and services. Improved PMI figures could boost confidence and support regional markets, including Hong Kong, where trade data will provide additional context for economic conditions.

Southeast Asia: MIST Markets Look for Direction

The MIST economies—Malaysia, Indonesia, Singapore, and Thailand—will look to local data and external factors for cues:

Source: TradingEconomics, Bloomberg

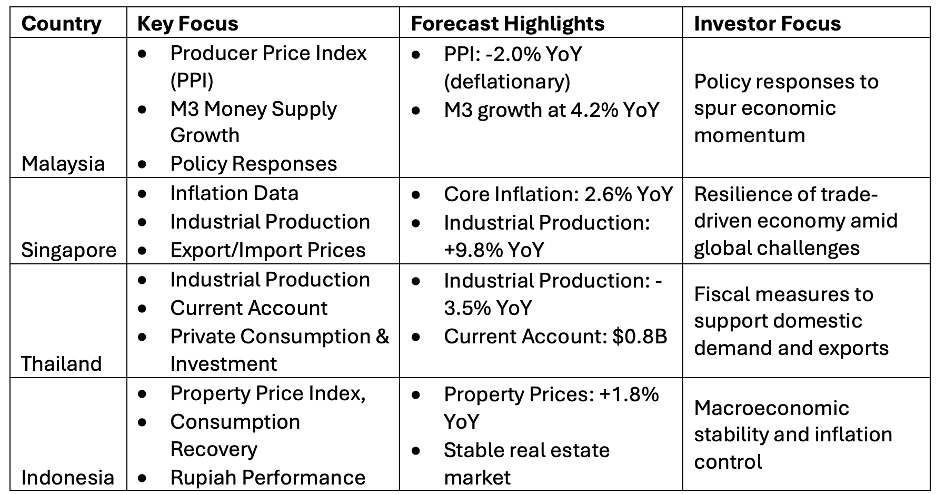

- Malaysia: In Malaysia, October’s Producer Price Index (PPI), forecasted at -2.0% YoY, could highlight ongoing deflationary trends in input costs. This could provide relief for manufacturers but also point to sluggish demand. Investors will look for any improvements in M3 money supply growth for October, expected to remain at 4.2% YoY, to assess liquidity conditions in the economy. With subdued data, attention will turn to fiscal or monetary policy responses to revive momentum.

- Singapore: Singapore’s economic calendar is headlined by October inflation data, where core inflation is expected to ease slightly to 2.6% YoY, signaling a gradual normalization of price pressures. October’s Industrial Production is projected to rise significantly (9.8% YoY), driven by a rebound in electronics and pharmaceuticals, despite flat growth MoM. Additionally, export and import prices for October are forecast to decline (-9.4% YoY and -7.9% YoY, respectively), reflecting the impact of softening global demand. The data will help investors gauge the resilience of Singapore’s trade-driven economy amid external challenges.

- Thailand: Thailand’s economic releases will paint a picture of ongoing domestic struggles. October’s Industrial Production is forecast to contract further, at -3.5% YoY, as weak export demand weighs on manufacturing. The Current Accountbalance for October is expected to improve marginally to $0.8 billion, providing some support to the baht. However, Private Consumption and Investment data, with forecasts pointing to subdued growth, reflect the fragility of domestic demand. September’s stellar Retail Sales growth (31.36% YoY) could taper off as base effects wane, leaving markets to focus on whether fiscal measures can drive sustained economic activity.

- Indonesia: Indonesia’s focus will be on the Q3 Property Price Index, forecasted to grow modestly at 1.8% YoY, indicating a stable but subdued real estate market. While the property sector shows resilience, investors will look for signs of broader recovery in consumption and investment activity. The rupiah’s performance and its influence on inflationary pressures will also remain in focus, with markets keen to see whether Indonesia’s macroeconomic stability can weather global headwinds, particularly as external demand softens.

Together, these forecasts offer a mixed outlook for the MIST economies, with domestic and external factors continuing to weigh heavily on their recovery trajectories. Investors will look for policy clarity and sector-specific resilience to navigate the week.

Europe: Economic Sentiment and Inflation Data

In Europe, sentiment surveys and preliminary inflation data will dominate the agenda. Germany’s IFO Business Climate Index and CPI figures will provide a pulse check on the eurozone’s largest economy, while ECB commentary will keep investors alert to potential policy shifts. The region remains sensitive to global growth concerns, making these data points particularly significant.

Call to Action: Focus on Fundamentals Amid Crosscurrents

As the week unfolds, investors should focus on key drivers shaping the markets. US corporate earnings from tech and consumer companies will provide valuable insights into trends in AI, chip demand, and discretionary spending, highlighting broader economic resilience. These reports, coupled with crucial inflation data and the FOMC minutes, will help gauge the Federal Reserve’s policy trajectory, with higher-than-expected inflation potentially reigniting fears of further tightening. Meanwhile, China’s industrial and PMI data will be pivotal in assessing the effectiveness of its stimulus measures, with positive surprises likely to lift sentiment across Asia, especially in Hong Kong and Southeast Asia. Amid thinner trading volumes during the US Thanksgiving week, heightened volatility offers an opportunity for investors to reassess portfolios, focusing on quality stocks with strong fundamentals to navigate these dynamic conditions.

Disclaimer: ProsperUs Head of Content & Investment Lead Billy Toh doesn’t own shares of any companies mentioned.

Billy Toh

Billy is deeply committed to making investment accessible and understandable to everyone, a principle that drives his engagement with the capital markets and his long-term investment strategies. He is currently the Head of Content & Investment Lead for Prosperus and a SGX Academy Trainer. His extensive experience spans roles as an economist at RHB Investment Bank, focusing on the Thailand and Philippines markets, and as a financial journalist at The Edge Malaysia. Additionally, his background includes valuable time spent in an asset management firm. Outside of finance, Billy enjoys meaningful conversations over coffee, keeps fit as a fitness enthusiast, and has a keen interest in technology.