Markets, geopolitics and the global economy are all dominated by volatile events, which leads to a lot of uncertainty and instability.

Year-to-date (YTD), the S&P 500 Index is down by 7.3% while the tech-heavy Nasdaq Composite Index is down by more than10%.

For investors who are looking for peace of mind and a good night’s sleep amid the volatility, Lockheed Martin Corp (NYSE: LMT) is a good choice for investors in the long term.

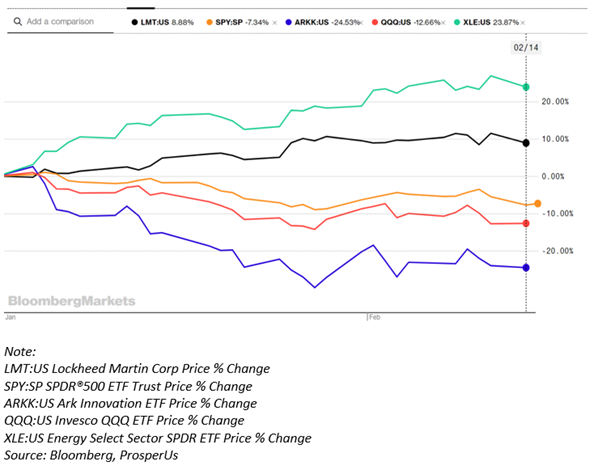

At the moment, Lockheed’s share price has gained by 8.9% YTD (see below).

While it is not as impressive as the Energy Select Sector SPDR Fund (NYSE: XLE), which has increased by 23.9% YTD, it is one of the few value stocks that can continue to provide stability in volatile times.

Lockheed Martin offers a stable return

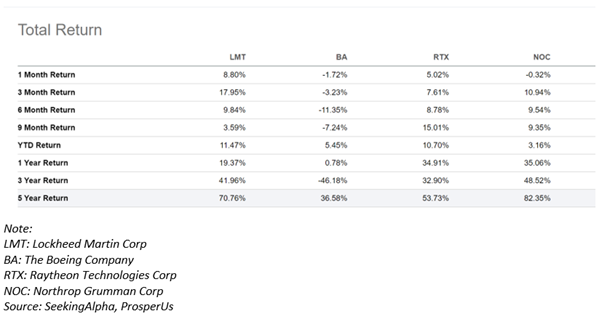

Lockheed’s share price performance has also performed consistently over the long term. The five-year total return of the company’s stock is 70.8%, which translates into an annual total return of 11.3%.

While there has been a dry spell in recent times, mainly due to supply chain issues, things have improved significantly as we learn to live with the pandemic.

Resilient amid supply chain crunch

Lockheed is not exposed to commercial aerospace demand but it is exposed to the supply chain issue as smaller players, with both commercial and defense exposure, were affected by the pandemic.

The risks of bankrupt suppliers rose at that time, which affects the defense supply chain.

Nonetheless, despite the recovery in its share price, its current price of US$386.97 is still about 12% below its peak in February 2020.

The current weakness in its share price mostly has to do with the company’s failed acquisition of Aerojet Rocketdyne Holdings Inc (NYSE: AJRD) after the US Federal Trade Commission tried to block the deal.

Leading defense contractor

The company has been around since 1995 when Lockheed and Martin Marietta merged, while the Lockheed Corporation was founded back in 1920.

It is also the world’s largest defense contractor and has dominated the Western market for high-end fighter aircraft since it was awarded the F-35 programme back in 2001.

Strong free cash flow

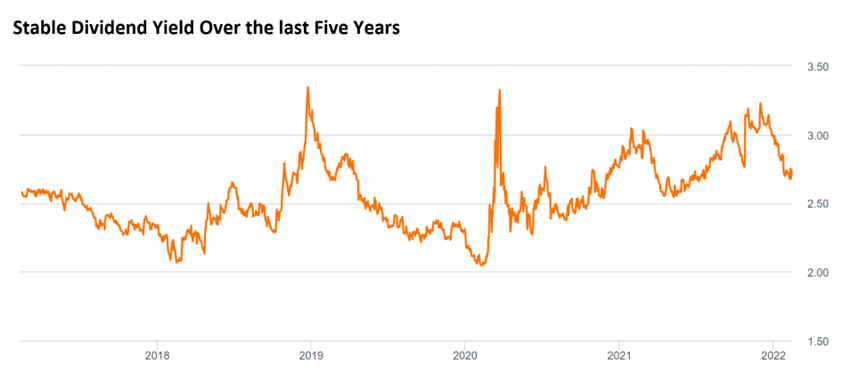

The forward dividend yield for Lockheed is 2.8%, which represents 38.9% payout ratio for the defense company.

