With all eyes on NVIDIA Corporation (NASDAQ: NVDA)’s earnings, the company didn’t disappoint. In fact, they not only surpassed expectations but also delivered a strategic roadmap that underscores their strong positioning within the tech sector, capitalizing on the surge in demand for Artificial Intelligence (AI). Here are five key takeaways from NVIDIA’s financial performance in the Q1 2025.

1. Strong Performance and Optimistic Outlook

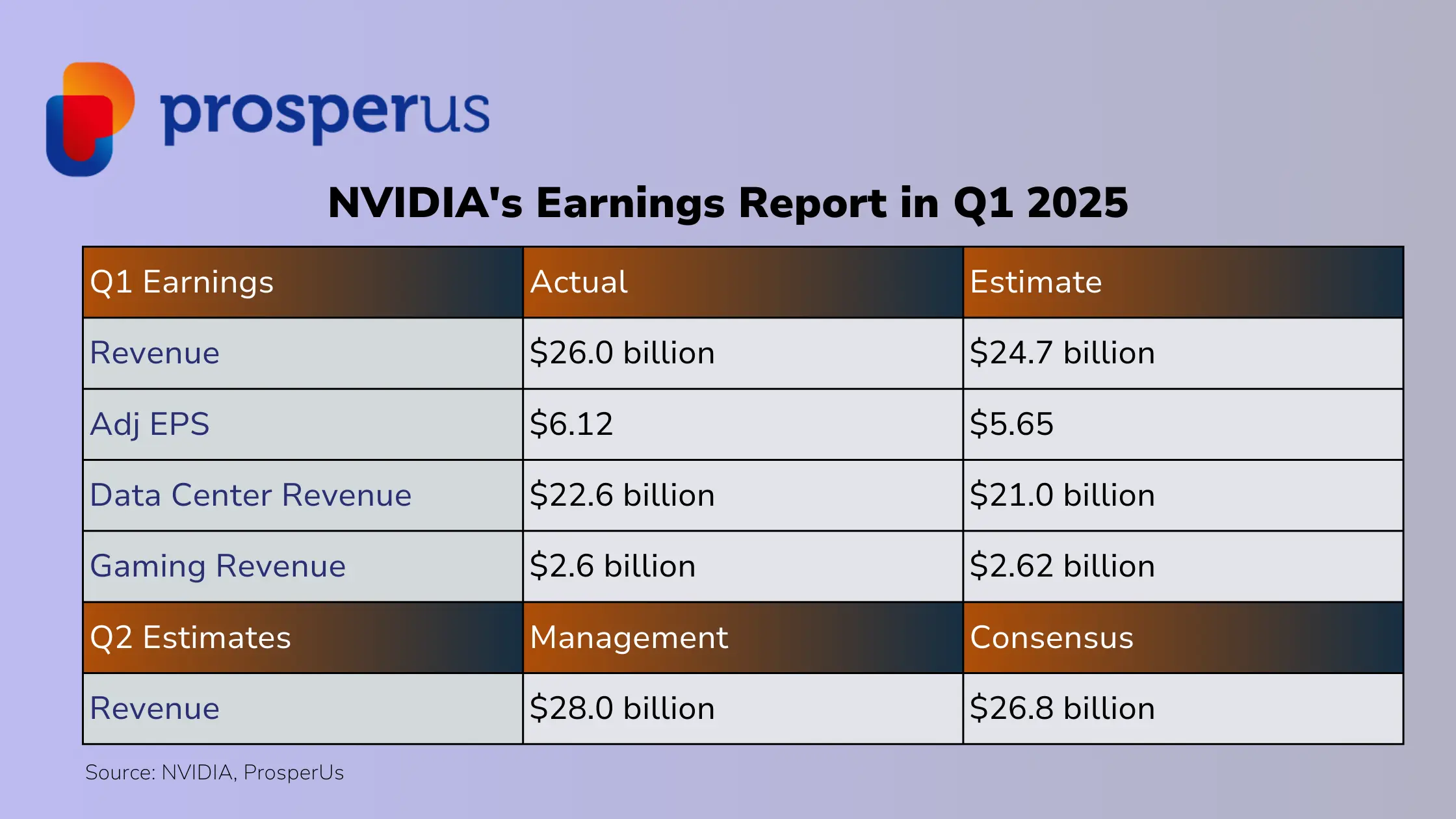

NVIDIA reported robust quarterly results with revenue and non-GAAP earnings per share (EPS) surpassing expectations. The company’s revenue stood at $26 billion, which was above the anticipated $24 billion, and non-GAAP EPS came in at $6.12, also exceeding estimates of $5.58. Looking ahead, NVIDIA anticipates a continued strong performance, with management expecting revenue for the upcoming quarter to be $28 billion, higher than the consensus estimates of $26.6 billion.

2. Continued Demand in Data Centers Driving Growth

Data Center revenue, a crucial segment for NVIDIA, showed significant growth, rising to $22.6 billion—a 23% increase quarter-over-quarter (qoq) and a staggering 427% year-over-year (yoy). This increase was primarily driven by strong demand from top cloud service providers and robust sales in enterprise and consumer internet segments. The upcoming Blackwell products are also generating substantial interest, with expectations of early volume ramps adding to the positive momentum.

3. Introduction of New Technologies and Products

NVIDIA is not just resting on its laurels but is actively expanding its product line. The company highlighted the upcoming release of the H200 and Blackwell products, with demand expected to exceed supply well into next year. Moreover, the introduction of the Spectrum-X Ethernet switch is projected to grow into a multi-billion-dollar business within a year, underscoring NVIDIA’s commitment to diversifying its revenue streams.

4. Seasonal Variations and Diverse Portfolio Benefits

While gaming revenue saw a seasonal decline, dropping 8% qoq, automotive revenue painted a different picture. It grew 17% qoq, driven by AI cockpit solutions and self-driving technologies. This diversification helps NVIDIA mitigate the impact of seasonal fluctuations in one segment by capitalizing on growth in others.

5. 10-for-1 stock split to make it more accessible for retail investors

In a significant move, NVIDIA announced a 10-for-1 stock split, set to take effect on June 10. This decision aims to make NVIDIA’s shares more accessible to a broader range of investors, potentially increasing stock liquidity and encouraging greater participation from retail investors.

6. Forward-Looking Valuation and Market Risks

Despite the strong performance, NVIDIA faces potential challenges, including the risk of inventory buildup by cloud customers, increased competition from in-house solutions by other tech firms, and potential slower adoption of AI technologies in enterprise sectors. The company’s stock is currently trading at 38 times FY25 projected non-GAAP EPS, reflecting a valuation that anticipates continued growth amidst these risks.

AI growth story will continue to drive earnings

Overall, NVIDIA’s latest earnings reflect how NVIDIA has benefitted from the surge in demand for AI. The management continues to remain optimistic about the AI growth story in the near-term and investors could take advantage of this structural shift and invest in the company. However, it is also essential to consider the key risks highlighted, such as potential inventory buildups, increasing competition from in-house solutions by other firms, and the uncertain pace of AI adoption in enterprise sectors. At the current level, NVIDIA is trading at 38 times its projected non-GAAP EPS in FY2025, reflecting a valuation that anticipates continued growth.

Disclaimer: ProsperUs Head of Content & Investment Lead Billy Toh doesn’t own shares of the company mentioned.