It has been a busy week for investors as the “Big Tech” companies released their earnings for the first quarter of 2022.

The results have been mixed so far but one of the “Big Tech” companies that has managed to calm investors’ nerves is Facebook parent company, Meta Platforms Inc (NASDAQ: FB).

Shares of Meta surged by 17.6% to close at US$205.73 in a relief rally, after having lost nearly half of its value this year.

Net income for the social media giant came in at US$7.47 billion, or US$2.72 in earnings per share (EPS), during the first quarter of 2022 (Q1 FY2022). Analysts had an average EPS estimate of US$2.56.

Revenue in its latest quarter rose by 7% year-on-year to US$27.9 billion, falling short of analysts’ expectations.

However, the rebound in Meta’s share price reflects the sigh of relief among investors as concerns over Meta’s advertising revenue in its social media feeds are being put to rest.

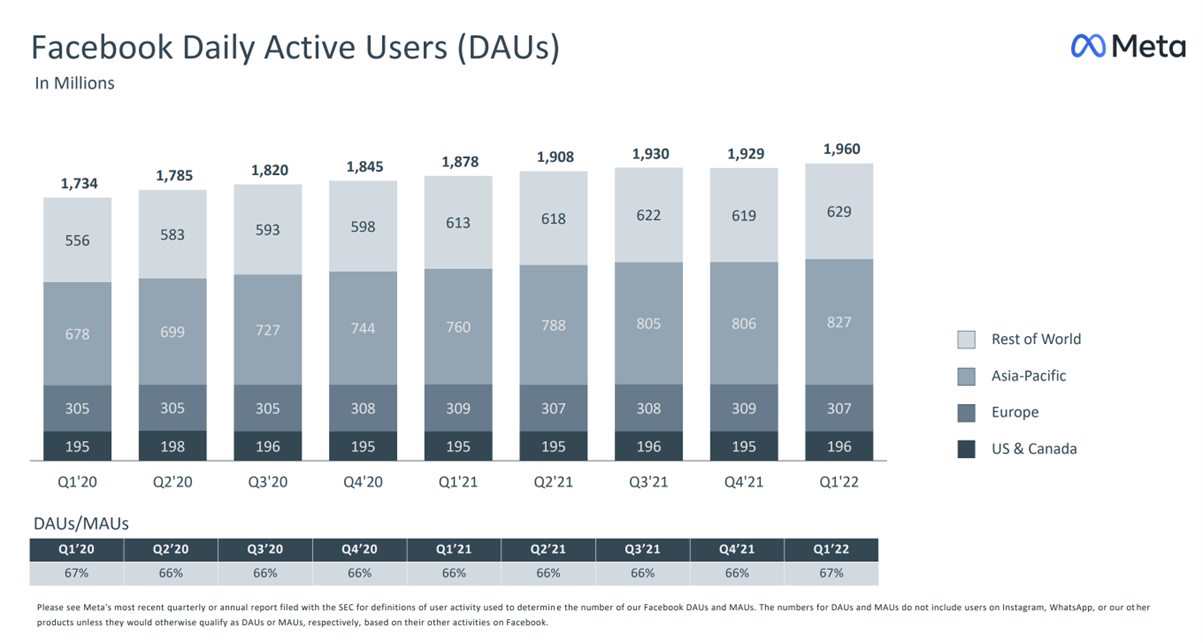

That’s mainly because Facebook added 31 million new daily active users (DAUs) during the quarter.

I recently wrote about three reasons why investors should buy Meta back in March when its share price was hovering at the US$187 level.

The latest earnings reemphasise my long-term view on Meta. Here’s what investors need to know.

Slowdown in growth not as bad as it looks

Analysts had expected Meta’s earnings to be worse given the headwinds in Europe, impact from Apple’s iOS privacy changes with its App Tracking Transparency (ATT) as well as competition from TikTok.

