Over the last year, Starbucks Corporation’s (NASDAQ: SBUX) share price has declined by over 30%.

As a result, the coffee giant is now trading at a trailing price-to-earnings (PE) ratio of 20.4 times, a historically low level for the company.

In comparison, Starbucks was previously trading at a five-year average PE of 49.3 times.

As a value investor and coffee lover, this has inevitably attracted my attention but is Starbucks stock worth buying now?

Given the company’s strong business, combined with its superior brand loyalty, it’s definitely worth a look.

So, here are five things to look into before investing in Starbucks.

1. China’s reopening

Starbucks has a massive footprint in China and has been a large part of the coffeehouse chain’s growth.

Unfortunately for the company, same-store-sales in China plunged 23% during the Q2 FY2022 (for the three months ending 3 April 2022) – mainly due to China’s strict zero-COVID policy.

At the end of Q2 FY2022, around one-third of Starbucks stores in China remained temporarily closed or offered mobile ordering channels only.

Therefore, investors need to pay attention to the developments in China as they plays an important role in Starbucks’ growth story.

In fact, during the Q2 FY2022 earnings call, Howard Schultz, interim CEO of Starbucks, reiterated his aspirations for its China business.

“And make no mistake, our aspirations around China have never been greater and I remained convinced Starbucks’ business in China will eventually be larger than our business in the US.”

Schultz added that management will be in a position to share details on the Group’s comprehensive post-COVID China plan once there is more visibility on Q4 FY2022 and FY2023.

That should come as we approach the company’s Investor Day that takes place in September.

It will be interesting to keep an eye on the reopening in China. As it stands, Starbucks has reopened 600 of its 940 stores in Shanghai on just the third day of Shanghai’s official reopening.

2. Howard Schultz’s return

Howard Schultz recently returned as interim CEO for Starbucks and this is the third time that he will lead the company.

In his first stint, Schultz essentially built the Starbucks brand into what we know today. This was way back in 1986.

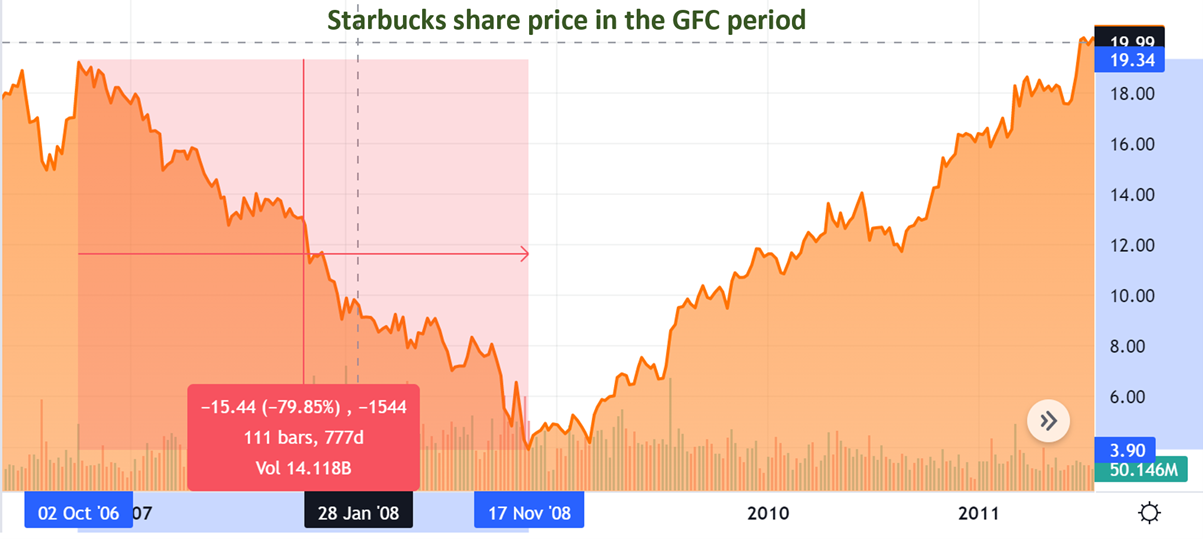

In 2008, he returned as Starbucks’ share price collapsed by more than 75% during the Global Financial Crisis (GFC) period.

Source: SeekingAlpha, ProsperUs

Source: SeekingAlpha, ProsperUs

If you look at the chart above, you will notice that Starbucks’ share price was down by close to 80% over 777 days during the Global Financial Crisis (GFC) period.

The return of Schultz and the recovery in the post-GFC era helped Starbucks regain its mojo.

Whether the third time could be another success for Starbucks remains to be seen but his return post two questions for long-term investors:

1) Starbucks’ reliance on Schultz and;

2) Who’s the next CEO at Starbucks?

3. How will unionisation affect Starbucks?

The ongoing trend of unionisation is another issue that Starbucks has to face.

Since late August 2021, over 200 Starbucks stores in the US have filed to unionise.

Starbucks has responded by raising average hourly wages to US$17 and its share buyback programme has been suspended in order to invest in staff and cafes.

This is a complicated issue that Starbucks needs to resolve but investment in its staff and cafes could prove to be vital over the long term.

After all, the Seattle-based company is well-known for its service, which needs to be maintained in order to drive growth going forward.

4. Starbucks is not immune to inflation and recession

The GFC period proved that Starbucks is not immune to recession and with rampant inflation and rising rates, the next worry is an impending recession.

While Starbucks’ earnings before interest, tax, depreciation and amortization (EBITDA) margin stood at a healthy level of 20.5%, which is higher than the median of 12% in the industry, the company will still have to deal with rising costs.

For example, Starbucks sources coffee beans globally before they’re transported to roasting centres, which then distributes them their worldwide stores.

Yet the prices of coffee beans have more than doubled since 2020 and the supply chain bottlenecks in the global shipping market will increase the cost of transporting coffee.

While these higher costs will eventually be passed on to consumers, it is likely to erode some of its margin in the near term.

5. Improved sales despite the negative headlines

It is easy to get carried away with the negativity and risks associated with a company, which is why I think it is essential for us to look at the financials at the end of the day.

Looking at Starbucks Q2 FY2022 results, global revenue was up 15% (from the same period in the previous year) to US$7.6 billion, driven by 18% revenue growth in the US and stellar performance across its diverse global portfolio.

As mentioned, the margin of the company is likely to be affected and it was obvious as earnings per share (EPS) declined 3% to US$0.59.

Buy Starbucks for its brand power

It is obvious that Starbucks is facing multiple headwinds at the moment but there is reason to be bullish about its future: the Starbucks brand.

If you talk to a friend about going for coffee, Starbucks is likely to be top of the list. The company has also put itself in a position to succeed in China.

And if you look at the return of Schultz, you will notice that the three-time CEO has also been buying up Starbucks shares.

I can’t guarantee that Starbucks will turn the corner soon, with so much uncertainty around, but I will put my money on its familiarity and brand power.

Disclaimer: ProsperUs Investment Coach Billy Toh doesn’t own shares of any companies mentioned.