Unity Software Inc (NYSE: U), a gaming software developer, just saw its shares crater by nearly 10%. But here’s why I think it’s still a strong long-term buy.

Tim’s Take:

For gamers, Unity Software is an integral part of the virtual worlds they exist in. That’s because software developers from Unity help construct these in partnership with large gaming firms that release the latest hits.

Yet Unity has only recently gone public, having floated shares in mid-September. Although relatively fresh to the markets, that doesn’t mean the company isn’t a powerhouse in the gaming world.

Think of Unity’s software as the equivalent of, say, Adobe Inc’s (NASDAQ: ADBE) Photoshop but for gaming developers.

Its other key competitor in the gaming software market is Epic Games, creators of Fortnite and the owner of the Unreal gaming engine.

And yesterday’s market sell-off saw Unity shares fall by nearly 10% as short-term traders decided to take profits. Having initially listed at US$52 a share, Unity shares are still trading at US$150 a pop (even after yesterday’s fall).

Yet Unity tends to be viewed through the same lens as Epic Games, even though it doesn’t publish games like Epic does. That’s a mistake because it has other streams of potential growth beyond just gaming.

AR/VR for the software world

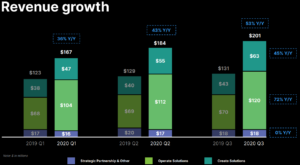

As you can see below, Unity’s revenue in its latest quarter as driven by two divisions; Create Solutions and Operate Solutions.

Although its key gaming software offerings come via Create, Unity is also fast expanding into other areas through its Operate division. It’s doing this by leveraging its experience in nascent technologies such as augmented reality/virtual reality (AR/VR).

Source: Unity Software Q3 2020 earnings presentation

In fact, Unity’s software experience is actually in demand in areas as diverse as construction, architecture and film making.

That puts it more in the mold of an Autodesk Inc (NASDAQ: ADSK), which I’ve written about previously. Over the coming years, I would expect to see Unity encroach more into this space and come into direct competition with Autodesk.

Strong revenue growth at Unity has also been complemented by an incredibly stable gross margin, which has stayed within a tight range of 78-81% over the past six quarters.

Riding mega-trends

As long-term investors we should be looking to tap into the mega-trends and then identify the winning companies within those spaces.

Given Unity’s massive runway for expansion, not only within gaming but also as other industries start to automate and utilise new technologies, this software company’s growth story is just getting started.

Disclaimer: ProsperUs Head of Content Tim Phillips owns shares of Adobe Inc.