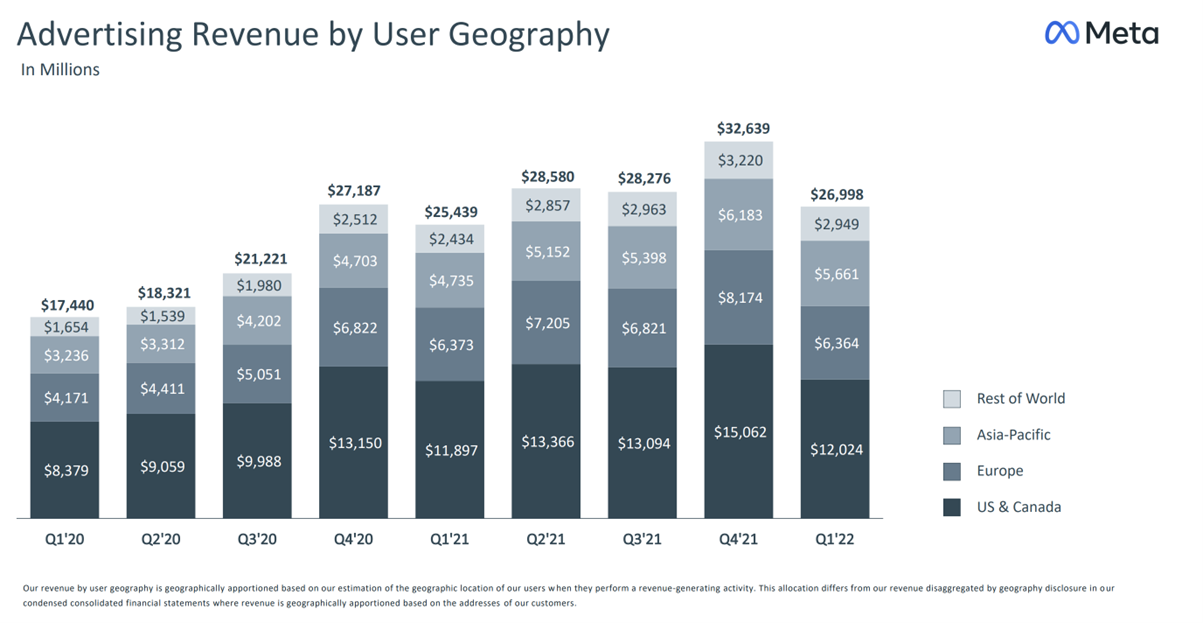

The slowdown in advertising revenue has a significant impact on Meta given its reliance on the advertising business. Almost 97% of Meta’s revenue is derived from the advertising business.

Advertising revenue grew by 6.1% to US$27.0 billion from the same period a year ago. While the growth was significantly lower than what we saw in FY2021, it reflects the current environment that Meta is operating in.

Slowdown in e-commerce, after its surge during the pandemic, the impact from Apple’s ATT, loss of revenue in Russia as well as the reduction in ad spending in Europe are among the factors that have led to a slowdown in advertising revenue.

As the post-COVID slowdown in e-commerce and the Russia-Ukraine war are one-off events, I believe Meta’s slowdown in advertising revenue will not be as bad as feared.

Source: Meta Earnings Presentation Q1 FY2022, ProsperUs

Source: Meta Earnings Presentation Q1 FY2022, ProsperUs

Facebook remains addictive

This is perhaps the main reason why we saw a surge in Meta’s share price as Facebook’s daily user growth has returned to a growth trajectory.

