A sudden and unexpected banking crisis in the US and Europe saw global stock markets endure a volatile ride in March.

That could shift the market outlook for interest rates significantly.

While the initial reaction to the market uncertainties has sparked a mild market panic, coordinated efforts by regulators and big banks to backstop the industry have helped to calm the market.

Fears of a domino effect of failing banks never came true and the help received supported the global market recovery after the initial selloff.

In Singapore, the Straits Times Index (STI) managed to record a marginal gain of 0.2% to – 3,258.90 points – during the first three months of 2023.

Taking into account its dividend yield, the STI would have delivered a total return of 0.6% during the same period.

With the stock market barely trended upwards, here are five key highlights from Singapore’s stock market during Q1 2023.

1. STI’s trading range doubled during banking crisis

One of the key takeaways from the period was how regulators and central banks managed to calm the market with the announcement to support the global financial sector.

Since 9 March, the STI’s trading range more than doubled to 5.5% for the rest of the month following the focus on the banking crisis in the US and Europe.

Central bank actions supporting financial stability led to a 6.2% gain, in SGD terms, for the SPDR Goldshares ETF (SGX: O87) since 9 March.

In the final week of Q1 2023, several actively-traded stocks posted positive returns exceeding 5%, with Consumer/China and Technology as the common themes.

This is as investors slashed expectations of global interest rate rises after the banking turmoil.

2. Asset and sector rotations amid adjustment of expectations

Asset and sector rotations were more prominent during Q1 2023.

That happened as investors switched to global money market funds from equities, particularly in yield-centric sectors, before rotating into the technology sector.

The technology sector was among the best-performing global sectors for much of the quarter after its laggard performance last year.

3. Institutional investors were net sellers

For the quarter, the Singapore stock market booked net institutional outflows of S$1.5 billion prior to the final session of the quarter, with net retail inflows close to S$780 million.

Institutional investors were net buyers of sectors such as Consumer Discretionary, Utilities, Consumer Staples, Technology, Healthcare and Energy.

Meanwhile, they were net sellers of Financial Services, Telecommunications, REITs, Industrials, Real Estate, and Materials & Resources sectors.

Genting Singapore Ltd (SGX: G13), Best World International Ltd (SGX: CGN), Halcyon Agri Corporation Ltd (SGX: 5VJ), Parkson Retail Asia Ltd (SGX: O9E), NIO Inc (SGX: NIO), The Hour Glass Limited (SGX: AGS), and Zhongmin Baihui Retail Group Ltd (SGX: 5SR) led the net institutional inflows to the Consumer Cyclical sector in Q1 2023.

4. Post-COVID consumer momentum continues

Post-covid consumer momentum continued across the region, with Singapore consumer stocks such as Genting Singapore, Thai Beverage Public Co Ltd (SGX: Y92), Best World, DFI Retail Group Holdings Ltd (SGX: D01), Sheng Siong Group Ltd (SGX: OV8), Halcyon Agri and Zhongmin Baihui among the consumer stocks that received the most net institutional inflows.

DFI Retail expects an improved performance in 2023, on the back of the recovery in Hong Kong and improved performance by its associate, Yonghui superstores, in China.

Meanwhile, Sheng Siong, an inflation hedge, added 2.4% in Q1 2023 to the 17.6% total return it delivered in 2022.

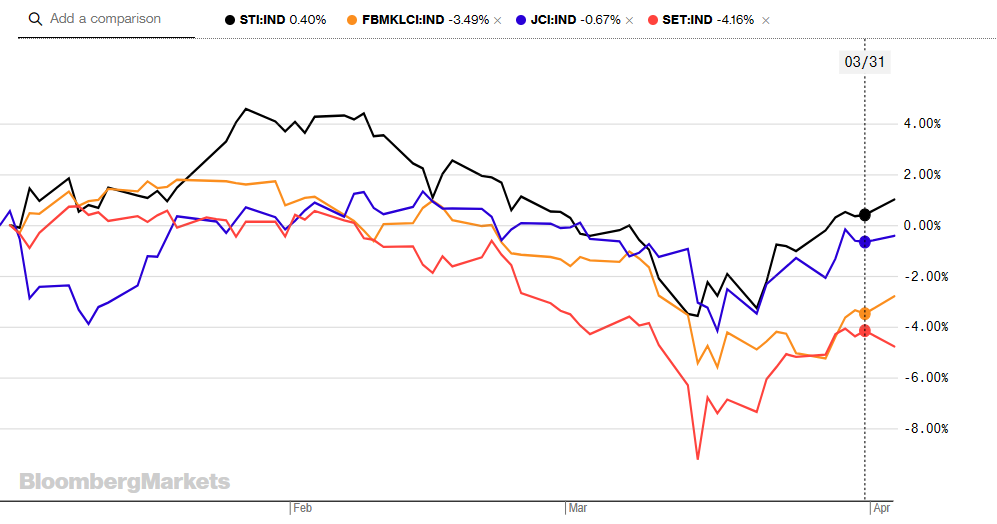

5. STI outperformed regional peers

The Singapore equity benchmark index has outperformed its regional peers during the latest quarter.

The resilient market reflects the strength of the Singapore stock market, especially during a volatile market.

Stay invested with a resilient portfolio

One of the advantages of investing in the Singapore market is the resilient portfolio that investors can build in the long term.

With the strong banking sectors, its resilient REIT players with high-quality assets, the defensive consumer stocks and healthcare sector (as well as the tech players that ride on the structural growth story in the region), there are plenty of options for investors to buy into during a slowdown in the market.

While there are still a lot of uncertainties in the market globally, investors can focus on building a resilient and diversified portfolio that consists of high-quality companies.

Disclaimer: ProsperUs Investment Coach Billy Toh doesn’t own shares of any companies mentioned.