Over the last five years, the company’s dividend yield has remained above 2.0% with an average yield of around 2.6% (see below).

Source: SeekingAlpha, ProsperUs

Source: SeekingAlpha, ProsperUs

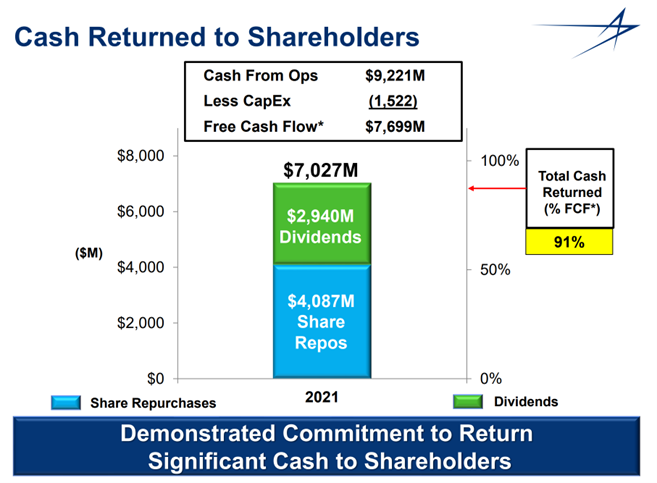

One important thing to take note is Lockheed’s ability to generate free cash flow. This allows the company to spend money on dividends and share buybacks.

In 2021, Lockheed generated US$7.7 billion of free cash flow and returned a total of US$7.0 billion to shareholders with US$2.9 billion in dividends and another US$4.1 billion in share buybacks.

Source: Lockheed Martin’s presentation slides(as of January 25, 2022)

Source: Lockheed Martin’s presentation slides(as of January 25, 2022)

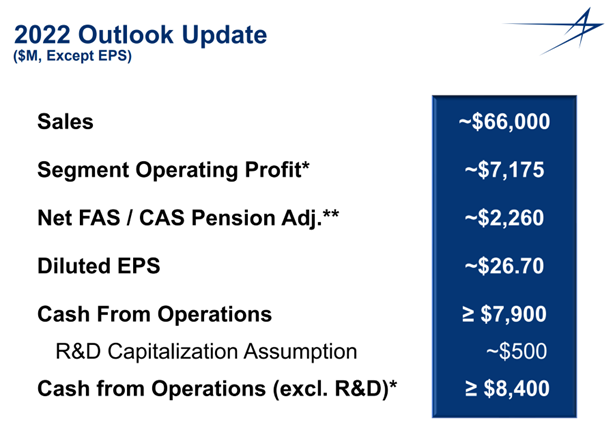

The outlook for 2022 also remains positive as Lockheed expects to generate more than US$8.4 billion in cash from operations. This is based on US$66 billion in sales and US$7.2 billion in operating profit.

Source: Lockheed Martin’s presentation slides (as of January 25, 2022)

Source: Lockheed Martin’s presentation slides (as of January 25, 2022)

Stable long-term growth

During the earnings call in January, CEO Jim Taiclet also shared Lockheed’s growth strategy, which anticipates sales to increase by 2% in 2023 with steady growth through 2026.

The four primary areas that underpin the long-term growth forecasts are programmes of record, classified activities, hypersonics and new business awards.

Lockheed has a fantastic business model although the exposure and reliance on government funding is its key risk.

Having said that, I believe that with the rise of China in recent years, we will see an expansion of investment for the defense budget of the US, which will benefit the company.

R&D focus

Focus on research & development (R&D) will also help to improve margins as large defense contractors generate better margins on R&D in advanced new weapons system compared to selling military equipment.

Other downside risks include the supply chain issues.

Given the current economic environment and volatile market, I believe it provides a good opportunity to buy into Lockheed that offers dividend growth, a high yield and an attractive valuation in a rather “expensive” market.

It is one of the few value stocks that will continue to provide stability if the current geopolitical tensions escalate further.

Disclaimer: ProsperUs Investment Coach Billy Toh doesn’t own shares of any companies mentioned.