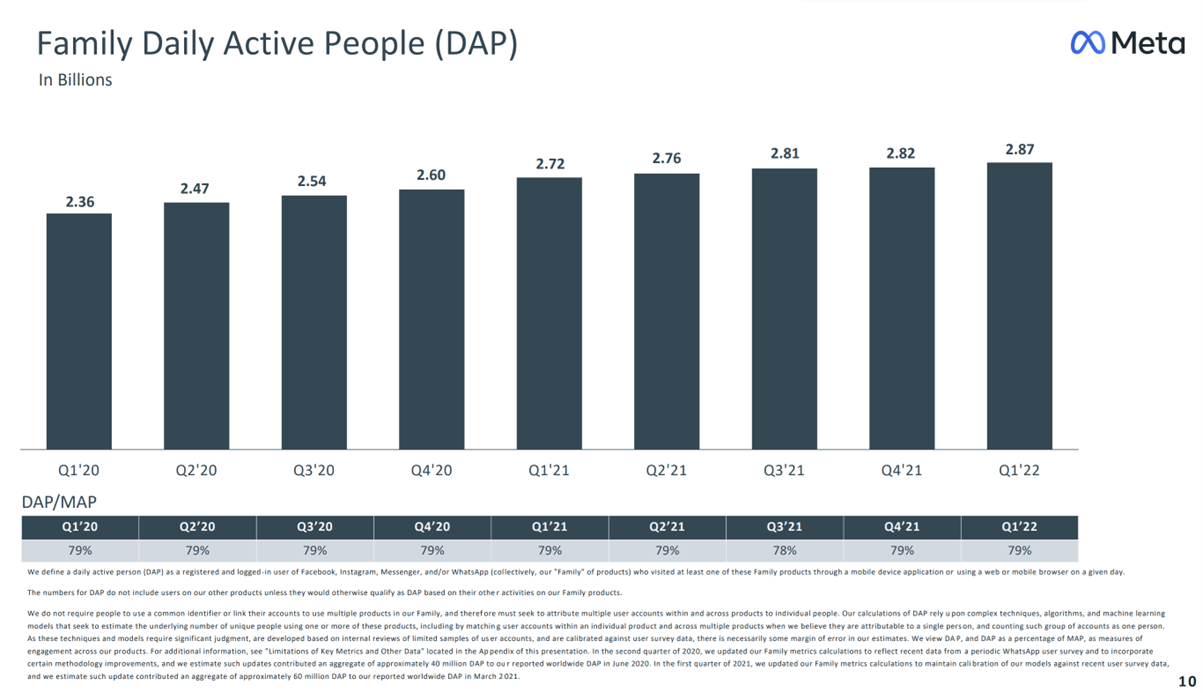

Meanwhile, Meta’s “family of apps” saw growth too. Family daily active people (DAP) was up to 2.87 billion during the Q1 FY2022, from 2.82 billion in Q4 FY2021.

The “family” includes users on Meta’s Facebook, Instagram, Messenger and WhatsApp platforms.

Source: Meta Earnings Presentation Q1 FY2022, ProsperUs

Source: Meta Earnings Presentation Q1 FY2022, ProsperUs

Meanwhile, Facebook daily active users (DAUs) increased to 1.96 billion in the current quarter as compared to 1.929 billion in Q4 FY2021.

Source: Meta Earnings Presentation Q1 FY2022, ProsperUs

Source: Meta Earnings Presentation Q1 FY2022, ProsperUs

Slowing expense to weather downside

This is not a big surprise to me but it helps to calm investors who are worried that Mark Zuckerberg would go on a spending spree on his Metaverse project.

During the earnings call presentation, Mark Zuckerberg, said this in regards to its investment into the Metaverse.

“However, based on the strong revenue growth we saw in 2021, we kicked off a number of multi-year projects to accelerate some of our longer-term investments, especially in our AI infrastructure, business platform, and Reality Labs.

These investments are going to be important for our success and growth over time, so I continue to believe that we should see them through. But with our current business growth levels, we’re now planning to slow the pace of some of our investments.”

As mentioned in my previous article, I believe the Metaverse is coming sooner than most of us would anticipate but given the head start that Meta has in comparison to its peers, the company can afford to slow the pace of its investment.

Growth slowdown is temporary

Long-term investors will find that the slowdown in growth for Meta could be temporary, similar to what we saw back in 2012 and 2018, when there was a transition from desktop to mobile feeds, and from a shift towards Stories instead of Feeds.

Given Meta’s focus on growing its Reels feature, a TikTok copycat, as a major part of its AI-based Discovery Engine vision, the company should eventually replicate some of the success it had in the past.

Meta has also adapted to Apple’s iOS privacy changes but downside risks remain as Apple iOS16 could introduce more changes for the social media giant.

Aside from that, rotation away from growth stocks to value stocks could also mean that valuations for technology stocks might be lower than what it was in the past.

Regulatory risks are also another growing concern that will keep investors awake.

On the whole, I think Meta offers an opportunity to long-term investors but don’t expect the volatility to end any time soon.

Disclaimer: ProsperUs Investment Coach Billy Toh doesn’t own shares of any companies mentioned.