It’s been big news in the past five days or so and practically impossible to ignore for investors globally.

I’m talking, of course, about the rather rapid collapse of Silicon Valley Bank (SVB) last Friday (10 March). The bank is officially known as SVB Financial Group (NASDAQ: SIVB).

It all started with the announcement of a US$2.25 billion capital raise by the bank on Wednesday, after the market closed.

The upshot of that announcement was a 60% plunge in SVB’s share price on Thursday, the cancellation of the planned share sale and then the subsequent collapse of the bank on Friday as shares plunged another 60% in pre-market trading.

However, for investors in Singapore, should we be worried about contagion to the banking sector in Asia? And how did SVB collapse so quickly and spectacularly?

Here’s what investors in Singapore should know.

What caused the collapse?

The collapse of Silicon Valley Bank was caused by two main issues:

- An asset-liability mismatch that resulted from poor risk management; and

- A very concentrated client base

Regarding its asset-liability mismatch, the bank took on a huge surge in deposits during the pandemic as interest rates were at rock bottom.

It then proceeded put a significant amount of these deposits into bonds, mostly long-dated mortgage-backed securities.

That was all fine if interest rates are zero and not expected to rise. However, it purchased these bonds at record low yields and, as we all know, the bond market cratered in 2022.

The crucial mistake by SVB was putting the deposits into longer-dated bonds, with more than 10 years to maturity. This created significant interest rate risk, which was not hedged, and this came to bear.

Its bond portfolio took a huge hit as interest rates rose but these notional losses escaped scrutiny as SVB was able to classify them as “held-to-maturity” securities that were effectively carried at their cost.

In fact, US$91 billion of its bond portfolio at the end of 2022, which was classified as “held-to-maturity”, was worth just US$76 billion, according to Barron’s.

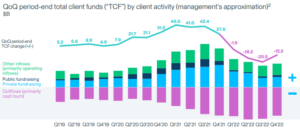

Yet, the deposits SVB took on were not sticky. As VC-backed companies’ cash burn rate picked up in 2022, deposits withered while withdrawals accelerated (see below).

Source: SVB Financial Q4 2022 earnings presentation

This clear pressure on funding in the VC space was a direct effect of the bank’s second problem; its narrow client base.

Concentrated deposit base

As its name suggest, SVB was the banker to the venture capital (VC) and tech ecosystem in the US. The bank’s clients were companies in the technology and life sciences space.

Indeed, 44% of US VC-backed technology and healthcare IPOs in 2022 banked with SVB and it was involved with nearly half of US venture-backed technology and life sciences companies.

What do these corporate clients require of SVB? They park their money with it, as they did in their droves when interest rates were zero and cash was practically free.

However, that has clearly changed in the past year as the Federal Reserve has hiked interest rates by 475 basis points (bps) within the space of 12 months.

That exposed the bank to the demands of corporate clients, i.e. they are much more selective in where they place capital in order to earn a higher return on their deposits.

While much has been made about deposits of US$250,000 and below being federally-insured, only 3% of deposits at SVB were actually under that threshold.

Combined with long-dated bonds and notional losses on these, once word got out about an acceleration in withdrawals, it became a vicious cycle for SVB.

How about large banks?

The news early this morning that all of SVB’s depositors would be made whole – via a joint announcement by the US Treasury, Federal Reserve and Federal Deposit Insurance Corp (FDIC) – means that the immediate fears of contagion have subsided.

It should also be noted that large banks (including here in Asia) have very diversified funding sources and asset bases. Effectively, they serve many different customers and sectors.

The concentration levels of an SVB are highly unlikely. Adding to that is the fact that most banks have floating rate loans that pay more when rates increase, something SVB didn’t possess.

Most of SVB’s assets were actually held in securities, to the tune of 55% of total bank assets.

Implications for investors

The immediate fallout from the SVB saga is likely to have been contained with the backstop announcement for depositors.

However, broader questions surrounding regulation will likely resurface in the medium term.

Broadly speaking, though, investors’ attention will now turn to US Consumer Price Inflation (CPI) data that is due out tomorrow before the market opens.

Following the SVB collapse, many market watchers are now suggesting that the US Fed may either raise interest rates by 25 bps (or even stay steady) when its FOMC meets next week.

It will certainly be an interesting next 10 days for global stock markets.

Disclaimer: ProsperUs Head of Content & Investment Lead Tim Phillips doesn’t own shares of any companies mentioned.